Not Your Last NAND Cycle

AI inference, NL-HDD substitution, and disciplined supply are rewriting the earnings path.

Affiliation Disclosure & Disclaimer:

The managing principal of Ridire Research is affiliated with a private investment fund that holds long positions in the securities discussed herein (Kioxia Holdings, 285A JP), which could influence the views expressed. This publication is for educational and informational purposes only. Any performance referenced is illustrative and tracked on a per-article basis, not as part of a model portfolio or investment program. Nothing herein constitutes investment advice, a recommendation, or a solicitation. → Ridire Research Substack Disclaimer

Table of Contents

Executive Summary – A Different NAND Cycle

Mix shift, improved earnings quality, and balance sheet repair within a tight supply backdrop.Company Overview – Enterprise-Weighted Model

Revenue composition, manufacturing control, and the Gen8 transition.The Setup – Operating Leverage and Cash Conversion

Price and volume strength, inventory discipline, and revised JV economics.Causal Mechanism – Earnings Path Upgrade

Enterprise mix expansion, supply discipline, node transition, JV compensation, and cash compounding.Timeline

JV extension, Gen8 production crossover, enterprise SSD qualification, and CY2026 supply outlook.Key Risks

Cycle normalization, AI demand variability, consumer weakness, execution, accounting transition, and FX.Conclusion – Structural De-Risking

Less about peak margins, more about sustained earnings quality and capital structure improvement.Special Note:

KIOXIA perpetual contract expected to launch.

Executive Summary

Kioxia (285A JP) is operating from a position of strength in a genuinely tight NAND backdrop. Pricing is firm, bit shipments are expanding, and the operating leverage is translating directly into cash. Q3 FY2025 revenue reached a record ¥543.6bn, non-GAAP operating income was ¥144.7bn (27% margin), and free cash flow was +¥85.7bn, the eighth consecutive quarter of positive FCF. Net debt-to-equity has been reduced to ~80%, materially improving the balance sheet profile. But the more important point isn’t really that “NAND is strong.” It’s more what Kioxia is doing with the strength and how it could exit this cycle.

Two things stand out:

Enterprise SSD is now the center of gravity. In SSD & storage, management described the mix as roughly ~60% data center/enterprise and ~40% PCs/other, with data center/enterprise volume and revenue both at record highs (AI server demand plus higher unit prices).

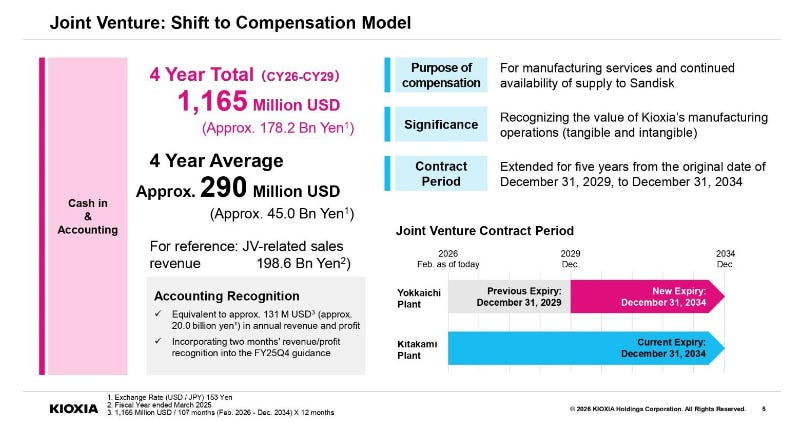

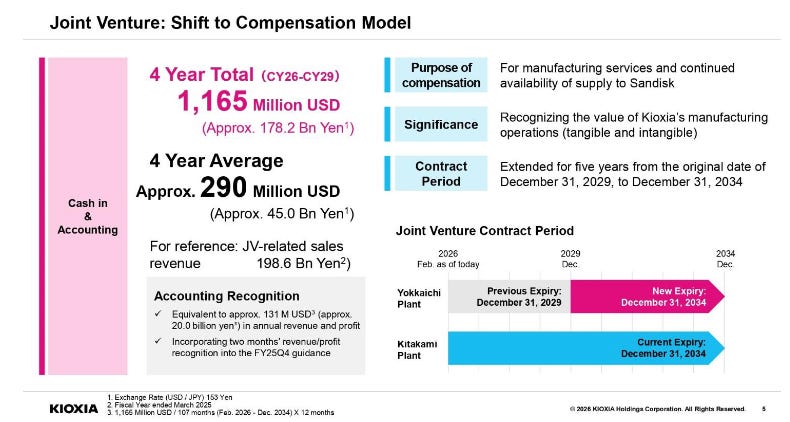

The SanDisk JV economics have been rewritten in Kioxia’s favor. Kioxia will receive $1.165bn in cash consideration over 2026–2029 (about $290m/year on average) and recognizes ~$131m/year of additional revenue from Feb 2026–Dec 2034 and management explicitly said this revenue contributes directly to operating profit. Historically, ~¥200bn/year of SanDisk-related revenue was effectively booked “at cost.” Simply put this changes the quality of earnings.

Guidance is aggressive and importantly specific. For Q4, revenue is guided to ¥845–935bn and non‑GAAP operating profit to ¥440–530bn, with unit pricing expected to increase significantly across applications, total shipments down, and data center/enterprise SSD mix up. Full-year FY2025 guidance calls for record revenue (¥2.1798–2.2698tn) and record non‑GAAP operating income (¥717–807bn). The trade is simple to state: if the company is right that CY2026 stays tight, then Kioxia is easily upgrading mix, upgrading earnings quality, and de‑risking the balance sheet at the same time.

Company Overview

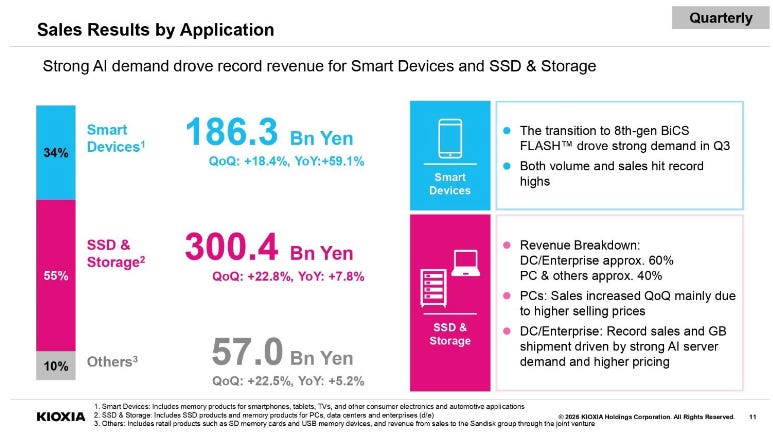

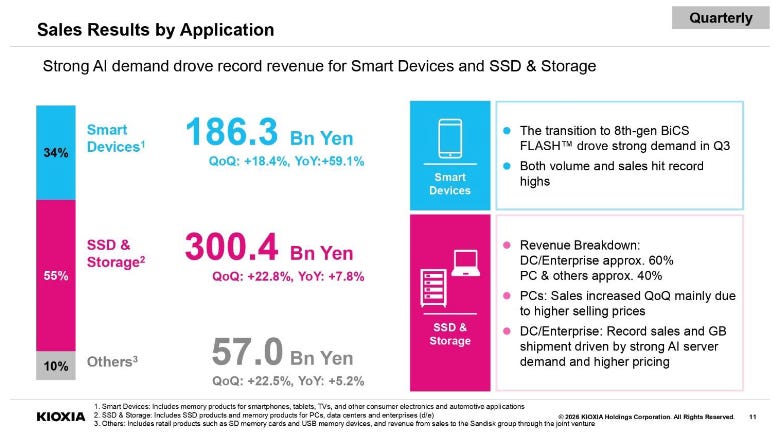

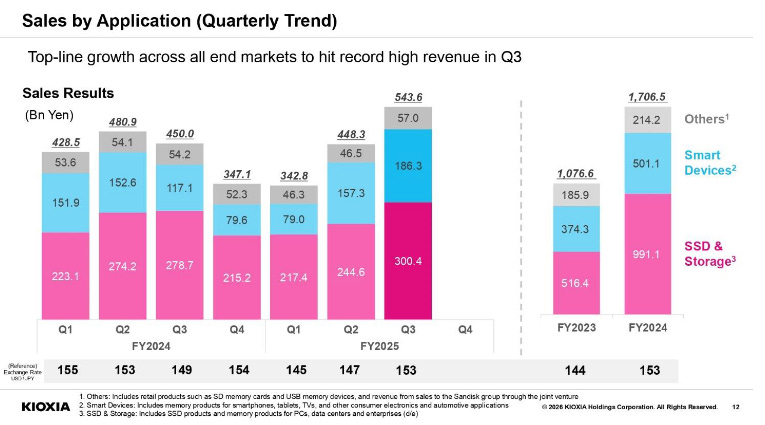

Kioxia is a NAND manufacturer with three practical revenue buckets: Smart devices, SSD & storage, and Other (which includes B2C products like SD cards and revenue from sales to SanDisk recorded via the manufacturing JVs). Management noted all three categories delivered record revenue in Q3.

In Q3 FY2025:

Smart devices (smartphones/tablets): ¥186.3bn, 34% of total revenue, up 18.4% QoQ, helped by the Gen8 BiCS FLASH transition that “began in earnest” in Q2 and continued through Q3.

SSD & storage: ¥300.4bn, 55% of total revenue, up 22.8% QoQ. Within this, management pegged the split at roughly 60% data center/enterprise / 40% PCs & other.

That 60/40 call matters because it’s management telling you what’s driving the margin profile: the incremental bit demand is moving toward enterprise sockets (qualification, endurance, performance-per-watt, controller/firmware tuning), not just consumer clearing prices.

On operations, they’re making a point of control: Kioxia says it controls 100% of wafer manufacturing at the Yokkaichi and Kitakami plants and independently manages procurement, automation optimization, cycle-time reduction, lead-time reduction, and yield management. That’s the “why” behind the confidence in investment efficiency and manufacturing competitiveness.

The Setup

In Q3 both price and volume moved higher. Unit pricing firmed again sequentially, but just as importantly, gigabyte shipments expanded, led by data center and enterprise demand. In memory, simultaneous price and volume strength is usually a signal of genuine supply tightness rather than short-term channel behavior.

Free cash flow remained solidly positive, leverage continued to decline, and the balance sheet is materially stronger than it was a year ago. Inventory trends tell a similar story. Days declined meaningfully, consistent with demand running ahead of supply and disciplined production execution.

Layered on top of the operating momentum is the revision to the SanDisk joint venture. What had historically been revenue recognized largely at cost now incorporates explicit consideration and margin-accretive recognition over time.

Guidance maintains the same posture: firm pricing, improving enterprise mix, and further profitability expansion.

Causal Mechanism

The first mechanical shift is mix. AI workloads are pulling NAND demand toward enterprise and data center sockets, where qualification cycles are longer, density requirements are higher, and product selection is less price-elastic. Management’s view is straightforward: data center and enterprise demand for AI applications is driving NAND growth, and near-term demand is expected to exceed supply into CY2026.

Importantly, the demand base is not singular. Enterprise growth is supported by three overlapping vectors: ongoing conventional server replacement, sustained AI inference deployment, and supply constraints in nearline HDD that encourage substitution into high-capacity QLC SSDs. Even if AI sentiment cools tactically, HDD availability and density economics can continue to shift bits toward enterprise SSD adoption. The demand story is therefore broader than a single AI capex cycle.

Demand alone, however, does not create earnings durability. Supply discipline does. The company expects market bit growth to remain in the mid-teens this year and upper-teens next year, while acknowledging ongoing capacity constraints. The implication is that the industry is not responding with aggressive capacity additions that would immediately compress pricing. Tightness converts mix into margin.

Overlay the product cycle. The transition to 8th-generation BiCS FLASH is progressing, with Gen8 expected to become the mainstay production node by fiscal year-end, while investment in subsequent generations continues. That sequencing is critical. Cost reductions and competitive positioning are advancing during the upcycle, not deferred to a downturn. It provides margin defense when pricing inevitably moderates.

Then there is the structural revision to the SanDisk joint venture. The shift toward explicit consideration and margin-accretive recognition through 2034 reframes part of what had historically been throughput economics. Management positions this as reflecting the strategic and technological value embedded in Kioxia’s manufacturing and development capabilities.

The practical result is improved cash visibility and higher-quality earnings. Higher-quality earnings compound through the balance sheet. Net D/E has already compressed meaningfully over the past several quarters, driven by sustained free cash flow and retained profitability. In prior cycles, leverage amplified volatility when conditions softened. Today, improving capital structure reduces the reflexive downside that has historically characterized memory equities.

The mechanism, therefore, is layered and put simply what changes the earnings path is:

Enterprise mix expansion → tight supply backdrop → node transition supporting cost structure → improved JV economics → sustained cash generation → balance sheet repair.

Timeline

Jan 30, 2026: Yokkaichi JV extended through end‑2034; $1.165bn consideration over 2026–2029; revenue recognition Feb 2026–Dec 2034 (~$131m/year).

End of CY2025: shipment of 122TB and 245TB SSD models for customer qualification (high‑capacity 2Tb QLC on Gen8 BiCS FLASH).

End‑March 2026: Gen8 expected to surpass Gen5 in production ratio and become the mainstay product.

Q4 FY2025: IFRS requires lump-sum recording of ¥12bn in property taxes for the full year (recorded in Q4); management says profit growth is expected to “significantly” exceed that headwind.

CY2026 (company view): NAND supply/demand expected to be very tight in the near term, driven by data center demand.

Key Risks

The NAND cycle risk doesn’t go away.

This is still a commodity industry at the core. The real risk is supply responding faster than expected (or demand pulling forward so hard that you get a digestion pocket). Management’s own strength in Q4 guidance implicitly raises the question: is this a peak quarter? Obviously not our view but still a reasonable question.

AI inference demand can wobble.

Kioxia is leaning on sustained AI inference and AI server demand as a driver for record data center/enterprise results. If hyperscalers pause deployments, or storage attach rates disappoint, enterprise SSD mix can normalize faster than investors expect.

Consumer sets are a real watch item.

Management flagged that in smartphones and PCs, there’s a shift toward higher-end AI models, but total sets may decline due to rising costs. If that turns into outright unit weakness, it can still pressure the broader NAND pricing umbrella.

Execution on Gen8 ramp.

The company expects Gen8 to become the mainstay product by end‑March 2026. Any yield, utilization, or transition inefficiency shows up quickly in gross margin, especially if ASP momentum decelerates.

JV optics / accounting noise.

Moving from “revenue at cost” toward explicit compensation improves economics, but it can create reporting quirks and confusion for generalist investors. The risk is the market misreads the income statement during the transition period.

FX and financing sensitivity.

Q3 benefited from FX tailwinds (JPY 153/USD vs 147 in Q2), and refinancing reduced interest cost. Both can reverse.

Conclusion

The easy take is “NAND upcycle.” The better take is that Kioxia is using the upcycle to change its shape.

Enterprise SSD is becoming the profit engine (and management is talking in enterprise terms: qualification, high-capacity QLC, data center sockets).

The SanDisk JV revision adds a contractual layer of cash consideration and margin-accretive revenue recognition that should make earnings less purely spot-driven over time.

Cash generation is not a slide-deck claim anymore, eight straight quarters of positive FCF and a net D/E ratio down to ~80% is a tangible de-risking path.

What needs to stay true for the thesis to work is also clear: pricing can’t roll over immediately, enterprise mix needs to hold, and Gen8 needs to ramp cleanly into mainstay production by fiscal year-end. If those three hold while the JV cash begins flowing (2026–2029), Kioxia exits this phase with a materially improved balance sheet and a higher-quality earnings base, exactly the combination that changes how cyclicals get valued.

Special Note:

Trade.xyz secured the KIOXIA listing via the HIP-3 auction, committing 515.64 HYPE (~$24k USD), which is burned upon settlement. At current pricing, this is a non-trivial expenditure for a single ticker, particularly with the perpetual not yet live.