Energy’s Shock Absorber

Built for Bad Prices. Paid for Normal Ones.

Table of Contents

1. Investment Thesis

2. Quantitative Context

3. Catalysts & Narrative

4. Risks

5. Conclusion

Thesis Summary:

Coterra Energy (CTRA) is a diversified oil and natural gas producer with an exceptional free cash flow profile and a disciplined capital return strategy. Formed from a merger of premier shale operators, Coterra commands low-cost assets in both the Permian (oil) and Marcellus (gas) basins, allowing it to nimbly pivot investment to whichever commodity offers better returns. Trading at a value-investor price but delivering high margins and return of capital, CTRA offers a compelling opportunity as an “all-weather” energy play poised to outperform when gas prices recover and as its shareholder-friendly initiatives gain traction.

1.) Investment Thesis

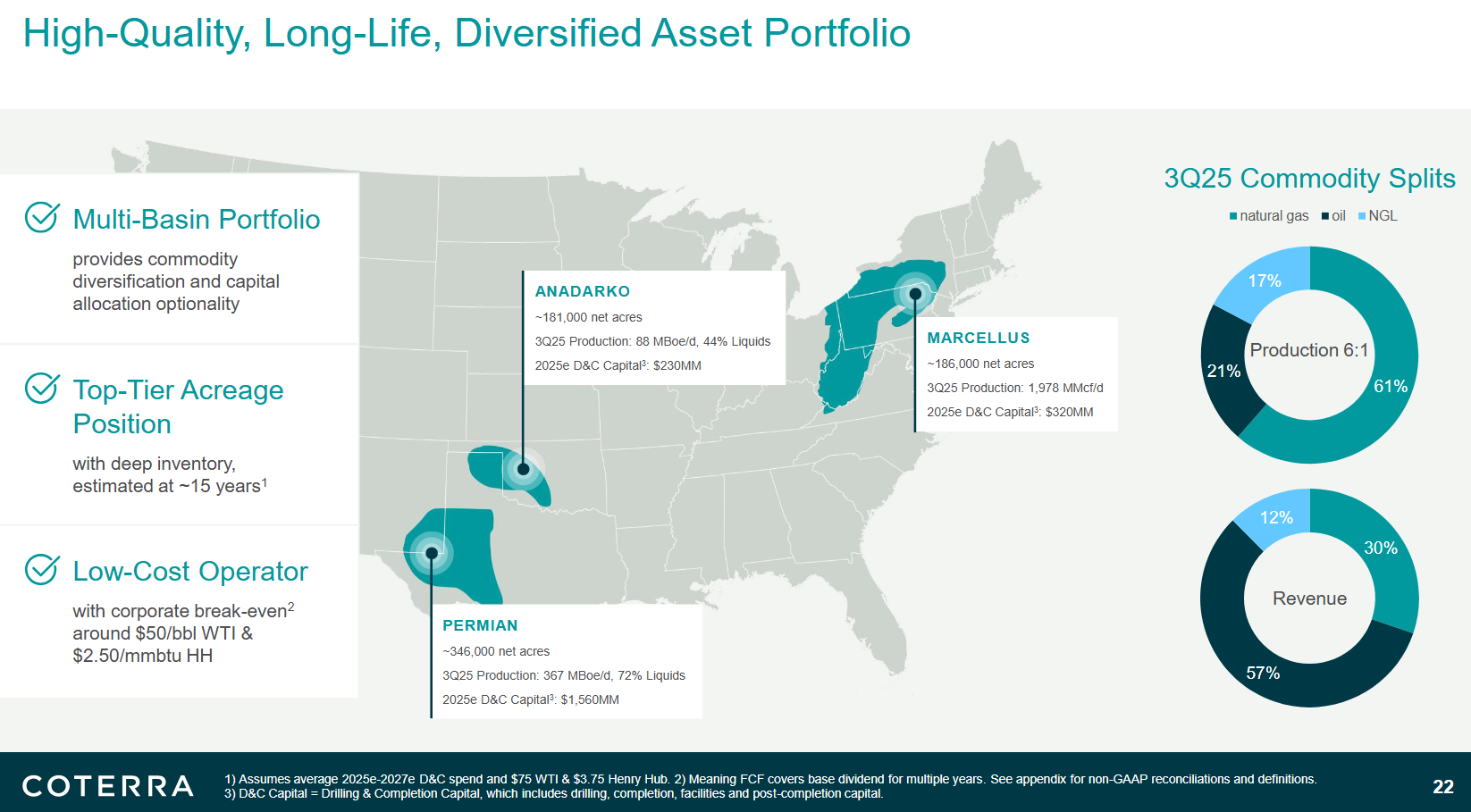

Coterra’s investment case rests on superior business quality and optionality within the energy sector. The company boasts a high-quality, long-life asset base across three core regions – the Permian Basin of West Texas/New Mexico, the Marcellus Shale in Pennsylvania, and the Anadarko Basin in Oklahoma. These assets are top-tier in productivity and cost-efficiency, giving Coterra one of the lowest cost structures in the industry.

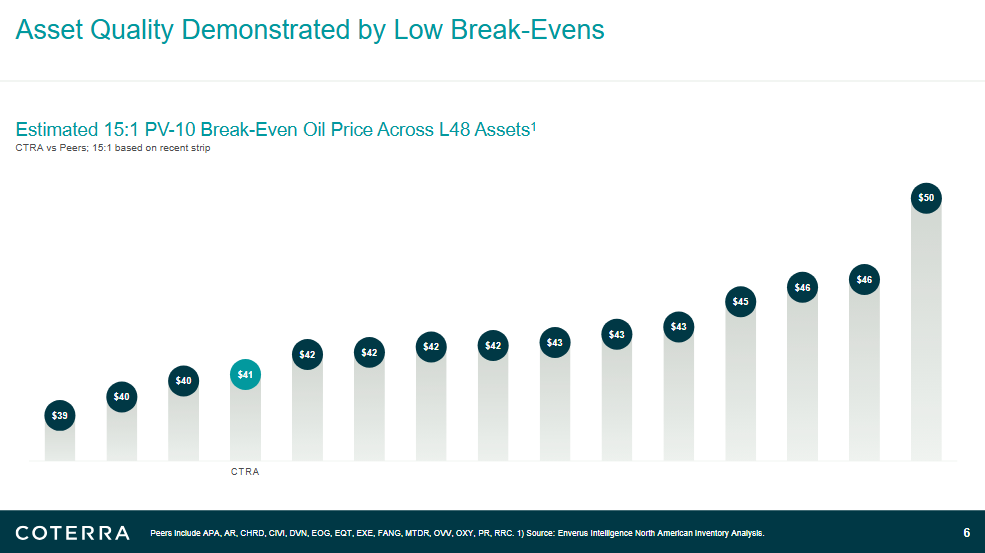

Management estimates Coterra’s corporate free cash flow breakeven at roughly $50/bbl WTI oil and $2.50/MMBtu Henry Hub gas, a remarkably low threshold that underscores its drilling prowess and geology.

In practice, this means Coterra can remain profitable (and even cover its dividend) through harsh downturns that would squeeze many peers off the field. As CEO Tom Jorden put it, the “durability of our high-quality asset portfolio shines throughout various price cycles,” driven by “the quality of the rock, our competitive drilling and completion costs, low cost structure and high margins”. This is a critical moat in a commodity business: Coterra sits low on the cost curve, enjoying high margins when prices are strong and still generating cash when prices are weak.

Diversification as a competitive advantage is the second pillar of the thesis. Unlike pure-play E&Ps, Coterra is a true oil and gas company, about half of its revenue comes from oil and liquids and half from natural gas, depending on price levels. This multi-basin, multi-commodity model gives Coterra flexibility to allocate capital to the highest-return projects at any given time.

For example, in 2023’s weak gas environment, Coterra leaned into its oil-rich Permian assets (running 9 rigs there) while scaling back activity in gas-focused Appalachia. Conversely, if gas prices surge, Coterra can ramp Marcellus drilling to capitalize. This dynamic approach maximizes returns and acts as a natural hedge: oil and gas fundamentals often diverge, and Coterra can benefit from whichever is favorable. Notably, an activist investor (Kimmeridge) has pressed Coterra to become a pure Permian oil player, but the company maintains that the “diversified strategy” unlocks more value by not “overlook[ing] the value of Marcellus gas assets”. We agree with management’s view: the gas segment is a strategic asset with significant long-term worth, and the diversification adds resilience. In short, Coterra has built-in optionality that most peers lack.

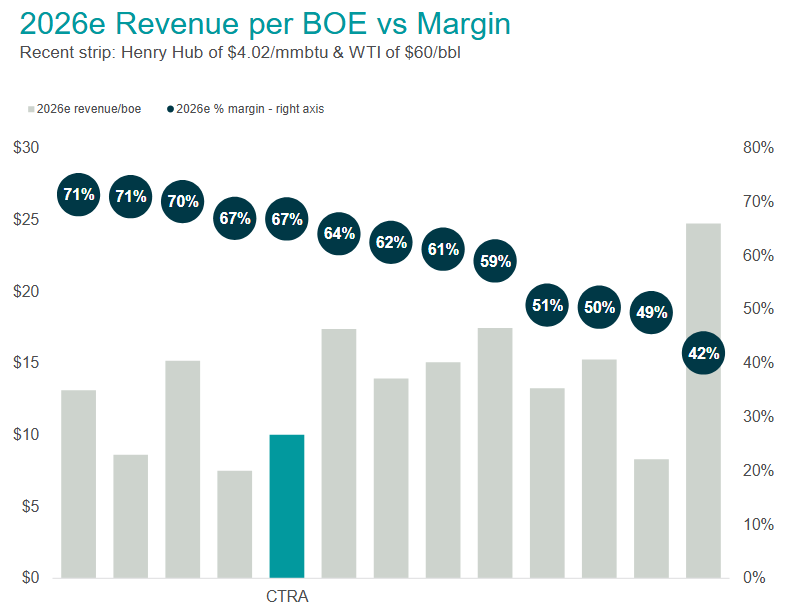

Crucially, Coterra couples this quality asset base with strong financial discipline and shareholder focus. The company runs a conservative reinvestment rate (about 50–55% of cash flow back into capex), which is far more restrained than shale drillers of the past and ensures hefty free cash flow. Indeed, at current strip prices Coterra expects ~$2.0 billion of free cash flow, roughly a 10% yield on the market cap. Rather than chase reckless growth, management prioritizes returning cash.

The stock’s valuation is mispricing these strengths, in our view. Despite its quality and cash generation, CTRA trades at a single-digit cash flow multiple and offers a high-single-digit to low-double-digit FCF yield at the current price.

Such a valuation implies skepticism either about commodity prices or about Coterra’s hybrid model.

This creates a classic asymmetry: Coterra is already highly profitable at today’s depressed gas prices, any improvement in pricing or sentiment could unlock outsized equity upside, whereas downside is cushioned by the company’s low cost base and ongoing buyback/dividend support. In effect, investors are “getting paid to wait,” collecting a ~3–4% base dividend (and additional buyback-induced EPS growth) while the thesis unfolds. Few E&Ps combine this level of income with torque to a recovery. In sum, Coterra represents a rare “quality-value” play in energy. It has the moats of low cost and diversified assets, the prudent capital allocation of a seasoned operator, and the shareholder orientation of a mature cash cow. Yet it’s “unloved and misunderstood” by some in the market (to borrow a recent description), a perception we expect will change as catalysts materialize.

2.) Quantitative Context

Under Ridire’s proprietary REC (Ridire Efficiency Composite) framework, Coterra screens as one of the most operationally efficient energy producers in our coverage universe. On this measure, CTRA ranks in the top decile of the sector, reflecting a business that consistently converts asset quality and capital discipline into durable cash outcomes.

CTRA’s REC strength is driven by its ability to sustain high free cash flow efficiency at current strip pricing without reliance on leverage, aggressive reinvestment, or favorable commodity conditions. The company demonstrates a repeatable capacity to self-fund operations, maintain production, and return capital through the cycle, a profile that distinguishes structurally efficient operators from cyclical beneficiaries.

Forward-looking indicators embedded in REC further reinforce this positioning. Coterra sits in the upper tier of large-cap E&Ps on operating durability, pairing strong margins with measured growth rather than volume-led expansion. This balance supports cash stability and limits downside sensitivity during weaker pricing environments.

Taken together, CTRA’s REC profile signals an efficiency advantage that is not fully reflected in market expectations. The stock is not mispriced because it is misunderstood on valuation, but because its operational efficiency tends to be under-appreciated during periods of commodity pessimism.

This gap between measured efficiency and prevailing sentiment is central to the CTRA thesis and frames the catalyst discussion that follows.

3.) Catalysts & Narrative

Coterra is positioned for a constructive shift in its operating environment without requiring a single-point forecast. U.S. natural gas fundamentals are moving toward balance as export capacity expands and supply growth moderates, creating asymmetric upside for large, low-cost producers with embedded optionality. Coterra’s scale gas position and capital flexibility allow it to participate in this transition without sacrificing balance sheet integrity.

The oil portfolio provides stability. Execution in the Permian continues to improve through efficiency gains and disciplined capital deployment, reinforcing cash durability at mid-cycle conditions and insulating returns from industry-wide growth deceleration.

Capital returns remain a core lever. Coterra’s framework prioritizes balance sheet strength while preserving flexibility to increase shareholder distributions as visibility improves. This approach compounds downside protection and supports re-rating as cash flow consistency becomes more evident.

Finally, the market narrative is evolving. What was once viewed as strategic ambiguity is increasingly recognized as resilience. As focus shifts toward efficiency, durability, and capital stewardship, Coterra’s diversified model and operating discipline are more likely to be rewarded.

4.) Risks

Coterra remains exposed to oil and natural gas pricing. A prolonged period of weak demand or oversupply would pressure cash generation and constrain capital returns. While the company’s cost structure and flexibility mitigate downside relative to peers, hedging can also dampen upside participation in sharp commodity recoveries. The market largely prices this risk as persistent; our view assumes eventual normalization, but timing remains uncertain.

Activist involvement introduces headline and strategic uncertainty. Pressure to pursue asset sales, structural changes, or strategic simplification could create execution risk or reduce diversification benefits if pursued opportunistically rather than cyclically. That said, increased scrutiny may also accelerate value recognition rather than impair it.

Coterra’s forward profile assumes continued operational consistency and successful integration of recently acquired assets. Any shortfall in drilling performance, cost control, or inventory quality would weaken the efficiency thesis. The company’s track record reduces this risk, but it remains a key variable to monitor.

Exposure to regulated basins introduces risks around permitting, environmental compliance, and infrastructure availability. These factors can limit growth optionality or reduce realized pricing, particularly for natural gas. Coterra’s conservative growth posture partially reflects this constraint.

A core point of debate is whether Coterra’s diversified oil-and-gas model enhances resilience or suppresses valuation. Bears argue the company lacks the focus needed to earn premium multiples. Our view is that the market over-penalizes this structure during commodity troughs, despite evidence that diversification improves cash durability and risk-adjusted returns.

Overall, these risks are real but largely known. We believe they are more than reflected in current expectations, while the upside from improved conditions and sustained execution remains under-appreciated.

5.) Conclusion

Coterra Energy is a case study in fundamental value waiting to be recognized. The company’s unique combination of low-cost, diversified assets and prudent capital management has produced a cash flow juggernaut that the market has yet to fully appreciate. Our analysis, highlights that CTRA scores highly on both profitability and valuation metrics, an alignment rarely seen without a catch. In Coterra’s case, the “catch” has been negative sentiment around natural gas and a complex story, but those are precisely the factors we see turning into tailwinds. As the narrative shifts, aided by improving gas markets, consistent execution, and active capital returns, we expect Coterra’s high efficiency, high cash yield profile to be rewarded.

In essence, Coterra offers the best of both worlds: it’s an energy producer that can thrive in either oil or gas up-cycles, and it pays you well to own it in the meantime. The stock’s current mispricing provides a margin of safety, while the upcoming catalysts provide multiple shots for unlocking value. This is a high-quality business priced like a mediocre one, a discrepancy worth exploiting.

Disclaimer:

This publication is for educational and informational purposes only. It reflects research opinions and illustrative examples, not investment advice or recommendations. Nothing herein constitutes an offer, solicitation, or advice to buy or sell any security. By reading, you agree to the full disclosures → Ridire Research Substack Disclaimer