From Royalties to Reinvention

A Royalty Stock Becomes a Capital Allocator

Affiliation Disclosure & Disclaimer:

The managing principal of Ridire Research is affiliated with a private investment fund that holds long positions in the securities discussed herein (Shionogi & Co., 4507 JP), which could influence the views expressed. This publication is for educational and informational purposes only. Any performance referenced is illustrative and tracked on a per-article basis, not as part of a model portfolio or investment program. Nothing herein constitutes investment advice, a recommendation, or a solicitation. → Ridire Research Substack Disclaimer

Table of Contents

Executive Summary

Company Overview

The Setup

Causal Mechanism

Timeline

Key Risks

Conclusion

Executive Summary

Shionogi (4507 JP) used to be easy to understand: a conservative Japanese pharma company with a large HIV-linked royalty stream, high margins, and a clean balance sheet. That version of the story is now stale.

The company is using its cash-flow base to do three things at once:

Deepen exposure to ViiV Healthcare.

Buy a U.S. rare-disease commercial business through RADICAVA.

Turn Fetroja / cefiderocol into a more strategic antimicrobial-resistance asset through U.S. government procurement.

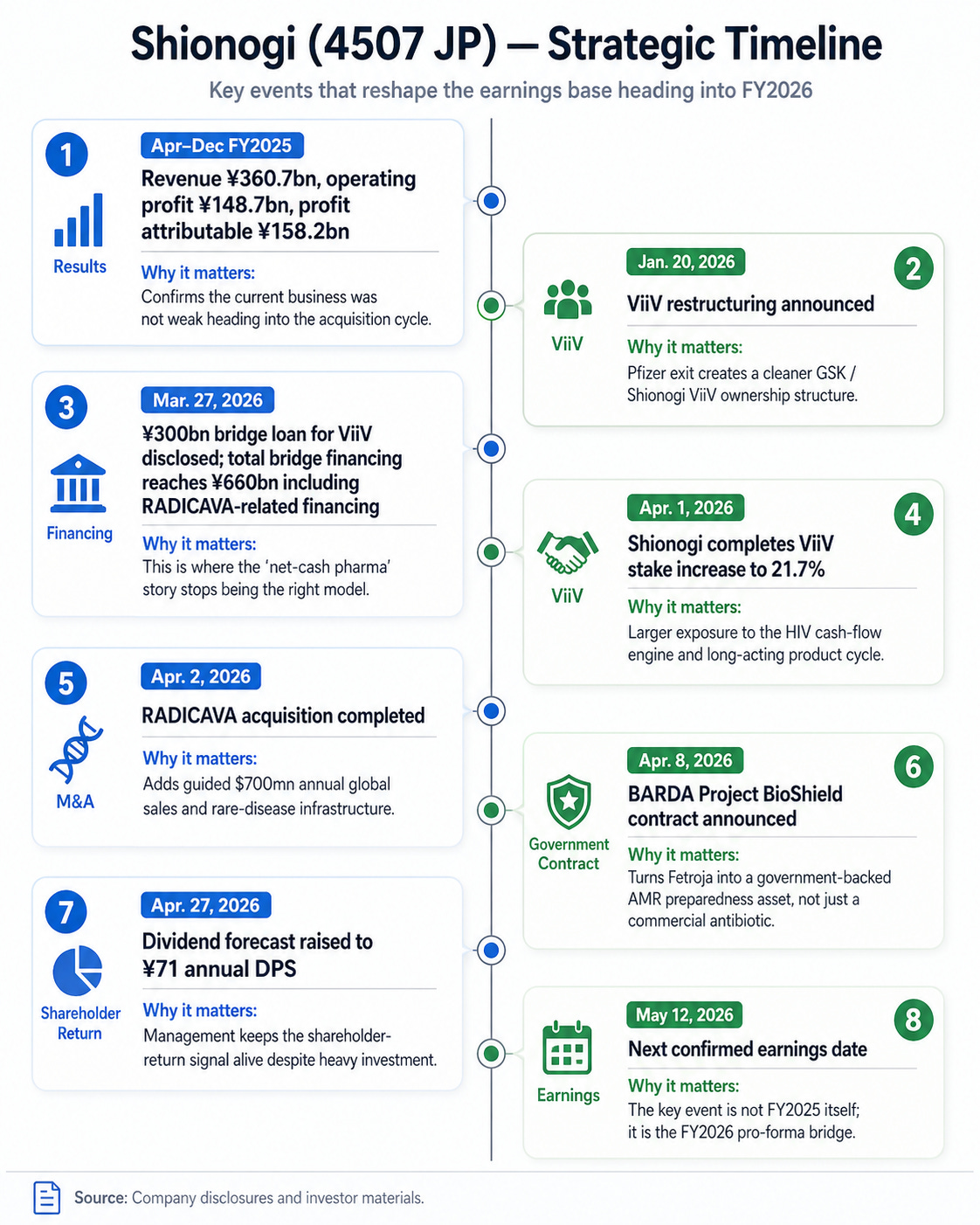

The result is a re-underwriting of what Shionogi’s earnings base should be worth after the balance sheet is put to work. The issue is whether management has just spent the old balance-sheet story on assets that extend the duration of the earnings base. The next serious checkpoint is the FY2026 guide, especially the bridge from ViiV, RADICAVA, financing cost, amortization, and post-deal leverage.

Company Overview

Shionogi is a Japanese pharmaceutical company with a historical strength in infectious disease, small-molecule drug discovery, HIV, influenza, and antimicrobial resistance. The company also has exposure to CNS / pain, sleep, rare disease, and domestic Japanese prescription drugs. The current reported business still looks unusually profitable:

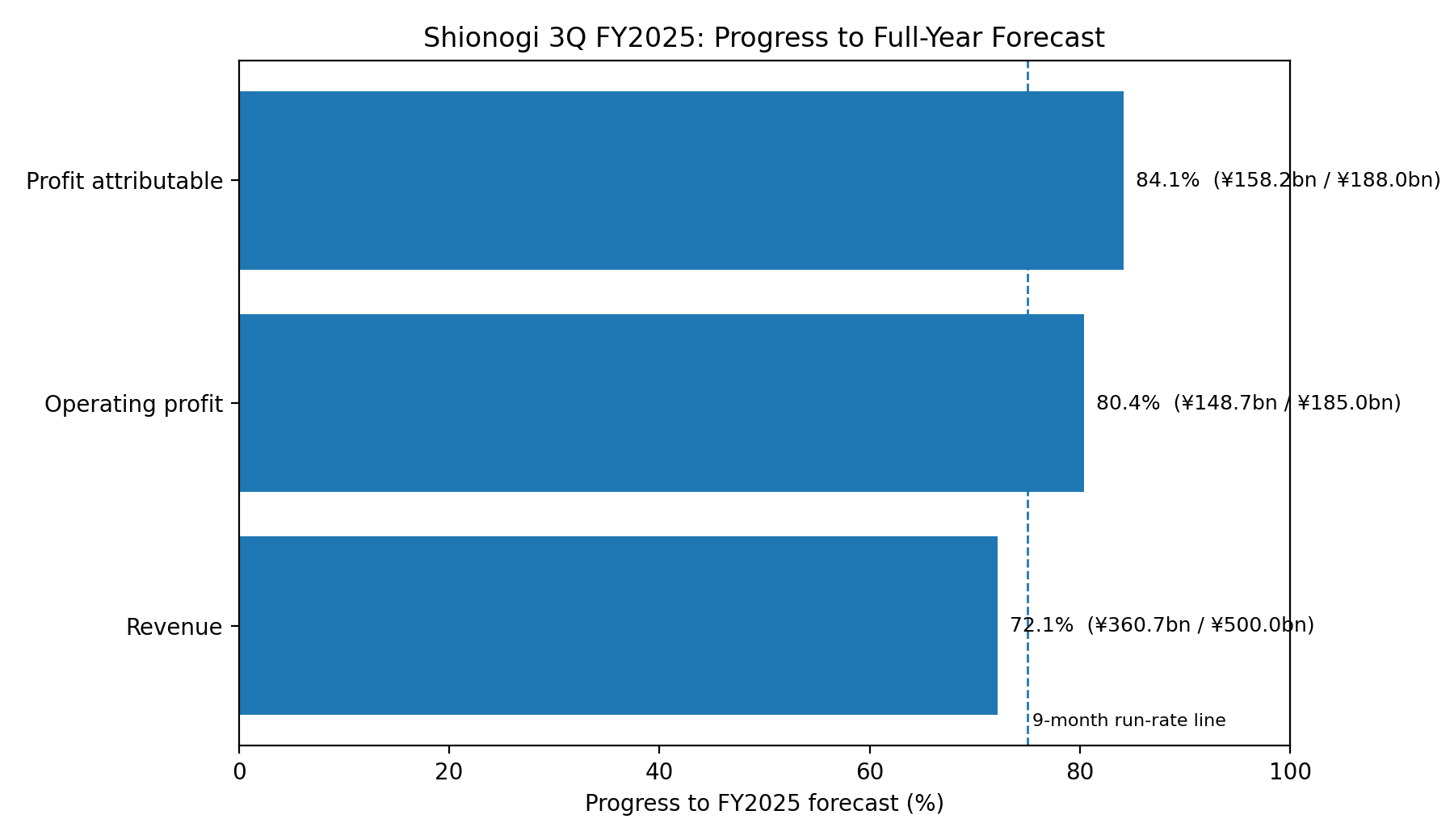

Figure 1 — FY2025 guide progress

At the Q3 FY2025 stage, Shionogi had already reached 72.1% of full-year revenue guidance, 80.4% of full-year operating profit guidance, and 84.2% of full-year profit-attributable guidance.

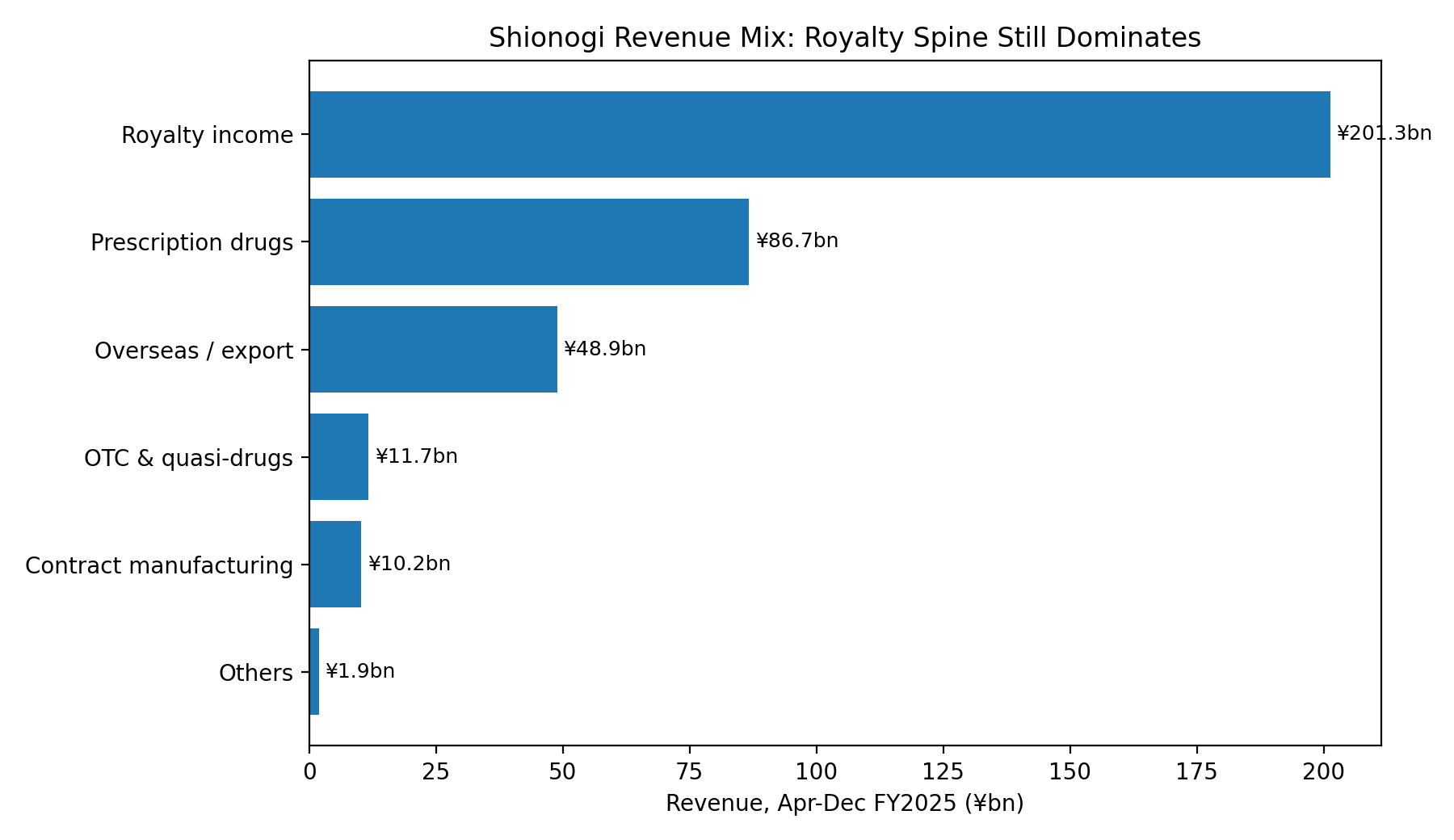

Figure 2 — Revenue mix

Prescription drugs contributed ¥86.7bn in Apr–Dec FY2025, overseas subsidiaries / exports contributed ¥48.9bn, and royalty income contributed ¥201.3bn.

Within the royalty line, the HIV franchise was ¥193.4bn. In plain terms: Shionogi is still economically anchored by HIV royalties more than by its domestic prescription-drug business.

A notable warning worth addressing: the valuation looks reasonable on the surface (~12–13x forward), but it is not obviously cheap. More importantly, the “net cash” screen may overstate balance-sheet comfort because Shionogi is using bridge financing to fund the ViiV and RADICAVA transactions.

However, that does not kill the bull case. The setup is no longer “cheap net-cash royalty compounder.” It is whether Shionogi can use its balance sheet to turn royalty income into a broader specialty pharma platform with more U.S. exposure, more owned products, and more control over future cash flows.

The Setup

The market knew Shionogi as a low-drama royalty compounder. Management is now forcing investors to decide whether it should be valued as something broader: a royalty-backed specialty pharma acquirer with more U.S. exposure and more control over its future cash-flow streams.

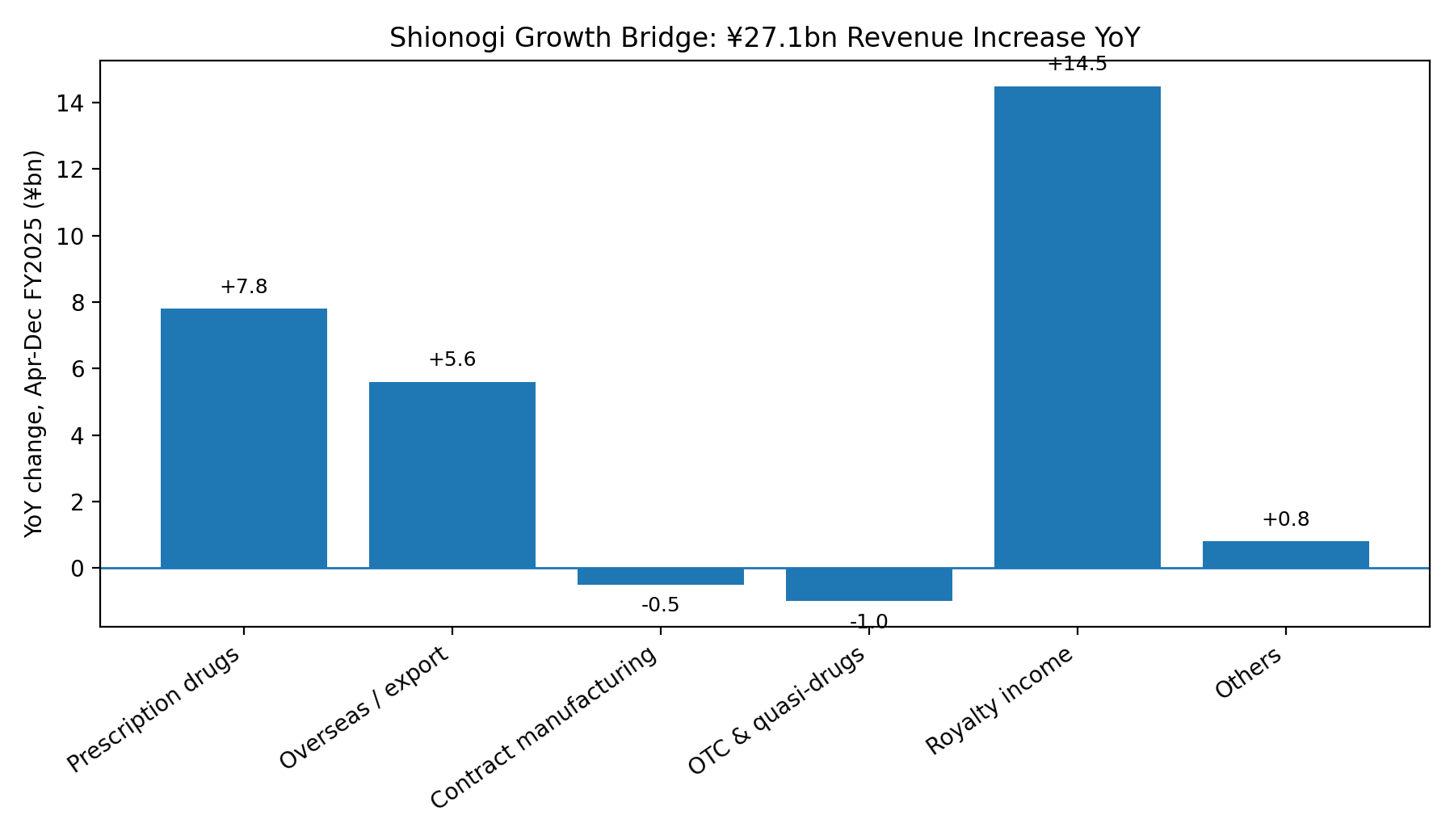

Figure 3 — YoY revenue growth bridge

There are three visible legs to the setup:

First, Shionogi increased its economic interest in ViiV Healthcare to 21.7%, while GSK retained 78.3%. ViiV issued new shares to Shionogi for $2.125bn, and Pfizer exited its holding.

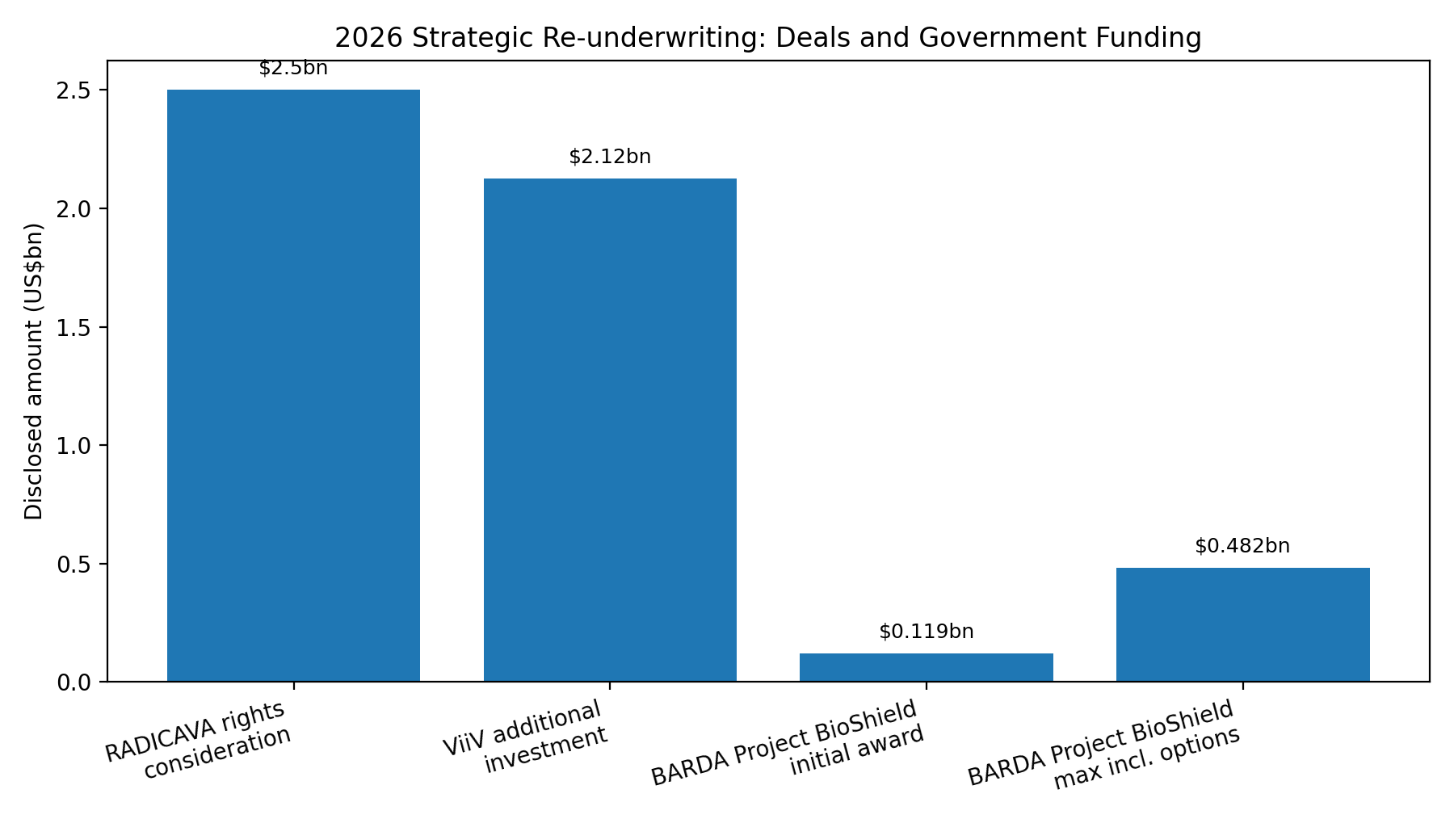

Second, Shionogi completed the acquisition of global rights to RADICAVA for $2.5bn. The company says the transaction should be immediately accretive in FY2026 and add roughly $700mn in annual global sales. RADICAVA is approved for ALS, and RADICAVA ORS / IV RADICAVA have been used to treat more than 22,000 people with ALS in the U.S. to date.

Third, Shionogi received a BARDA Project BioShield contract for Fetroja / cefiderocol. The contract is initially funded at $119mn, with multiyear options up to $482mn, and includes U.S. manufacturing, procurement, and development work for infections caused by high-priority biothreat pathogens.

Figure 4 — Disclosed 2026 strategic transaction / contract amounts

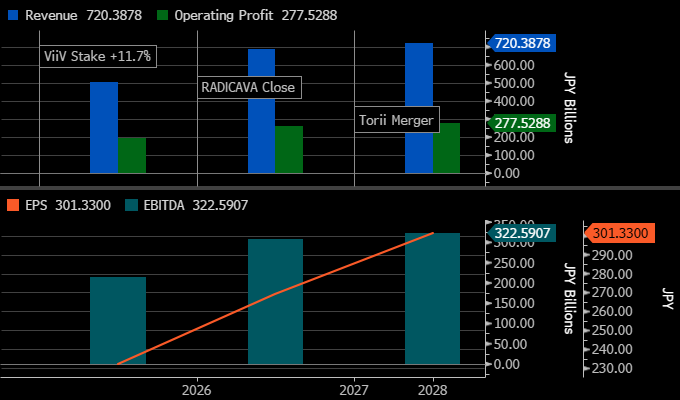

Is this disciplined reinvestment or balance-sheet dilution dressed up as strategy? Below is the pro-forma FY2026–FY2028 net debt / EBITDA and EPS accretion after ViiV, RADICAVA, JT / Torii, interest expense, amortization, and dividend policy.

Revenue steps up to ~¥720bn by FY2028 on RADICAVA, Torii, and ViiV, with operating profit ~¥278bn and EBITDA ~¥323bn; EPS reaches ~¥301, still lagging EBITDA as interest and amortization come through after the ~$4.5bn of deals. The shape here points to disciplined reinvestment: earnings scale and if leverage trends down and cash flow follows into FY2028, the step-up holds.

Causal Mechanism

The mechanism is simple enough to write on one line:

HIV cash flow funds control-like economics and U.S. commercial capacity; if those acquired assets produce stable earnings, Shionogi’s multiple should attach to a longer-duration base, rather than a fading royalty stream.

The ViiV leg is the cleanest. GSK reported 2025 HIV sales of £7.687bn, up 11% CER, driven by Dovato, Cabenuva, and Apretude. Long-acting medicines contributed more than 75% of total HIV growth in 2025, with Cabenuva contributing 55%. Cabenuva sales reached £1.402bn, up 42%, and Apretude sales were £439mn, up 62%. So Shionogi’s HIV economics are not just legacy royalty tailwind. The product mix is shifting toward long-acting treatment and prevention. It’s likely the HIV line can remain durable for longer than a “mature royalty” model implies.

The RADICAVA leg is different. It is not just another product line. It gives Shionogi an operating footprint in U.S. rare disease. The company’s December acquisition announcement explicitly framed the deal as a way to create a U.S. rare-disease commercial platform that can support future launches, including Fragile X syndrome, Jordan’s Syndrome, and Pompe disease programs.

The AMR leg is smaller but strategically useful. Antibiotics are usually difficult businesses because stewardship caps volume and reimbursement is uneven. Government procurement changes the shape of the economics. BARDA is not a guarantee of a blockbuster. It does, however, make Fetroja more than a hospital-sales story; it becomes part of a national preparedness budget.

The JT / Torii transaction rounds out the domestic base. Shionogi agreed in 2025 to succeed Japan Tobacco’s pharmaceutical business, acquire Akros, and make Torii a wholly owned subsidiary. JT’s pharmaceutical business had fiscal 2024 net sales of ¥44.942bn. The strategic logic is not glamorous, but it is coherent: more small-molecule discovery capacity, more domestic breadth, and more non-infectious-disease exposure.

The whole story depends on one discipline test: acquired earnings must be good enough to offset the loss of balance-sheet purity.

Timeline

At this point, everything is in motion, but the next guide and actual execution is the real event. May 12 is the next report. If the FY2026 bridge is clean, the story re-rates. If not, it stalls.

Key Risks

1. The balance sheet has changed

Shionogi disclosed ¥300bn of bridge borrowing for the ViiV investment and said total bridge loan financing reached ¥660bn when combined with the RADICAVA-related bridge loan. The company plans to refinance into mid- to long-term financing by the repayment deadline, and said FY2027 impact was still being examined. The stock’s old appeal included excess cash and low financial complexity. The new appeal requires confidence in management’s capital allocation.

2. RADICAVA must be more than acquired revenue

RADICAVA adds scale and U.S. rare-disease infrastructure, but ALS is a hard market. The acquisition price is $2.5bn, and Shionogi may pay additional royalties on future sales. The deal can work, but it needs durable sales and follow-on use of the commercial infrastructure. Otherwise, the market will treat it as bought growth rather than strategic extension.

3. Xocova / respiratory revenue is volatile

The acute respiratory virus treatment line fell from ¥43.3bn to ¥27.3bn in Apr–Dec FY2025, down 37.0%. That includes Xocova, Xofluza, and Rapiacta. This is the clean bear argument against over-capitalizing Shionogi’s infectious-disease optionality: outbreak-linked revenue is not the same as a durable annuity.

4. AMR is strategically important but commercially awkward

The BARDA contract is positive, but antibiotics remain structurally unusual assets. Stewardship limits volume by design. Government procurement helps, but it also means timing, funding, and manufacturing obligations matter. Fetroja also carries a label history that includes an observed increase in all-cause mortality in certain critically ill patients in a study versus best available therapy; Shionogi’s own U.S. safety language flags this issue.

5. The next guide can disappoint even if the strategy is right

FY2026 guidance has to absorb multiple moving parts: ViiV accounting, RADICAVA sales, financing cost, amortization, JT / Torii consolidation, U.S. SG&A, and dividend policy. A messy bridge could delay the re-rating even if the long-term logic is sound.

Conclusion

The old Shionogi thesis was balance-sheet quality plus HIV royalties.

The new Shionogi thesis is capital allocation.

That makes the stock more interesting and less forgiving. The company is no longer just collecting from ViiV and paying dividends. It is increasing its ViiV exposure, buying U.S. rare-disease infrastructure, consolidating domestic assets, and pushing antimicrobial resistance into a procurement-backed model.

The strongest version of the thesis is straightforward: ViiV’s long-acting HIV cycle extends the royalty base, RADICAVA adds near-term sales and U.S. commercial capability, and BARDA turns Fetroja into a strategic asset with government demand. In that version, the market moves away from viewing Shionogi as a static royalty story and begins valuing it as a higher-duration specialty pharma cash-flow compounder.

The weakest version is just as clear: management spent a pristine balance sheet at the wrong time, Xocova fades, RADICAVA under-earns, and the pro-forma guide forces investors to model more debt, more amortization, and less simplicity.

The May 12 guide will be very important because it will show which version investors have to underwrite.