AI Turns IP Into Yield

The biggest AI winners may not be AI companies at all.

Affiliation Disclosure & Disclaimer:

The managing principal of Ridire Research is affiliated with a private investment fund that does not currently hold long or short positions in the securities discussed herein, but may in the future, which could influence the views expressed. This publication is for educational and informational purposes only. Any performance referenced is illustrative and tracked on a per-article basis, not as part of a model portfolio or investment program. Nothing herein constitutes investment advice, a recommendation, or a solicitation. → Ridire Research Substack Disclaimer

Table of Contents

Executive Summary & Special Note

Company Overviews

The Setup

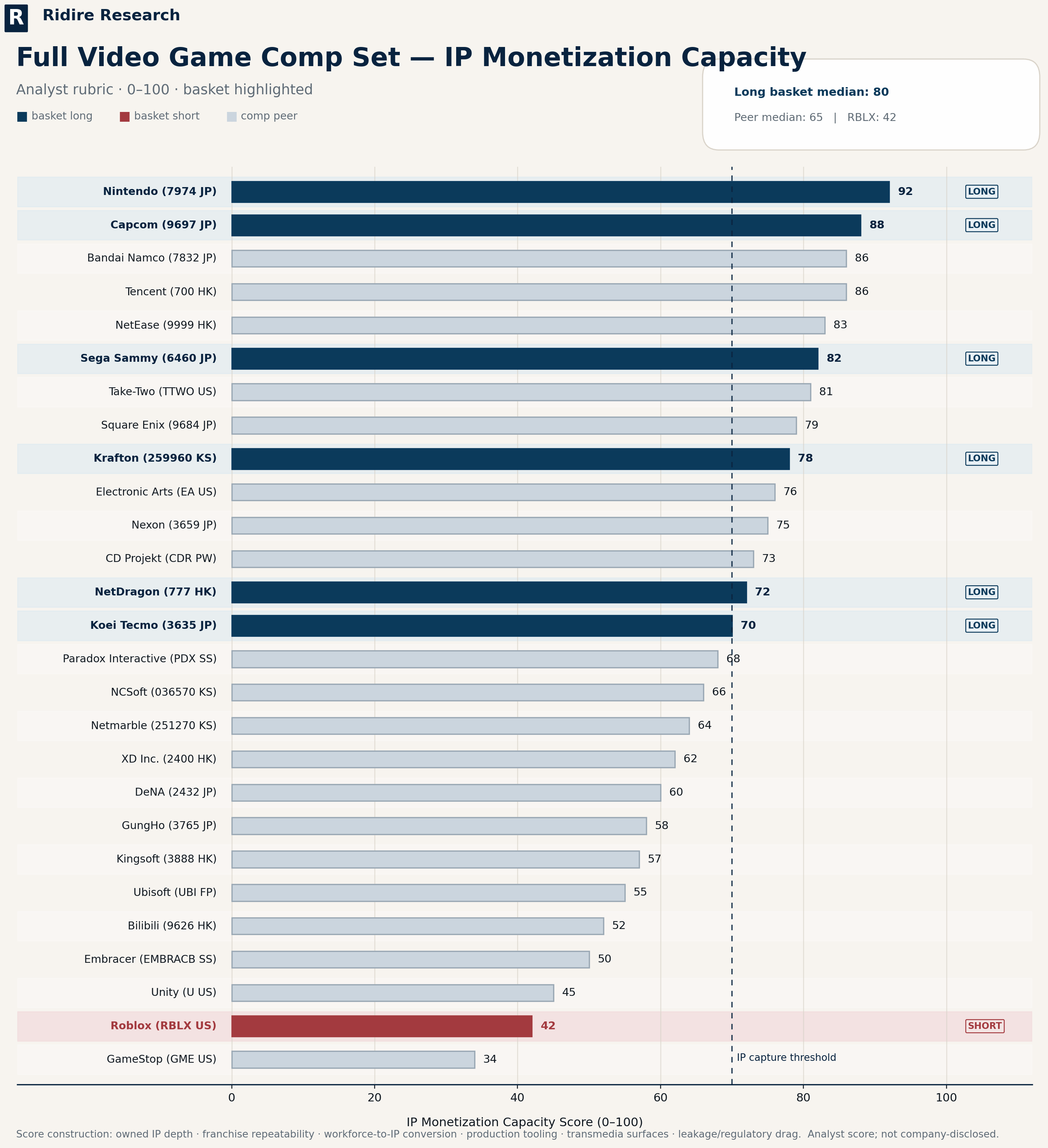

IP Monetization Capacity Score

Causal Mechanism

Timeline

Key Risks

Conclusion

1. Executive Summary

Special Note: This article, along with the proprietary measures and analytical insights presented throughout, was co-authored by Carson Hawley. Carson brings deep experience in the video game development industry and is currently exploring new opportunities. If you’re interested in collaborating with Carson or discussing the industry with him, you can connect with him on LinkedIn HERE.

Most software investors are underwriting the same trade in different wrappers: fewer employees, more automation, higher margins. Our view is that this is too crude for the video games subsegment.

Games are not simply software. They are libraries, characters, worlds, songs, battle systems, fan memory, recurring communities, and half-depreciated catalogs that can be resold for decades if the owner keeps the franchise alive.

In that structure, labor is not automatically deadweight. A writer, artist, engineer, localization team, or live-ops group attached to owned IP is closer to a refinery than an overhead department. The value sits in what the company can issue from the library.

This basket expresses that distinction:

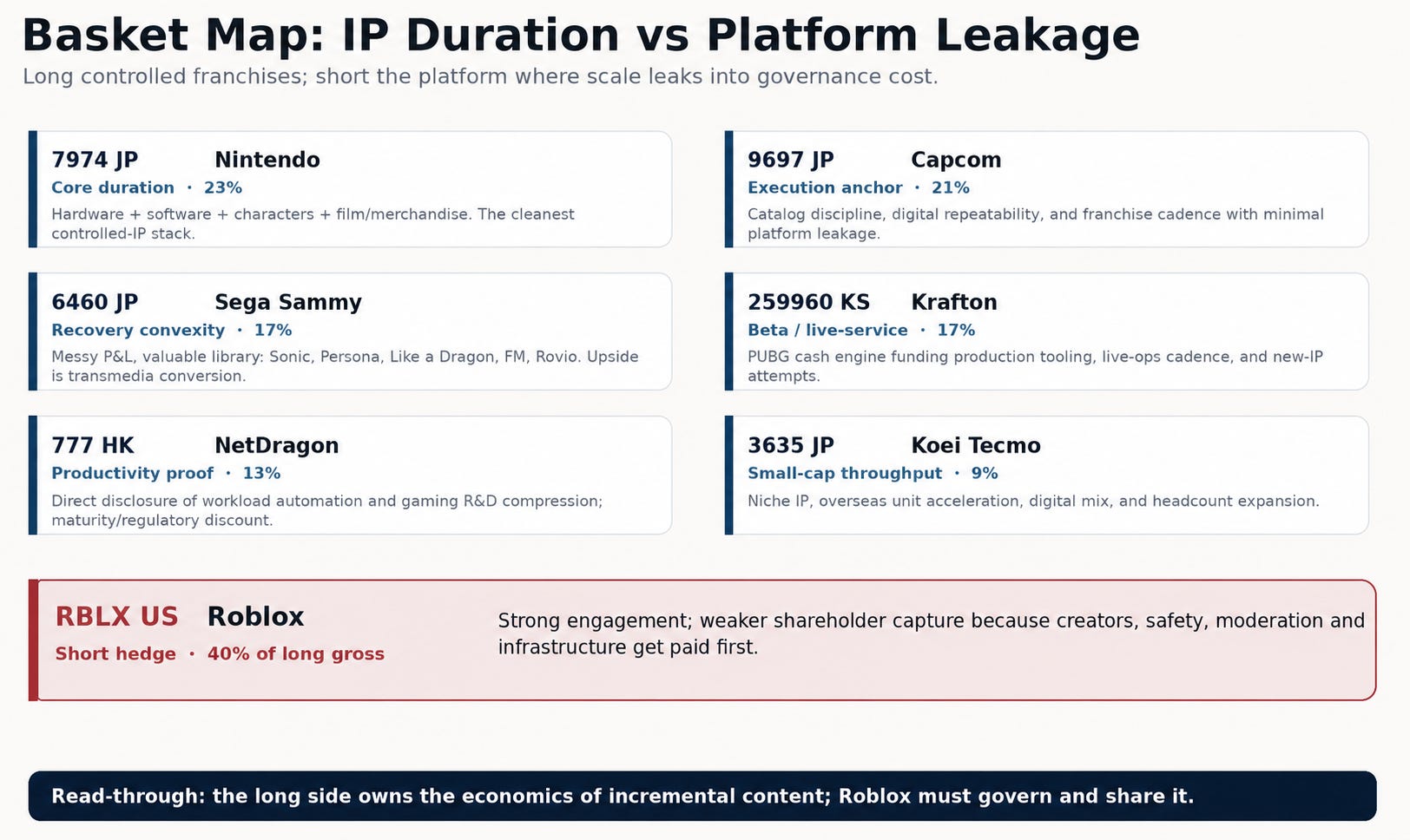

Long the publishers that own the economics of the next unit of content: Nintendo, Capcom, Sega Sammy, Krafton, NetDragon, and Koei Tecmo.

Short Roblox, where usage is large but shareholder capture is polluted by creator payouts, infrastructure, safety, moderation, and regulatory exposure.

In brief: long owned-IP publishers where content economics accrue to the franchise owner; short Roblox, where UGC scale carries higher leakage, moderation burden, and governance cost. Full disclosure: Basket inclusion also cross-referenced names above our IP-capture threshold with Ridire Research’s proprietary fundamental risk/reward metrics.

There is a nuance with Sega worth highlighting: Sega Europe did announce layoffs and sold Relic. However, Sega’s IP still requires a creative workforce to convert legacy assets into products, licensing, mobile adaptations, remasters, and transmedia revenue. A company with weak IP uses productivity tooling to shrink but a company with real IP can use it to issue more revenue-bearing content from the same library.

This distinction can be standardized. We developed an internal score used here called IP Monetization Capacity: a measure of how much of the productivity gain actually reaches shareholders. (More on this in Section 4)

For the basket components, Nintendo and Capcom justify the top scores: Nintendo owns the full stack; Capcom has the cleanest franchise execution. Sega ranks as recovery torque, not quality earnings, valuable library. Krafton is live-service leverage through PUBG. NetDragon and Koei Tecmo are narrower throughput cases. Roblox scores poorly because usage leaks into creator payouts, safety, moderation, and infrastructure before it reaches shareholders.

Basket Calculation: (7974 JP Equity * 0.23 + 9697 JP Equity * 0.21 + 6460 JP Equity * 0.17 + 259960 KS Equity * 0.17 + 777 HK Equity * 0.13 + 3635 JP Equity * 0.09) / (RBLX US Equity * 0.40)

2. Company Overviews

The basket is a stack of different IP-duration profiles:

Nintendo (7974 JP)

It owns the hardware interface, first-party software economics, royalty rails, characters, merchandise, and filmed-entertainment extension.

FY2026 net sales rose 98.6% to ¥2.31tn, operating profit rose 27.5% to ¥360.1bn, and Switch 2 hardware reached 19.86m units with 48.71m units of Switch 2 software.

The debate is how much of Switch 2 becomes high-margin software and recurring IP income rather than a one-cycle hardware pull-forward.

Capcom (9697 JP)

The company reported its ninth consecutive year of record profits, eleventh consecutive year of more than 10% operating-profit growth, and 59.07m consumer game units sold.

Capcom’s edge is discipline: allocate capital to franchises with global repeatability, keep the catalog alive digitally, and avoid cheapening the product with obvious automation artifacts.

Sega Sammy (6460 JP)

FY2026 was not clean. Net sales rose, but operating income declined and the company reported a net loss tied partly to Entertainment Contents weakness and impairments around Rovio and Stakelogic.

The offset is asset value: Sonic, Persona, Like a Dragon, Football Manager, Rovio/Angry Birds, and the broader catalog. Licensing revenue associated with transmedia rose 31.6% year over year, which is the part of the P&L that matters most for the thesis.

Krafton (259960 KS)

PUBG remains the profit pool. Q1 2026 revenue rose 56.9% year over year to KRW1.371tn, operating profit rose 22.8% to KRW561.6bn, and PUBG franchise revenue exceeded KRW1tn in the quarter.

Krafton has the live-service surface area where faster iteration, personalization, and content cadence can matter quickly. The risk is internal disruption and the upside is that a global cash engine funds the transition.

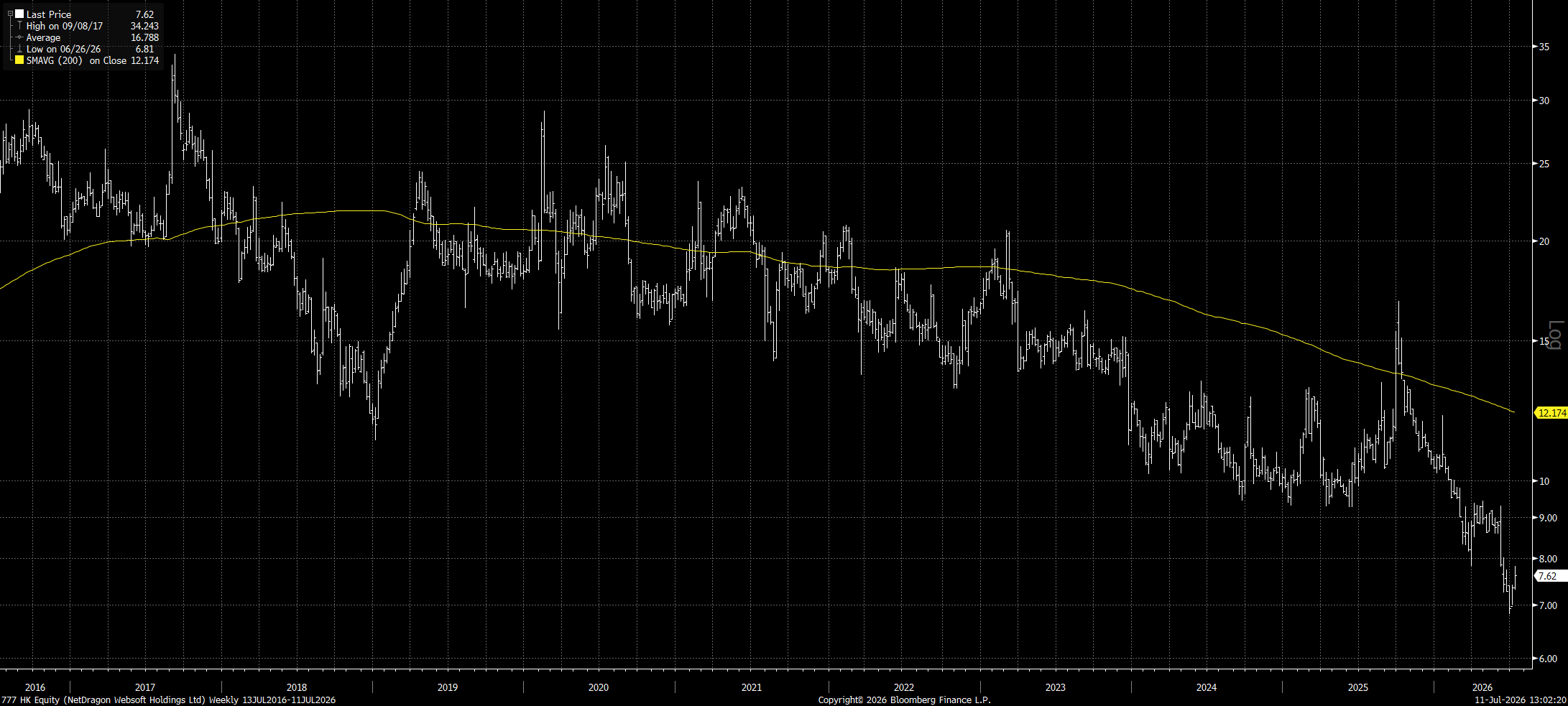

NetDragon (777 HK)

FY2025 gaming and app revenue was RMB3.3bn, or 73.2% of total revenue. Gaming and app core margin rose 3.9 points to 27.4%, gaming R&D expense fell 33.2%, and management disclosed 25% AI-driven workload with a 50% end-2026 target.

It is not the purest franchise-quality long but it is possibly the best case study:

Alignment is unusually strong: founder-chairman Liu Dejian and Liu Luyuan were deemed to control 40.73% of shares at year-end 2025.

NetDragon also uses Tang Yu, an AI-powered virtual executive, as rotating CEO for organizational affairs and strategic execution at its flagship subsidiary

Koei Tecmo (3635 JP)

FY2026 Entertainment segment sales were ¥82.5bn. Console and PC sales increased with 14 new titles, total units rose 84.8% to 14.1m, overseas units rose 88.4%, and the digital ratio reached 61.8%.

Headcount increased by 151 to 2,835. Koei is still adding production capacity because the unit economics of controlled IP justify it.

Roblox (RBLX US) is the short hedge.

Q1 2026 revenue rose 39% to $1.4bn, bookings rose 43% to $1.7bn, DAUs rose 35% to 132m, and hours engaged rose 43% to 31bn.

The cost of governing their growth is simply too high. Roblox reduced expectations because of safety initiatives, expects sequential DAU pressure, and guided full-year 2026 bookings growth to 8–12%, with a projected net loss of $1.035bn–$1.175bn.

This was published over a year ago but many of the key points still hold, if you would like to read it it can be accessed here for free:

3. The Setup

The market has over-learned this generic software lesson: it sees automation and immediately looks for layoffs. That works when the company sells “workflows”. It misses the economics of owned entertainment.

A relevant tangent on selling “workflows”: Alex Karp (CEO of PLTR), of all people, recently changed our perspectives on the whole thing in this interview. If these models are really that powerful, why is everyone still selling tokens? Why not just sell the workflow that makes you a billion dollars?

It is a crude simplification, but if LLMs created that much enterprise value, vendors would charge against the value created rather than simply billing token usage. Raw model access is not the scarce asset. The money should accrue to the person who owns the workflow, the distribution, the proprietary context, and the end-market where the output can actually be monetized. Tokens are the commodity layer.

Furthermore, the market has already produced a kind of reverse-engineered confession:

Social media is full of users posting the same failure mode: the model was not “good enough,” the agent wandered, the output still required human cleanup and somehow the token bill was spectacular.

At some point the question stops being technical and starts being economic, consider:

Do the labs not see the inefficiency in how these agents behave? Or do they see it perfectly well, but have no incentive to fix it quickly?

Their pricing model answers the question:

They charge for token consumption.

They are paid when the machine thinks longer, loops more, retries more, and burns more inference.

Their incentives are straightforward: They get paid when you consume more tokens, not necessarily when you reach the right answer faster.

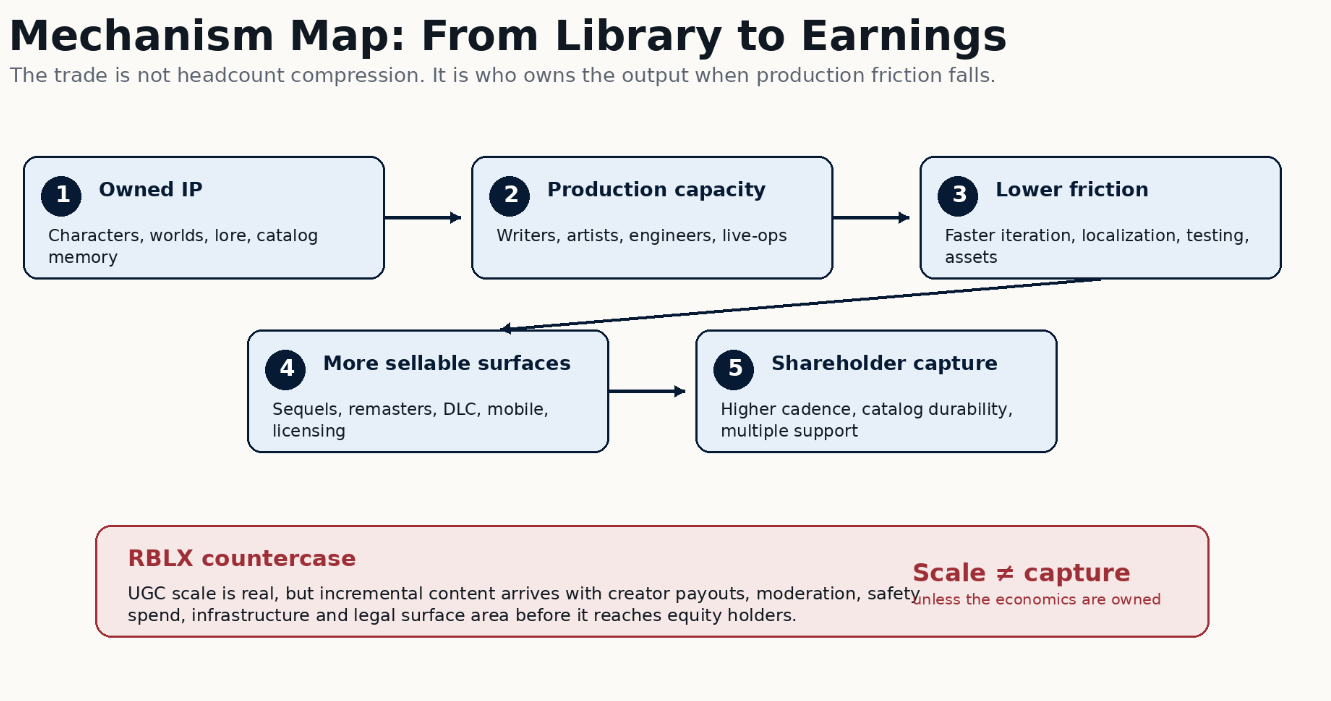

This incentive structure is worth keeping in mind because it extends well beyond foundation models. The economic question is not simply who builds the best model, but who owns the layer where value is ultimately captured. In enterprise software that may be the workflow but in gaming, it is the intellectual property.

A publisher with deep IP is not merely trying to produce the same number of games with fewer people. It is trying to increase the number of credible commercial surfaces from a finite library: sequel, remaster, DLC, mobile adaptation, localization, animated series, film, merchandise, in-game event, live-service season, or catalog relaunch. The marginal product is not code or a workflow, rather it is another monetizable appearance of a familiar world.

The long/short construction therefore is essentially owned issuance versus platform leakage.

4. IP Monetization Capacity Score

The score below is an internal rubric, not a disclosed company metric. It asks one question: when production friction falls, how much of the benefit reaches the equity holder?

The components are deliberately ownership-weighted: depth of owned IP, proof of franchise monetization, ability of labor to convert catalog into product, integration of productivity tooling, transmedia optionality, and the absence of safety or regulatory leakage.

Nintendo scores highest because it owns the stack.

Capcom scores nearly as well because execution discipline has already turned catalog depth into repeatable earnings.

Sega ranks below them because the P&L is messier, but above most of the group on latent IP optionality.

Krafton has live-service torque.

NetDragon has the cleanest disclosed productivity evidence.

Koei has niche IP and visible production investment.

Roblox ranks materially lower because the platform captures scale only after paying creators and policing the system.

The nuance in interpreting the score is that the crucial test is not whether the company can automate work. The test is whether the company owns something worth producing more of.

A bad software business can automate and become a smaller bad software business.

A good IP business can automate and issue more product without surrendering the economics.

5. Causal Mechanism

Library ownership → production capacity → lower iteration friction → more commercial surfaces → earnings durability → multiple support

Nintendo and Capcom are the cleanest versions. They already have global franchises and operating discipline. Production leverage is incremental, not existential.

Sega: The market has good reasons to distrust the P&L: impairments, underperformance, and integration noise. But the IP base is too valuable to price only off recent execution. If Sonic, Persona, Like a Dragon, Football Manager, and Rovio begin showing up as a broader licensing and transmedia engine, the market can stop underwriting Sega as a troubled content house and begin underwriting it as an under-monetized library.

Krafton: PUBG gives the company a high-frequency surface where better tooling should show up in cadence, events, personalization, and operating leverage faster than in a traditional boxed-title model.

NetDragon: The company is already giving investors the kind of disclosure the theme wants: measurable workload automation, R&D compression, and margin improvement. The risk is legacy game maturity; the attraction is visibility into the mechanism.

Koei Tecmo is the overlooked version. Smaller franchise base, lower global heat, but credible unit growth, digital mix, overseas acceleration, and headcount investment. It belongs in the basket because not every IP throughput story needs to be a large-cap.

Roblox is the short because the mechanism runs in reverse. Content volume rises, but so do the liabilities attached to running a youth-heavy UGC platform. More engagement does not automatically mean cleaner equity economics. The company can keep growing and still deserve a lower multiple if investors reclassify it from “frictionless platform” to “regulated social infrastructure with creator leakage.”

6. Timeline

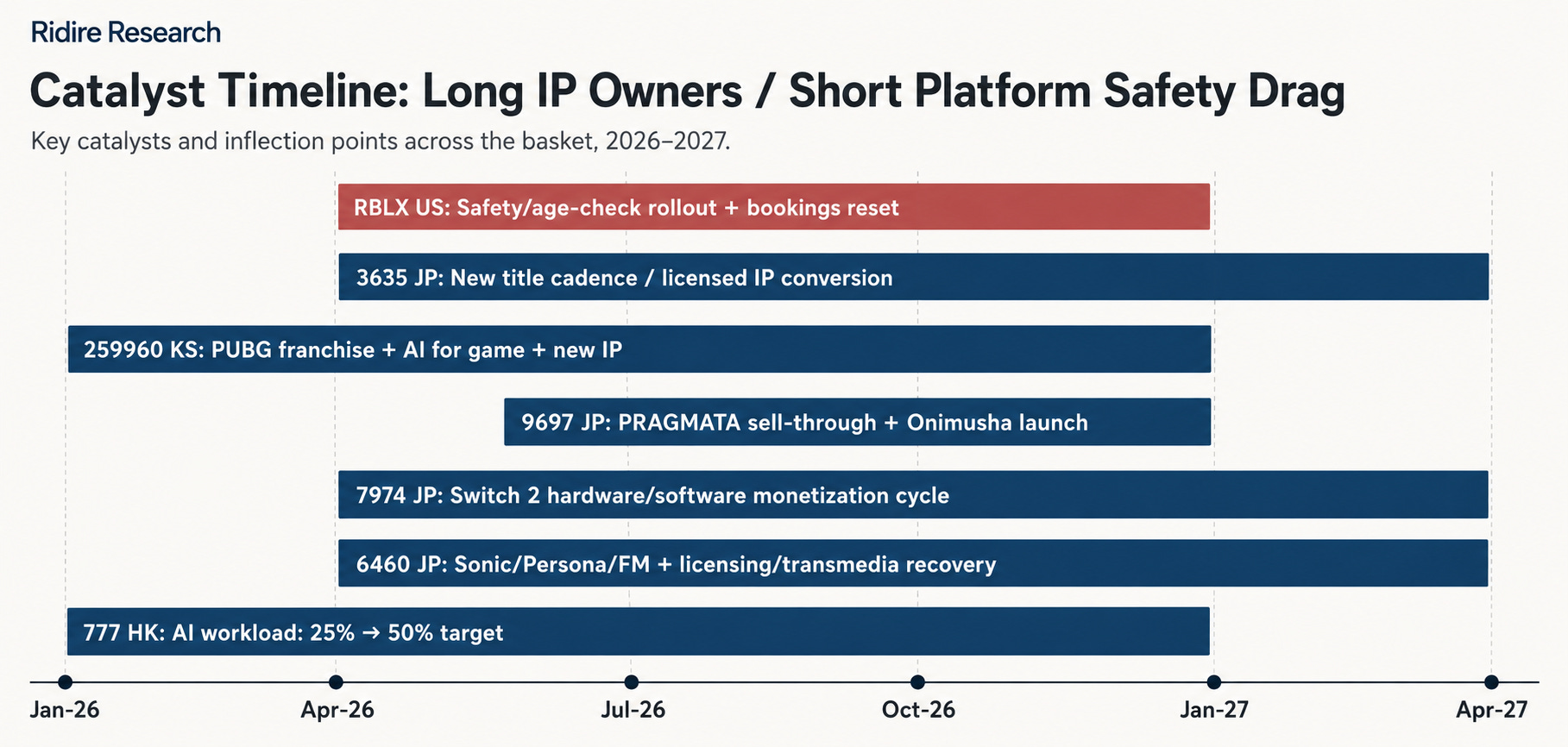

The trade has three windows: productivity proof, franchise conversion, and Roblox guidance pressure.

2026 is the proof-of-mechanism year. NetDragon should be judged against the 50% workload target, gaming R&D efficiency, and whether margin improvement offsets legacy revenue maturity. Krafton should be judged on whether the internal transition improves live-service cadence without damaging culture or product quality.

FY2027 is the Sega test. Sega needs cleaner Entertainment Contents performance, continued licensing/transmedia growth, and evidence that Rovio is not another capital-allocation scar. It needs enough evidence that the library is worth more than the cleanup discount.

Nintendo’s next test is attach and mix. FY2027 guidance calls for ¥2.05tn of net sales, ¥370bn of operating profit, 16.5m Switch 2 hardware units, and 60m Switch 2 software units. Hardware sell-through opens the door; software attach, first-party mix, and IP-related income decide the margin profile.

Capcom’s test is cadence. PRAGMATA, Onimusha, and the broader slate should be monitored less as isolated launches and more as evidence that Capcom can launch new or revived IP without weakening the catalog model. The draft notes PRAGMATA’s rapid sell-through as a validation point for this cadence argument.

Roblox is the near-term hedge catalyst. The next few quarters should show whether safety changes are a temporary DAU disturbance or a structural cost of doing business. If bookings stay near the reduced 8–12% guide and safety costs remain elevated, the short continues to have oxygen. If DAUs stabilize quickly and older cohorts monetize better, the short becomes dangerous.

7. Key Risks

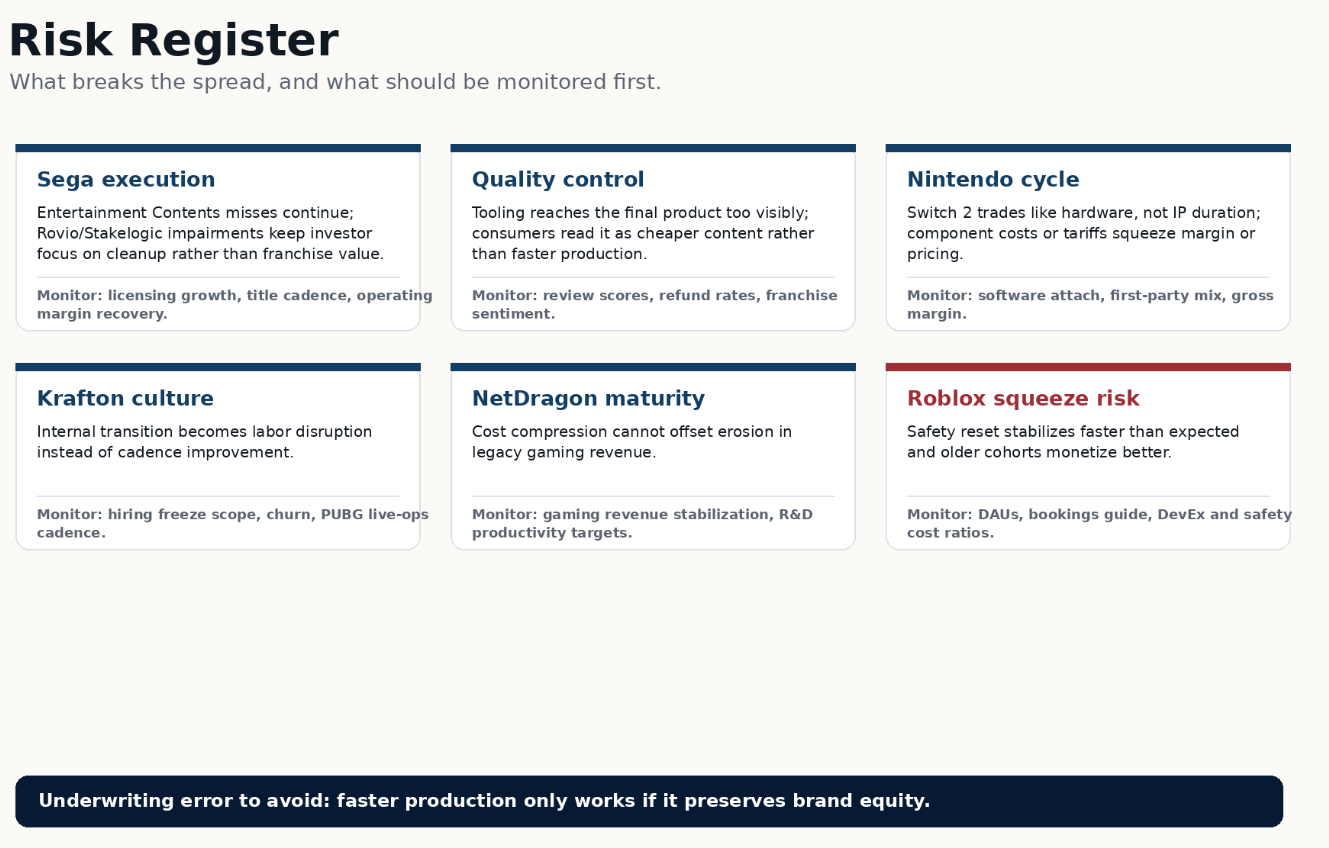

The biggest risk is mistaking production leverage for franchise quality.

Sega can fail the trade by remaining a cleanup story. The IP is valuable, but investors will not pay for latent library value indefinitely if execution keeps producing impairments and missed titles.

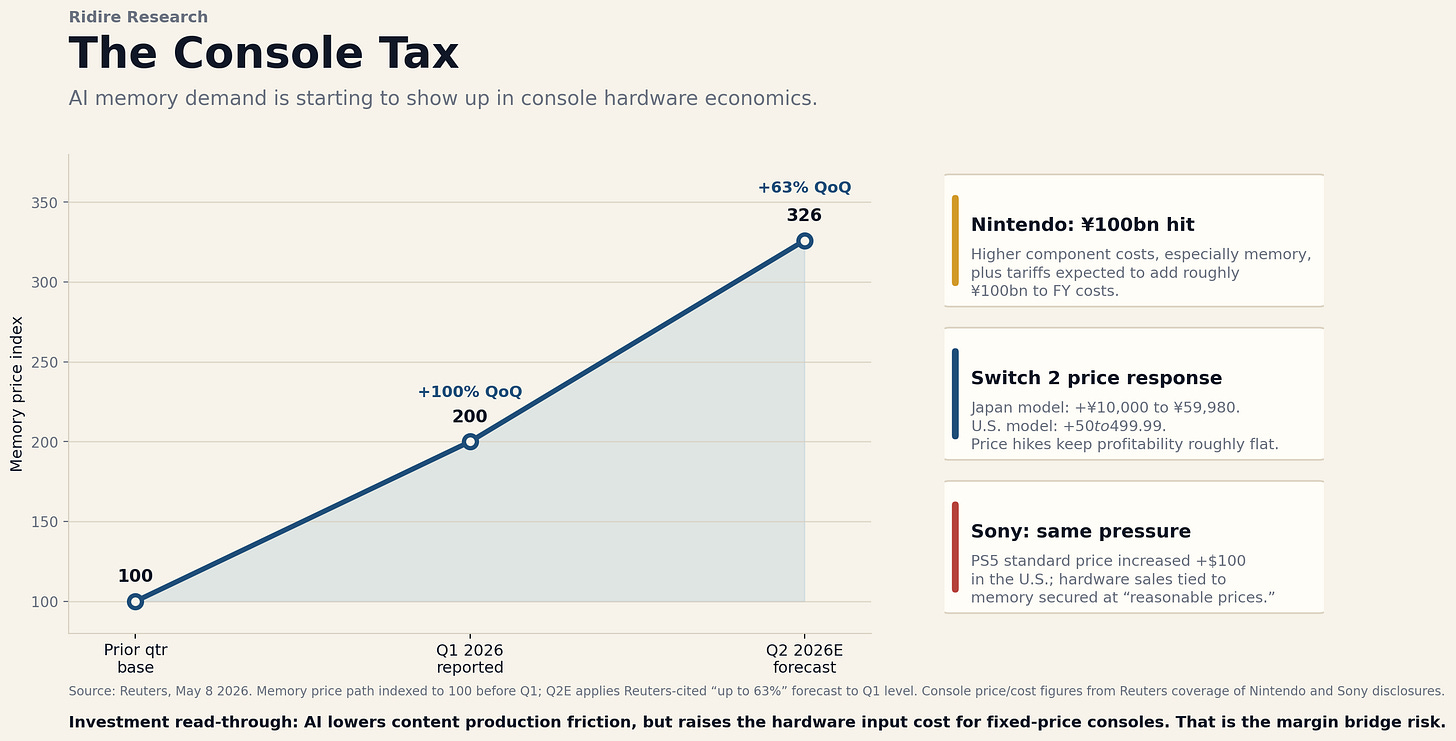

Capcom and Nintendo can fail through brand dilution or cycle mispricing. Capcom’s discipline is part of the asset; if production tooling leaks visibly into the final product and consumers read it as cheap content, the quality multiple should compress. Nintendo’s risk is more classical: Switch 2 can trade like a hardware cycle if pricing, component cost, tariffs, or attach disappoint.

Side note on memory: the console tax. Nintendo’s hardware risk is the collision between a fixed-price consumer device and an AI-driven memory market. Consoles need DRAM and NAND; AI infrastructure is now competing for the same supply chain with a much higher willingness to pay.

That leaves console makers with an ugly choice: absorb the cost, raise hardware prices, or protect margin and risk slower adoption. Switch 2 is not the thesis by itself.

It is the installed-base ramp that feeds the higher-margin part of the model: first-party software, attach, catalog, DLC, subscriptions, licensing, and broader IP monetization. If memory inflation turns the hardware layer into a margin fight, the market can temporarily stop valuing Nintendo as an IP compounder and start treating it like a hardware name again.

Same basic issue for Sony and Microsoft: AI may lower the cost of content production, but it can raise the cost of the box that content depends on.

Krafton can fail through culture. An aggressive internal transformation that reads as restructuring rather than product improvement can damage morale and slow output. Live-service companies do not get infinite chances to disrupt themselves.

NetDragon can fail if cost compression arrives after the revenue base has already faded. Productivity helps only if the company has enough demand to monetize.

Roblox can break the short if safety investment normalizes quickly and the company monetizes older users at a higher rate. The short is not premised on cultural irrelevance. It is premised on a worse shareholder capture rate than the market is willing to price.

8. Conclusion

The basket expression is long owned IP where production leverage accrues to the owner; short UGC scale where production volume increases governance burden before it reaches shareholders.

Engagement is not the same thing as owned economics.

A company cutting labor because workflows are replaceable is not the same as a company retaining creative labor because the labor sits next to monetizable IP. Cost story vs issuance story.

The basket expression remains:

Long 7974 JP, 9697 JP, 6460 JP, 259960 KS, 777 HK, 3635 JP. Short RBLX US.

Calculation: (7974 JP Equity * 0.23 + 9697 JP Equity * 0.21 + 6460 JP Equity * 0.17 + 259960 KS Equity * 0.17 + 777 HK Equity * 0.13 + 3635 JP Equity * 0.09) / (RBLX US Equity * 0.40)

Special note got compressed in the email version, for reference:

Special Note: This article, along with the proprietary measures and analytical insights presented throughout, was co-authored by Carson Hawley. Carson brings deep experience in the video game development industry and is currently exploring new opportunities. If you’re interested in collaborating with Carson or discussing the industry with him, you can connect with him on LinkedIn HERE https://www.linkedin.com/in/carson-blue-hawley/