Megawatt Mutiny

Backing the hardware & fuel that liberate us from grid choke-points

America’s electricity still flows through a hand-full of fragile chokepoints: ~55,000 high-voltage transformers with an average age of 38 years and replacement lead-times of 12-24 months (DOE LPT report, 2024). A wildfire, cyber exploit or simple aging failure at a single substation can black out 100,000+ households. Meanwhile geopolitical risk has re-priced industrial policy: Washington now pays companies to on-shore batteries (IRA 45X), offers loan guarantees for new HVDC lines, and backstops the first small-modular-reactor (SMR) deployments. Our basket is built to monetize that structural rewiring:

Local batteries to decouple homes, EVs and datacenters from distant peaker plants.

Buried or subsea HVDC to harden bulk power corridors.

Modular fission to supply always-on generation without sprawling cooling towers.

Edge intelligence: micro-grid controllers, smart meters, and protection devices, to stitch the decentralized mesh together.

Each core holding owns an engineering bottleneck, IP, certification or scale that slower peers cannot replicate quickly, while the moonshots deliver convex optionality on single-point breakthroughs such as laser enrichment or island-scale hybrid plants.

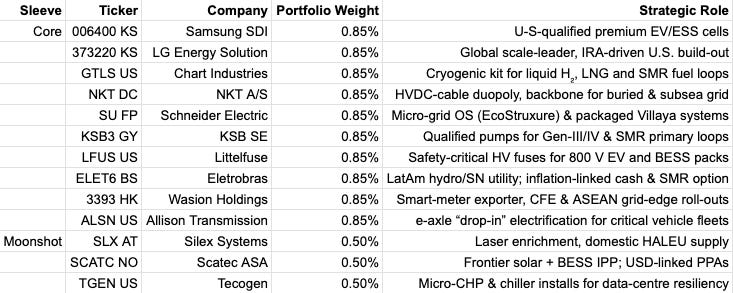

Core Sleeve Rationale

Samsung SDI (006499 KS) – Premium Chemistry

GM’s joint-venture with Samsung SDI will pour US $3.5b into a New Carlisle, Indiana gigafactory, ramping 27 GWh expandable to 36 GWh by 2027. The facility will churn out nickel-rich prismatic and 46-series cylindrical cells that qualify for the US$35 kWh 45X manufacturing credit, adding roughly 10 percentage points of gross margin versus Chinese imports. SDI’s cobalt-lean Gen-5 NCA already commands a price premium: energy density lets OEMs shave 40 kg per pack, while its next-gen solid-state roadmap (pilot lines 2027) preserves that edge. In short, SDI’s moat blends materials IP with first-wave IRA economics; every incremental U.S. production line both locks in margin and inoculates GM from CATL dependence.

LG Energy Solution (373220 KS) – Sheer Scale as Competitive Gravity

LGES targets 540 GWh global capacity by 2025, second only to CATL. That scale commits suppliers (separator, cathode, electrolyte) on take-or-pay contracts, flattening input volatility and granting LGES bargaining power that sub-50 GWh peers lack. Capex is largely pre-funded through IRA ATVM loans and customer co-investment (Honda, Stellantis, Hyundai), so equity dilution risk is minimal. Critically, 41% of planned capacity sits in North America, assuring IRA credits and derisking geopolitically. For the decentralization theme, LGES is the mass-volume guarantor that EV and stationary-storage build-outs can actually materialize onshore.

Chart Industries (GTLS) – Cryogenic Gatekeeper

Hydrogen may be light, but storing it colder than -253 °C is heavy engineering. Chart commands >800 liquid-H₂ tanks already deployed and, per the Q1 2025 report, backlog just crossed US $5.14 billion, its first time above five billion. Orders span LH₂ rail tenders, nuclear isotopic storage and marine bunkering, tapping three orthogonal growth vectors. The company’s brazed-aluminium heat-exchanger patents and field-service network (required every five years under CGA H-3) create a razor-and-blade model: 45% of revenue is aftermarket at ~34% EBITDA margin. No other western vendor offers the same breadth of cryogenic SKUs, giving Chart a gatekeeper role whenever H₂ or small-reactor helium loops show up in a project spec.

NKT A/S (NKT DC) – Cable Duopoly with a Vessel Hedge

Europe’s energy transition is constrained not by turbine blades but by copper cores. NKT closed Q1 2025 with a €10.7 billion high-voltage backlog and still quotes 2028 lead-times on XLPE HVDC. The moat is regulatory as much as technical: only three manufacturers (NKT, Prysmian, Nexans) are type-tested to 525 kV DC polymer insulation. NKT differentiates further by owning its own cable-lay ships and trenchers, shielding project schedules from the current tight spot-market for installation assets. As the EU mandates meshed offshore grids and the U.S. approves Atlantic HVDC corridors, NKT’s capacity scarcity translates directly into multi-year pricing power.

Schneider Electric (SU FP) – Software-Defined Micro-Grids

Villaya Flex, launched 2024, packages inverters, BESS, diesel hybrids and the EcoStruxure Microgrid Advisor EMS, cutting design-to-commissioning lead-time by 50% for off-grid communities. Unlike hardware-only rivals, Schneider monetizes a recurring software layer, license + data subscription worth ~8% of system ASP, and locks customers into its parts catalogue for 20-year maintenance. The result is SaaS-like stickiness inside an industrial conglomerate: gross margin on digital energy climbed from 37% (2021) to 42% (2024). As hospitals, airports and data-centres demand island-mode capability, Schneider’s fully integrated stack is becoming the default “easy button” for CFOs.

KSB SE (KSB3 GY) – Nuclear Pump Certification as High Barrier

Liquid-metal SMRs require pumps that survive 430 °C lead coolant without external seals. In January 2025 KSB signed an LOI with Swedish developer Blykalla to supply the SEALER reactor primary pumps. For context: there are fewer than five vendors worldwide certified for conventional PWR primary loops; for lead-cooled fast reactors, KSB is effectively first. Each reactor fleet expects three decades of spares and service, locking in annuity-like revenue once the first units enter operation around 2029. Meanwhile, KSB’s existing PWR/GWR pump installed-base ensures stable cash while it rides the SMR wave.

Littelfuse (LFUS) – Design-In Economics in 1,500 V Architectures

Every EV battery management system must interrupt 800 – 1,000 V DC faults within microseconds. Littelfuse’s newly launched AEC-Q200-qualified 823A fuse brings 1kV rating to a 5 × 20 mm SMD package. Once a fuse is designed into an EV platform the OEM would face a 9-to-12-month UL re-qualification cycle and ~$200k re-tooling to switch suppliers, classic stickiness. Littelfuse’s high-voltage automotive segment is growing double-digits despite the broader electronics slowdown. As battery pack voltages ratchet towards 1,500 V for faster charging, Littelfuse’s portfolio widens the total dollar content per vehicle and per stationary storage rack.

Eletrobras (ELET6 BS)– Inflation-Protected Hydro Cash, SMR Optionality

Post-privatisation, Eletrobras cut head-count 22% and aims for R$13 billion opex savings by 2027 (company roadmap). Brazil’s May 2025 Provisional Measure 1,300 opens the free power market and mandates tariff recalibration by July 2026, effectively index-linking Eletrobras’ 29 GW hydro portfolio to inflation while freeing it to contract directly with SMR developers for firming capacity. The result: defensive cash flows now, long-dated upside through new-build nuclear participation once a domestic SMR framework is finalised.

Wasion Holdings (3393 HK) – Emerging-Market Meter Trojan Horse

In June 2025 Wasion Mexico secured a MXN 623 million smart-meter order from CFE, raising cumulative contract value above MXN 2.08 billion (≈US $121m). By localising assembly in Nuevo León the company dodges CFE’s 20% import penalty and out-scores western meter vendors on localization criteria. Smart meters are the vanguard for demand-response programmes; once installed, Wasion upsells concentrators and edge compute modules, deepening its margin stack. ASEAN utilities (TNB, PLN) are replicating CFE’s template, giving Wasion a pathway to triple export revenue without relying on China’s slowing domestic AMI market.

Allison Transmission (ALSN) – Drop-In Electrification for Critical Fleets

Fire-trucks, refuse haulers and defense vehicles need torque, range and reliability, not passenger-car drivetrains. Allison’s eGen Power 100S axle has been selected by Oshkosh/McNeilus for North America’s first zero-emission refuse truck. The axle bolts into conventional chassis rails, letting municipalities electrify fleets without redesign. Allison’s aftermarket network (1,400 service points) ensures lifetime uptime, a service moat unmatchable by EV start-ups. ICE transmissions still fund >US $0.6b FCF annually, underwriting R&D and shielding shareholders from the capital burn typical in clean-tech pivots.

Moonshot Sleeve – Convex Asymmetry

Silex Systems (SLX AT) owns the only western-ready laser enrichment tech. TRL-6 demonstration began 9 May 2025; management expects “hundreds kg of 19.75% HALEU” by YE25. DOE’s HALEU Availability Program earmarks US $3.4b for first movers, one offtake contract would dwarf Silex’s opex.

Scatec ASA (SCATC NO) operates 4.2 GW and has 2 GW under construction plus a 6 GW+ pipeline, lifting Q1 2025 proportionate EBITDA +48 % YoY and raising full-year guidance. 85% of cash flows are USD-linked, mitigating EM currency risk.

Tecogen (TGEN) reported Q1 2025 revenue +17.6% to US $7.3m, gross margin 44%, backlog US $10.8m with a surge in data-centre chiller orders. Edge-site CHP offers black-start capability when grid diesel fails, an increasingly valuable niche as AI campuses proliferate.

Key Positives for Narrative

Domestic policy tailwinds are no longer theoretical: production-tax credit cheques are clearing, and order books prove it. Samsung SDI’s and LGES’s U.S. plants embody Washington’s realpolitik that batteries must be made onshore, and the 45X credit effectively shifts 80% of cell manufacturing margin from Asia to Indiana and Arizona. Simultaneously, the private sector is voting with capex: Chart’s record US $5.14 billion backlog covers everything from NASA hydrogen systems to SMR helium loops, evidence that developers will spend on cryogenics once the supply chain exists.

At grid scale, regulators are taking the shovel. NKT’s €10.7 billion backlog equates to six years of factory utilization, reflecting a continental decision to route power through seabed cables rather than NIMBY-prone overhead lines, making buried infrastructure the new base case. Schneider captures the mirror image at the edge: its Villaya kits sell because community hospitals in Texas or telecom towers in Nigeria can’t afford 18-month transformer wait times.

In nuclear, KSB’s pump LOI with Blykalla and Silex’s TRL-6 test both target the Achilles heel of reactor scalability, qualified hardware and enriched fuel. If either fails, SMR timelines slip; if both hit, the ecosystem re-rates. Importantly, these milestones are funded: DOE cost-share for HALEU and European Union’s Euratom for fast-spectrum R&D reduce financial risk.

Finally, consumer-side electrification continues even in a cyclical downturn. Littelfuse is shipping 1 kV SMD fuses because EV battery architects are already designing 900+ V packs. Allison’s e-axle order with Oshkosh shows municipalities aren’t waiting for a perfect macro, they’re ordering now to meet zero-emission mandates in 2027.

Key Risks

Policy Reversal: A change in U.S. administration could dilute or repeal IRA 45X. Samsung SDI and LGES both carry covenant clauses to renegotiate JV economics; an abrupt repeal would compress cell margins.

Commodity Exposure: Copper and aluminum spot spikes squeeze NKT cable contribution spreads; while pass-through exists, working-capital swings could pressure FCF coverage of its Danish plant expansion.

Execution Slippage: Chart’s Brazed Aluminum exchanger plant in La Crosse is at 93% utilization, any weld rejection cascades into schedule penalties. NKT’s new XLPE extrusion line must pass type-test by Q2 2026 or incur liquidated damages on TenneT 2 GW contracts.

Technology: Silex must hit 19.75% enrichment assay under NRC surveillance; failure forfeits its place in the HALEU incentive queue. KSB’s lead-cooled pump faces untested corrosion regimes, if mean-time-between-repair is <10 years, SMR economics erode.

Emerging-Market Counterparty: Scatec’s Egyptian 1.1 GW solar project depends on EETC USD PPA adherence; currency controls could delay cash repatriation. Wasion’s CFE invoices hinge on Mexican budget cycles.

Conclusion

This 10% sleeve provides hard-asset inflation shelter, policy-backed growth, and technological convexity. It marries asymmetric catalysts, laser enrichment, frontier IPP gigaprojects, with durable compounders like Schneider and NKT whose order books stretch beyond 2030. Grid fragility is no longer an engineer’s lament; it is a capital allocation fact. Owning the assets that rebuild and decentralize the system is the highest-probability path to multi-cycle alpha.

Disclaimer:

Ridire Research is an independent research publication operated by Ridire Research LLC and affiliated with a private fund, an Exempt Reporting Adviser under the U.S. Investment Advisers Act of 1940. Ridire Research is not registered as an investment adviser and does not provide personalized investment, legal, accounting, or tax advice.Informational & Educational Purpose Only

All materials—including text, charts, model portfolios, and explicit labels such as “Buy,” “Sell,” “Hold,” “Long,” or “Short”—are published solely for general informational and educational purposes. They reflect the author’s views at the time of writing, derived from publicly available data, proprietary frameworks, and market analysis, and are not tailored to any reader’s specific objectives, financial situation, or risk tolerance. Subscription to this Substack does not create an adviser–client relationship with the affiliated private fund or its principals.

No Offer or Solicitation

Nothing herein constitutes (i) an offer to sell or the solicitation of an offer to buy any security or other instrument, (ii) a recommendation to participate in any investment strategy, or (iii) a solicitation for investment advisory services. Any references to trades, allocations, or vehicles should be viewed as hypothetical model illustrations only. Offers, if ever made, will be made solely by confidential offering documents and only to qualified investors in jurisdictions where permitted.

Potential Conflicts of Interest

The affiliated private fund, its affiliates, employees, and related accounts may hold, increase, decrease, initiate, or exit positions, long or short, in securities or digital assets discussed, without notice or obligation to update disclosures. Such positions may be inconsistent with views expressed in this publication. The affiliated private fund, related entities, and personnel may initiate, modify, or exit positions in any mentioned security before or after publication without further notice. We maintain internal policies, including trading blackout windows and conflict reviews, to mitigate potential conflicts of interest.

Accuracy & Forward-Looking Statements

Although we strive for accuracy and analytical rigor, information may become outdated and may contain errors or omissions. Forward-looking statements, projections, or target prices are inherently uncertain and may differ materially from actual results. No warranty, express or implied, is given as to completeness, accuracy, or reliability.

Risk Acknowledgment

Investing involves substantial risk, including the potential for complete loss of capital. Past performance, whether actual, indicated by back-tests, or modeled, is not indicative of future results. Securities, derivatives, and digital assets mentioned may be illiquid, highly volatile, or subject to regulatory change.

Reader Responsibility

Readers should conduct their own due diligence, consider their personal circumstances, and consult a licensed financial professional before acting on any information contained herein. By reading this publication you agree that Ridire Research LLC, the affiliated private fund, and their affiliates accept no liability for any direct or consequential loss arising from reliance on the information presented. This research is not directed at persons in jurisdictions where such distribution would be contrary to local law.

I think NKT's total addressable market is restricted to Europe's offshore build out. Which, although ambitious, isn't enough to sustain NKT's now c25 P/E multiple. For one the EU's plan is to halve the per annum rate of GW offshore capacity construction from the 2030s to the 2040s. I explain my long term sell perspective on NKT's valuation here - https://carbonconclusions.substack.com/p/nkt .