Bandwidth Wars

Long the Architects of Connectivity’s Future, Short the Commoditized Past

Executive Summary

The LSCONNECT basket is a market-neutral long/short equity basket focused on connectivity infrastructure and bandwidth deployment. The basket is equally weighted on the long and short sides and aims to generate relative alpha by leveraging secular growth tailwinds in next-generation networking while shorting names facing structural headwinds or rich valuations in legacy connectivity markets. This positioning capitalizes on the divergence within the broad connectivity theme:

Longs 0.5% each (HLIT, COHR, CRDO): Providers of critical technology for broadband buildouts, optical transport, and AI data center fabrics, each with strong growth drivers (e.g. cable/fiber network upgrades, hyperscale AI interconnect demand) and reasonable valuations. These companies are enabling the next generation of bandwidth expansion, from gigabit residential broadband to 800G+ optical links for cloud AI clusters. Their fundamentals (double-digit revenue growth, expanding margins, solid balance sheets) and sector positioning suggest outperformance relative to legacy networking players.

Shorts -0.5% each (UI, NTGR, EXTR): Legacy or niche networking hardware makers facing maturing end markets, competitive pressure, and/or premium valuations. These companies largely cater to traditional enterprise, consumer, or campus networking segments that are growing slower and becoming increasingly commoditized. While some have enjoyed a cyclical boost or pandemic-era demand, their forward outlook is muted relative to the secular trends driving our longs. We see these names as structurally disadvantaged in the emerging connectivity landscape, and in several cases their stocks price in optimism (or “value trap” stabilization) that is unlikely to fully materialize.

The connectivity ecosystem is bifurcating: on one side, innovators powering the bandwidth boom (from DOCSIS 4.0 cable upgrades to AI interconnects), on the other, incumbents in low-growth niches (consumer Wi-Fi routers, on-prem enterprise networks) struggling to keep up. By going long the former and short the latter, the LSCONNECT basket aims to capture relative outperformance regardless of absolute market direction. The strategy is not dependent on the overall technology sector rising; rather, it seeks to profit from spread compression as the superior economics and growth of our long positions are recognized against the weaker profiles of the shorts.

Longs are leveraged to strong secular drivers: broadband infrastructure spending (HLIT), explosive demand for optical connectivity in AI and cloud (COHR, CRDO) supported by customer capex cycles and technology upgrades. Shorts are exposed to slower-moving or saturated segments: commodity SMB/consumer networking (NTGR, UI) and enterprise campus networks (EXTR), with fewer near-term catalysts. We discuss each company’s demand drivers and competitive position in detail.

Product Roadmaps & Technology: Our long companies are leaders in next-gen product roadmaps, Harmonic’s virtualized cable access and converged DOCSIS 4.0/fiber platform, Coherent’s 800G/1.6T optical transceivers and all-new optical circuit switch, Credo’s active electrical cables (AEC) and high-speed SerDes chiplets for AI networks. Each is positioned to ride the technology curve as networks upgrade to higher speeds and more software-defined architectures. In contrast, the short side products skew toward incremental updates in maturing technologies (e.g. Ubiquiti’s Wi-Fi access points and switches, successful in their niche but not a fundamentally new architecture; NETGEAR’s consumer routers, reliant on Wi-Fi standard refresh cycles; Extreme’s campus Ethernet switches/Wi-Fi, a competitive field with limited differentiation).

Customer & Market Exposure: The long book is tied into high-growth customer spending areas: Harmonic selling to cable/telco operators investing in gigabit broadband, Coherent and Credo selling to hyperscale cloud and data center customers racing to build AI superclusters. The short book sells to more fragmented or stagnant customer bases: Ubiquiti to small enterprises/WISPs, NETGEAR to retail consumers, Extreme to general enterprises and schools. We provide color on each name’s customer mix and any notable concentration or diversification (e.g. Credo’s recent growth fueled by two top cloud customers and an “emerging hyperscaler”, versus NETGEAR’s broad but low-growth retail channel).

In summary, the LSCONNECT basket expresses a high-conviction view that the future of connectivity belongs to those enabling greater bandwidth, efficiency, and convergence, while legacy pure-play hardware vendors will lag in relative performance.

Thematic Rationale: The Coming Connectivity Boom

Bandwidth demand is surging from core to last mile, creating strong tailwinds for providers of modern connectivity infrastructure, and headwinds for vendors tied to aging hardware. Our long/short positioning reflects four interconnected themes:

Broadband Buildouts (Cable and Fiber):

Global infrastructure is undergoing a major upgrade cycle. Telcos and cable operators are deploying DOCSIS 4.0 and fiber-deep architectures, using distributed access and virtualization to deliver 10G speeds efficiently. Harmonic’s CableOS platform enables operators to scale and converge coax and fiber. Government subsidies (e.g., rural broadband, EU digital programs) further support deployment. HLIT and COHR are directly leveraged here; UI and NTGR lack telco exposure and miss the spend.

Optical Transport & Datacenter Interconnect:

Cloud and 5G networks require massive optical upgrades. Coherent leads in photonic components, its datacom revenue rose 89% YoY on AI-linked demand. The company is scaling 800G modules and developing 1.6T transceivers and an optical circuit switch. These innovations address the surge in AI-related traffic between data centers. Shorts like EXTR and UI lack optical portfolios and are confined to slower-growth hardware segments.

AI Datacenter Fabrics:

The rise of GPU clusters introduces new network demands. Coherent and Credo benefit from this structural shift, Coherent via AI-driven optics, Credo through its high-speed, low-power Active Electrical Cables and SerDes. CRDO's revenue is growing rapidly as hyperscalers scale clusters of tens of thousands of accelerators. EXTR and NTGR do not participate meaningfully in this spend and may be deprioritized as budgets shift toward AI.

Enterprise & Telco Network Architecture Shifts:

Telcos are virtualizing BNGs and cable cores, HLIT’s strength. Enterprises are adopting cloud-managed, AI-augmented networks. Leaders like Cisco and Juniper dominate; smaller players like Extreme face rising pressure. While EXTR’s SaaS ARR grew 23%, total revenue dropped 24% YoY as pandemic-era backlog unwound. HLIT and COHR remain better positioned in modern network infrastructure than traditional switch vendors.

In essence, the LSCONNECT basket is a bet on convergence, virtualization, and scalable bandwidth (800G+/AI fabrics), and a relative short on fragmented, box-based architectures. Our positioning captures this inflection point across connectivity markets.

Long Position Theses:

Harmonic Inc. (HLIT)

Harmonic is a networking equipment company benefiting from the cable broadband upgrade cycle and streaming video growth. With strong execution across Broadband and Video segments, and a large committed backlog, HLIT is well positioned to gain market share as operators shift to next-gen architectures.

Business Overview: CableOS, HLIT’s flagship product, is a virtualized CMTS that unifies coax and fiber (PON) on one platform. With 129 deployments managing ~33.9M modems and a $485M backlog, the platform is scaling. Video streaming is also growing; Q1 revenue was $48.3M, with SaaS up 15% YoY and driving margin expansion.

Growth Drivers: 2025 is a transitional year before DOCSIS 4.0 ramps in 2026. HLIT began shipping Remote-PHY Devices and added another top-5 operator. The company also won multiple fiber access deals, including Tier-1 operators expanding use of its remote OLT. DZS’s bankruptcy has opened market share opportunities. Video growth is driven by live streaming demand and major event delivery.

Financial & Competitive Position: HLIT posted $21M adjusted EBITDA in Q1 and used FCF for buybacks. Gross margins are improving from software mix. Virtualized access faces limited competition as rivals remain hardware-centric. Interoperability and converged cable+fiber solutions help differentiate in fiber access.

Risks: Main risks include timing of DOCSIS 4.0 rollouts, tariff-related uncertainty, and customer concentration. HLIT is mitigating this through global expansion and Tier-2 adoption. Video risks include disruption from internal streaming solutions, though Harmonic's encoding expertise remains competitive.

Conclusion: Harmonic is a rare pure-play on bandwidth growth, with near-term profitability and long-term optionality. As cable capex returns, HLIT is set to inflect positively, offering differentiated upside versus legacy hardware shorts.

Coherent Corp. (COHR)

Coherent is a leader in optical and material technologies with key exposure to datacenter interconnect, telecom fiber, lasers, and SiC materials. It benefits from AI/cloud optical demand and eventual telecom/electronics recovery. Post-merger execution is strong, and its portfolio spans multiple high-growth verticals.

Business Overview:

Networking: Coherent provides transceivers, wavelength components, and sub-systems. Datacom revenue rose 89% YoY in Q1 FY25, driven by AI. 800G shipments are scaling, 1.6T launches are expected in 2025. Coherent is also launching an Optical Circuit Switch for next-gen datacenter architectures.

Lasers: Stable YoY, but with growth in OLED manufacturing tools and new product launches for display and optical network applications. Cross-segment synergy is evident in laser-driven optical network support.

Materials: Focused on SiC, GaAs/GaN, and other advanced compounds. Automotive softness impacted Q1, but long-term EV demand supports recovery. Internal capability supports vertical integration.

Financial & Execution: Margins improved significantly YoY. Debt is being reduced, capex moderating. Free cash flow is rising post-integration. The company’s vertical integration and proprietary tech give it strong positioning.

Technology & Competition: Vertical integration enables in-house production of lasers and photonic elements, supporting better performance and margins. Competes with Broadcom, Marvell, Lumentum, Ciena, and others. Coherent is gaining share and diversifying its customer base.

Risks: Leverage, cyclicality in telecom/cloud spend, geopolitical exposure (China), and competition from giants. However, diversification and scale help buffer volatility.

Conclusion: Coherent is a foundational enabler of next-gen connectivity. Strong execution, product innovation, and AI/cloud exposure make it a high-conviction long, especially relative to legacy enterprise infrastructure names.

Credo Technology Group (CRDO)

Credo is a fabless semiconductor firm focused on high-speed, low-power connectivity solutions for AI/cloud datacenters. Its portfolio directly addresses AI interconnect demands and continues to grow rapidly.

Products:

AECs: Copper cables with active electronics replacing optical links in short distances. Latest 800G models support high-speed rack-level connectivity. Demand driven by hyperscaler AI clusters.

SerDes & DSPs: High-performance chiplets and IP enable 100G+ lane speeds, essential for switches and NICs. Currently developing 200G per lane.

Retimers/CDRs: Signal integrity chips for high-speed board traces, crucial for maintaining performance as speeds rise.

Growth Catalysts: AI infrastructure is driving record orders. Credo rebounded post-2023 customer pause by diversifying accounts. Multiple top customers and an emerging hyperscaler are now ramping purchases. AI rack builds need massive high-speed interconnects, for which AECs are ideal.

Technology Leadership: Strong margins (~65%), fabless model, and efficient R&D. Positioned ahead of slower incumbents in SerDes performance. Maintains edge through integration and power efficiency.

Customer Base: Diversifying beyond initial Microsoft dependency. OEMs and cloud providers now form a broader base. Positioned as a vendor of choice in a fast-growing niche.

Risks: Customer concentration, supply execution, and potential shifts toward optical-only or co-packaged solutions. AECs are well-suited for the near-to-mid term until more advanced options mature.

Conclusion: CRDO is a pure-play on cloud bandwidth growth. Its role in enabling scalable, efficient AI interconnects makes it one of the most levered names to this structural trend. Long positioning captures both growth momentum and secular tailwinds.

Short Position Theses

Ubiquiti Inc. (UI)

Ubiquiti is a profitable but structurally limited networking firm. It faces growing competition, slowing growth, and lacks exposure to high-growth infrastructure verticals like cloud, optical, or telecom.

Business Model: UI serves SMBs, WISPs, and prosumers via UniFi, airMAX, AmpliFi, and UISP. It uses a lean model: no salesforce, low R&D, and direct distribution. While margins remain high, growth has slowed. The Service Provider segment declined, and Enterprise Wi-Fi faces saturation and price competition.

Competitive Pressures: UI is squeezed between low-cost vendors and premium players (Cisco, Aruba). As it moves upmarket, its limited support model and slower innovation cadence become headwinds. Growth increasingly depends on incremental share gains in a crowded market.

Operational Risks: With 1,300 employees and limited R&D spend, UI risks falling behind tech cycles like Wi-Fi 7. Founder-led structure centralizes control but limits transparency.

Strategic Gaps: UI lacks presence in fiber, cloud interconnect, or AI infrastructure. Demand from SMBs and prosumers is cyclical and more discretionary. Macro tightening or slower office reopenings would hit UI harder than core infrastructure names.

Conclusion: Ubiquiti is a well-run business, but strategically disadvantaged versus our connectivity longs. Its focus on traditional Wi-Fi and lack of exposure to secular growth themes makes it a strong short candidate in this basket.

NETGEAR Inc. (NTGR)

NETGEAR is exposed to slow-growth or shrinking markets like home Wi-Fi and small business switches. While cost-cutting has stabilized margins, revenue remains in decline. Its turnaround is unproven and challenged by structural headwinds.

Segment Overview:

NFB (SMB): Growing, but small (~$79M) and not enough to offset declines elsewhere. Pro-AV switches performing well.

Mobile: Revenue down 25% YoY. Demand has normalized post-COVID and growth catalysts are lacking.

Consumer: ~9% decline YoY. Mesh Wi-Fi upgrades peaked in 2020–21. Faces pricing pressure from TP-Link, Amazon, Google.

Strategic Issues: Core consumer segment is commoditized. Subscription initiatives remain small. Wi-Fi 7 might bring a temporary bump, but competition will be intense. NETGEAR’s limited differentiation weakens its recovery potential.

Execution Risk: The company has cut costs aggressively but will need revenue growth to expand margins. Marketing or inventory missteps could reverse gains. Growth from ProAV needs to scale significantly to matter.

Competitive Landscape: Larger vendors (Cisco, Extreme) and upstarts (Ubiquiti) are eating into SMB share. NETGEAR’s simplicity/value proposition is being matched elsewhere. Certification and AV partnerships help, but won’t prevent long-term erosion.

Conclusion: NTGR is a value trap. While margins have improved, top-line pressure remains. Without compelling growth levers, it’s likely to underperform as enterprise and cloud networking demand accelerates.

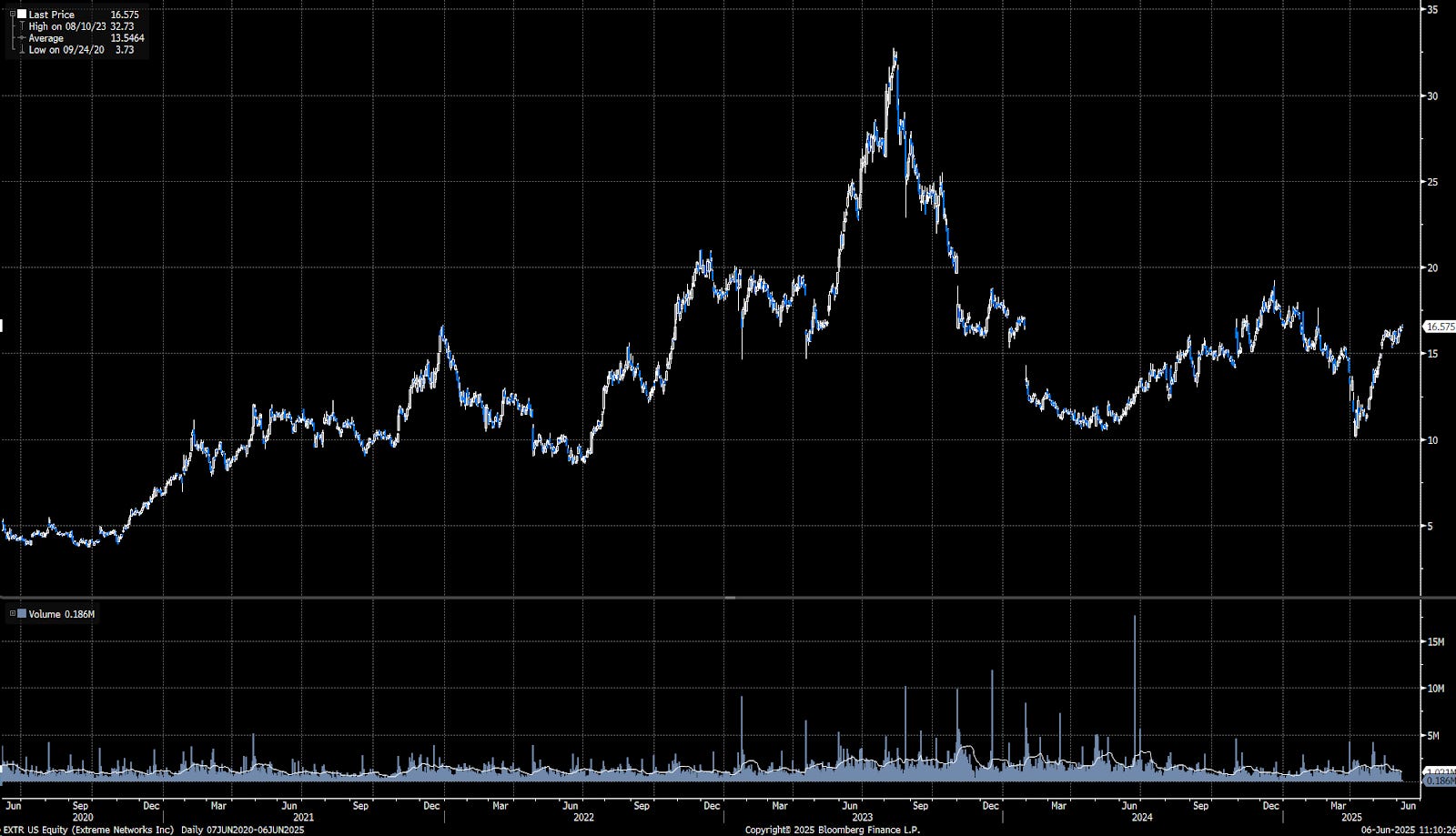

Extreme Networks (EXTR)

Extreme has lost momentum following a strong 2022. Its exposure to mature campus networking and heavy competition limits near-term upside. Backlog tailwinds have faded, and organic demand remains soft.

Performance: Q1 FY25 revenue fell 24% YoY. Product sales dropped sharply post-backlog burn. SaaS ARR is growing (+23%), but not enough to offset hardware weakness. Operating margins fell due to volume loss despite gross margin improvement.

Market Position: Competes in a saturated campus switching market. Faces headwinds from Cisco, HPE Aruba, Juniper, and Arista. Its pitch around cloud-managed fabric is no longer unique. Bigger players have caught up on AI/cloud features.

Why Short Now: FY25 growth depends on a 2H recovery that may not materialize. Macro IT spending is under pressure. EXTR must win fresh deals to grow, without the backlog tailwind. If estimates are missed or delayed, the downside could be material.

Relative Trade Rationale: HLIT and COHR serve strategic upgrades (DOCSIS 4.0, AI optics) that customers must deploy. EXTR’s Wi-Fi refreshes and enterprise switch upgrades are deferrable. In a constrained environment, infrastructure-first vendors win.

Conclusion: EXTR’s competitive position is deteriorating. Without a breakout product or clear growth driver, it lags our long exposures. The stock has rerated on hopes of recovery that may not play out. We see continued underperformance ahead.

Risks & Mitigants

Macro & IT Spending Risk: A global recession could reduce capex in telecom, cloud, and enterprise, hurting our longs. Market-neutral structure helps hedge this. Some secular drivers (AI buildouts, government broadband) may continue. If severe cuts materialize, we will reduce or hedge exposure.

Order Timing Risk: HLIT expects 2025 to be slow before DOCSIS 4.0 ramps in 2026. Coherent’s growth could moderate after AI digestion phases. CRDO’s FY25 strength may be front-loaded. We track order trends and earnings commentary. Basket diversity (cable, optics, silicon) helps absorb timing shocks.

Competitive Risk (Longs): HLIT could face pricing from Cisco/CommScope. COHR competes with Broadcom and Chinese vendors. CRDO may lose design wins. We monitor product cycles and customer engagement closely. Our shorts also face intense competition, so this risk is symmetric.

Execution Risk (Shorts): Shorts may surprise positively. UI could launch a strong Wi-Fi 7 line. EXTR could benefit if Cisco stumbles. NTGR could pop if Wi-Fi 7 drives upgrades. We manage this by keeping position sizing moderate and tracking sales momentum.

M&A Risk: Credo or HLIT could be acquired, creating upside but capping further gains. Shorts like EXTR or NTGR could be PE targets. We monitor M&A chatter and would cover if strategic reviews begin. Basket diversification limits impact from single-name events.

Liquidity & Technical Risk: CRDO and NTGR have limited float. UI’s insider ownership makes it prone to squeezes.

Geopolitical/FX Risk: USD strength or renewed tariffs could impact global operations. Coherent and Credo have China exposure. We monitor FX swings and trade policy, noting some relief has recently boosted margins. Long/short structure helps mitigate systemic shocks.

The LSCONNECT basket is built to absorb macro and idiosyncratic shocks through balanced exposures and active monitoring. We will adjust weights and constituents as needed to protect performance and thesis integrity.

Conclusion

In crafting the LSCONNECT basket, we targeted a powerful secular theme: connectivity infrastructure, and constructed a paired trade to exploit the winners and losers within that theme. Our long positions (HLIT, COHR, CRDO) represent companies enabling the next leg of bandwidth expansion, whether through virtualized cable networks, optical links for AI supercomputers, or high-speed datacenter interconnect silicon. These firms are growing faster than the market, have strengthening financials, and trade at valuations that do not fully reflect their secular tailwinds. Our short positions (UI, NTGR, EXTR), by contrast, are businesses tethered to legacy or slower-growth segments of connectivity, they face structural challenges, competitive pressure, or unwarranted market optimism. By balancing these longs and shorts, we aim to generate alpha that is uncorrelated to general market moves, instead driven by relative fundamental performance as the connectivity cycle plays out.

To recap this basket offers:

Exposure to high-growth connectivity themes (broadband fiber upgrades, cloud optical networks, AI fabrics) without the full volatility of a pure long bet, the shorts provide cushion and could profit in scenarios (e.g. enterprise weakness) that might modestly impact the longs.

A clear catalyst path: as we move through 2025, we expect tangible developments, major DOCSIS 4.0 deployment announcements (benefiting HLIT), hyperscalers expanding AI clusters (COHR, CRDO wins), versus potential disappointments like Ubiquiti’s growth normalization or Extreme’s financial guidance proving too rosy. Each earnings cycle should provide opportunities for the spread to widen in our favor, as evidenced by this Q1: our longs mostly beat and raised (or gave strong outlooks), while our shorts faced growth issues or only modest beats off low bars.

Attractive risk-reward: The longs are fundamentally strong and, in our analysis, somewhat undervalued (especially HLIT, COHR), offering downside protection via cash flows and backlog. The shorts, meanwhile, either have valuation support (NTGR’s cash) or high-quality businesses (UI), which is why we use them in a relative trade rather than outright shorts. This means even if we’re early or partially wrong, the hedged nature limits absolute downside. But if our thesis is largely correct, the relative performance gap could be significant (we anticipate several hundred basis points of alpha, as the longs could each outperform the shorts by 5–15% over the next 6–12 months, summing up nicely in a market-neutral structure).

Model Portfolio Actions:

Longs (1.5% total)

Harmonic (HLIT): 0.50%

Coherent (COHR): 0.50%

Credo (CRDO): 0.50%

Shorts (-1.5% total)

Ubiquiti (UI): -0.50%

NETGEAR (NTGR): -0.50%

Extreme Networks (EXTR): -0.50%

Disclaimer:

Ridire Research is an independent research publication operated by Ridire Research LLC and affiliated with a private fund, an Exempt Reporting Adviser under the U.S. Investment Advisers Act of 1940. Ridire Research is not registered as an investment adviser and does not provide personalized investment, legal, accounting, or tax advice.Informational & Educational Purpose Only

All materials—including text, charts, model portfolios, and explicit labels such as “Buy,” “Sell,” “Hold,” “Long,” or “Short”—are published solely for general informational and educational purposes. They reflect the author’s views at the time of writing, derived from publicly available data, proprietary frameworks, and market analysis, and are not tailored to any reader’s specific objectives, financial situation, or risk tolerance. Subscription to this Substack does not create an adviser–client relationship with the affiliated private fund or its principals.

No Offer or Solicitation

Nothing herein constitutes (i) an offer to sell or the solicitation of an offer to buy any security or other instrument, (ii) a recommendation to participate in any investment strategy, or (iii) a solicitation for investment advisory services. Any references to trades, allocations, or vehicles should be viewed as hypothetical model illustrations only. Offers, if ever made, will be made solely by confidential offering documents and only to qualified investors in jurisdictions where permitted.

Potential Conflicts of Interest

The affiliated private fund, its affiliates, employees, and related accounts may hold, increase, decrease, initiate, or exit positions, long or short, in securities or digital assets discussed, without notice or obligation to update disclosures. Such positions may be inconsistent with views expressed in this publication. The affiliated private fund, related entities, and personnel may initiate, modify, or exit positions in any mentioned security before or after publication without further notice. We maintain internal policies, including trading blackout windows and conflict reviews, to mitigate potential conflicts of interest.

Accuracy & Forward-Looking Statements

Although we strive for accuracy and analytical rigor, information may become outdated and may contain errors or omissions. Forward-looking statements, projections, or target prices are inherently uncertain and may differ materially from actual results. No warranty, express or implied, is given as to completeness, accuracy, or reliability.

Risk Acknowledgment

Investing involves substantial risk, including the potential for complete loss of capital. Past performance, whether actual, indicated by back-tests, or modeled, is not indicative of future results. Securities, derivatives, and digital assets mentioned may be illiquid, highly volatile, or subject to regulatory change.

Reader Responsibility

Readers should conduct their own due diligence, consider their personal circumstances, and consult a licensed financial professional before acting on any information contained herein. By reading this publication you agree that Ridire Research LLC, the affiliated private fund, and their affiliates accept no liability for any direct or consequential loss arising from reliance on the information presented. This research is not directed at persons in jurisdictions where such distribution would be contrary to local law.

“Ubiquiti is a well-run business, but strategically disadvantaged versus our connectivity longs. Its focus on traditional Wi-Fi and lack of exposure to secular growth themes makes it a strong short candidate in this basket. “

Probably you should never short a well run business. They are small team iterating fast with the help of AI.

dude! Don't agree with NTGR thesis. They're pivoting focus on B2b for Proav which appears to be growing quite nicely. MS gains in commercial. If TP link are banned in Retail models, they can pick up anywhere from 30-60% market share in a restocking market. DM me if you want to chat.