Hard Power, Hard Cash

The Industrialization of Deterrence

Table of Contents

Executive Summary: Overview of the defense industrial cycle and Hard-Power Basket.

Macro Context: The Industrialization of Deterrence: Global spending trends, NATO normalization, and supply-chain bottlenecks.

Bristow Group (VTOL): Vertical-lift logistics and resilience infrastructure.

Hyundai Rotem (064350 KS): Integrated armor and rail manufacturing.

Creotech Instruments (CRI PW): Sovereign satellite and orbital systems.

Conclusion: Equally weighted across air (VTOL), land (Rotem), and orbit (Creotech).

Executive Summary

Defense spending is entering an industrial phase. Across NATO and the Pacific, budgets are expanding and production lines are running at capacity. Foundries, avionics, and heavy-lift logistics are now the critical inputs for deterrence, and demand visibility stretches years ahead. The market is still focused on AI, but the more durable opportunity possibly sits in the companies rebuilding the physical infrastructure of defense.

Hard-Power Basket includes Bristow Group (VTOL), Hyundai Rotem (064350 KS), and Creotech Instruments (CRI PW), three firms positioned to compound through this defense industrial cycle. Each represents a different layer of the rebuild: air mobility, armored transport, and orbital communications.

Macro Context: The Industrialization of Deterrence

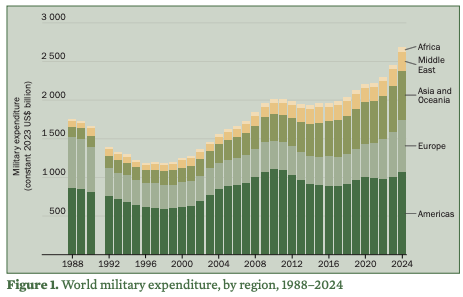

Rearmament has become a global capex cycle. Military expenditure reached $2.72 trillion as of 2024, up 9.4% yoy and 37% higher over the decade, the fastest sustained build-up in decades.

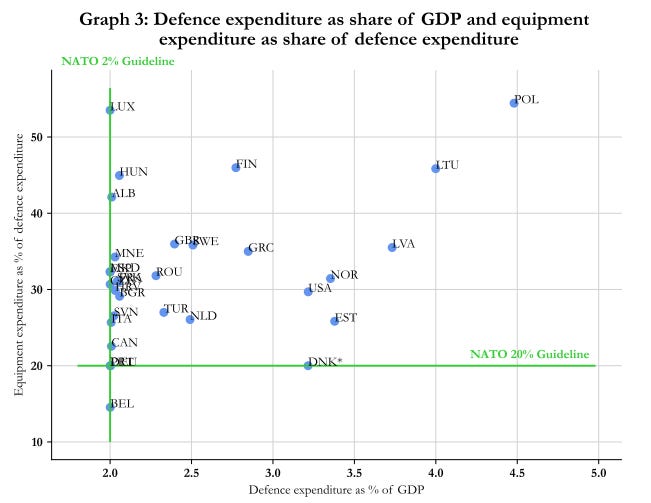

By the end of this year, all 32 members are expected to meet the 2% of GDP defense target, with Poland and the Baltic states above 3%, locking in multi-year procurement pipelines.

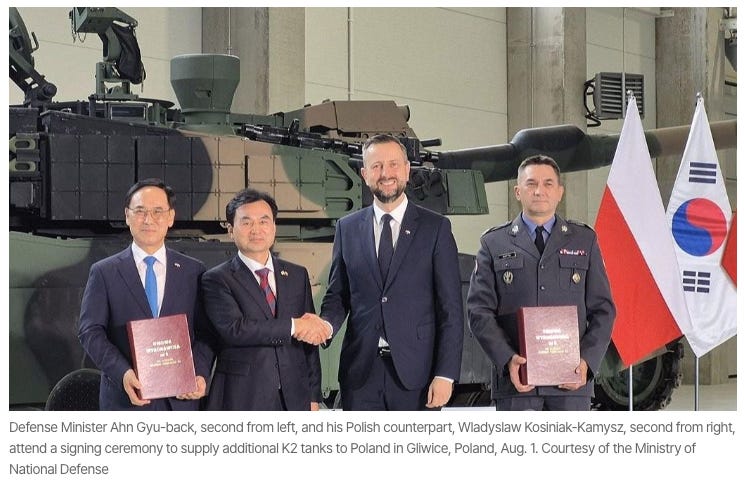

South Korea has become a key arsenal for Europe, delivering tanks, self-propelled howitzers, and rocket systems on tight schedules. Export volumes are tracking record highs this year.

Casting, avionics, railcar, and logistics suppliers are running near capacity. Lead times are stretching, and certified operators are beginning to gain pricing power as bottlenecks persist. In addition, defense logistics now overlaps with offshore wind, search-and-rescue, and satellite infrastructure, reducing cyclicality.

Our view: The “long defense” trade has moved past the primes. The alpha sits with Tier-2 enablers that turn sovereign policy into delivered capability, firms positioned at the intersection of manufacturing, logistics, and autonomy.

Bristow Group (VTOL)

Bristow operates one of the most advanced vertical-lift fleets in the world and remains the only independent operator with full global certification for government and offshore missions. Its competitive edge lies in scale, the world’s largest S-92 fleet, and in the hard infrastructure of trust: safety record, pilot training, and maintenance capability. The model is sticky; when a government contracts search-and-rescue, it stays with the same partner for decades. An example of this is the UKSAR2G rollout expanding Bristow’s footprint across the U.K. and Northern Europe, anchoring multi-year logistics revenue under government backing. At the same time, its offshore energy work is stabilizing as projects add to flight hours.

In addition, the partnership with Vertical Aerospace gives the company early exposure to eVTOL operations, a natural extension of its mission profile.

Essentially Bristow is evolving from an oilfield service legacy into the backbone of resilience logistics, emergency response, defense support, and offshore infrastructure. Few operators combine its regulatory clearances, pilot bench, and operational safety history. The next leg of growth comes from scaling these competencies into a global platform for industrial and sovereign missions.

Hyundai Rotem (064350 KS)

Rotem is Korea’s integrated manufacturer for both rail and armored systems, a dual capability that gives it a unique advantage as nations rebuild industrial capacity. The company produces the K2 main battle tank and high-speed rolling stock from a single engineering base, supported by the Hyundai and Hanwha industrial ecosystem. That combination of defense credibility and civilian manufacturing scale allows Rotem to deliver faster and at lower cost than European peers.

The landmark K2 program in Poland is now the anchor of Europe’s armor renewal. Localized production at Gliwice will embed Rotem inside Europe’s supply chain, creating a template for follow-on orders from other NATO members. Parallel wins in rail, including the record ONCF contract in Morocco, keep the company’s backlog balanced across sectors and geographies.

Rotem’s strength is in its ability to move quickly from design to delivery. Korea’s export model, government financing, proven equipment, and flexible transfer-of-technology, is giving it a structural foothold in markets once dominated by Western primes. As Europe re-industrializes its defense base, Rotem stands out as the supplier building both the tracks and the tanks.

Creotech Instruments (CRI PW)

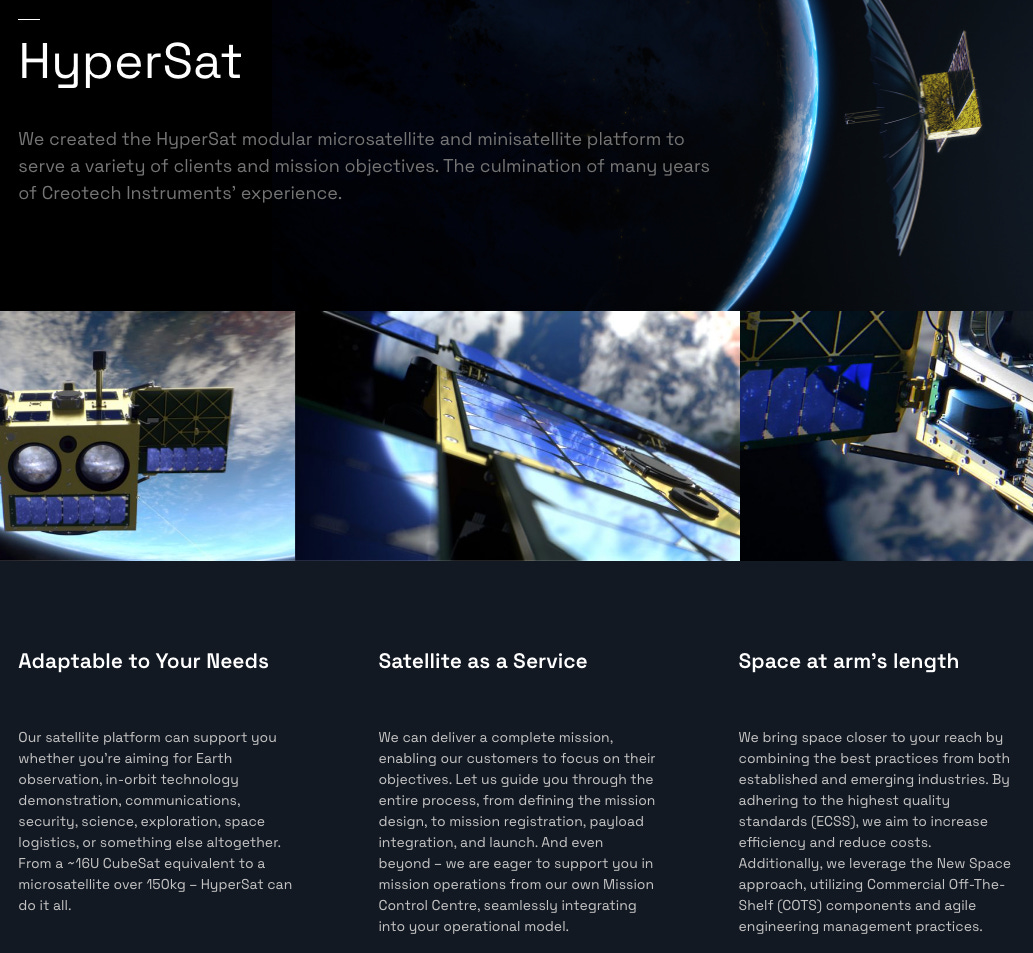

Creotech is Poland’s leading satellite integrator and one of the few European firms capable of building complete small-sat systems, from electronics to ground control, under ESA certification. Its HyperSat platform is modular, flight-proven, and fully owned, positioning the company at the center of Europe’s push for strategic autonomy in space.

The CAMILA constellation and the MIKROGLOB defense program have turned Creotech into a sovereign supplier. Together, these contracts align the company with Europe’s own shift toward independent launch and observation capacity.

Creotech’s moat is technological sovereignty. It builds the subsystems Europe no longer wants to import, onboard computers, power units, and integration services for national constellations. As satellite demand moves to security, Creotech has already become one of the continent’s default providers.

Conclusion

The Hard-Power Basket holds Bristow (VTOL), Hyundai Rotem (064350 KS), and Creotech Instruments (CRI PW), operators building the air, land, and orbital layers of modern deterrence. The sleeve runs at 0.7% of NAV, sized for a cyclical but durable policy-driven uptrend. Positions are equally weighted (~0.23% each) to balance exposure across transport, armor, and space until the theme matures.

Disclaimer:

This publication is for educational and informational purposes only. Any performance referenced is illustrative and tracked on a per-article basis, not as part of a model portfolio or investment program. Nothing herein constitutes investment advice, a recommendation, or a solicitation. → Ridire Research Substack Disclaimer