Optionality with Training Wheels

Capturing Sponsor-Led Upside with Trust-Floor Downside Protection

We’ve constructed a focused event-driven SPAC basket rooted in a core principle: when the structure itself limits your downside, you gain the freedom to allocate into asymmetric upside without overexposing risk capital. This is not a thematic SPAC punt, it's a rules-based allocation to pre-vote vehicles with embedded capital protection and sponsors with a credible record of dealmaking.

Each position is selected not for what it might become, but for what it already structurally is: a low-drag vehicle tethered to a known liquidation floor, with upside potential tied to the quality and optics of the eventual business combination.

Structural Setup

Pre-vote SPACs offer one of the few remaining examples of built-in convexity in public markets. Through the vote date, each SPAC maintains a hard capital floor, typically ~$10 per share, corresponding to cash held in trust. That means:

Downside is constrained by design

Upside is unlocked via credible deal announcements

Optionality is embedded, not implied

The value lies in the structure, not sentiment. We are not relying on broader market enthusiasm, we are simply allocating into a set of contracts where the worst case is known and the best case is reputation-driven, narrative-led repricing.

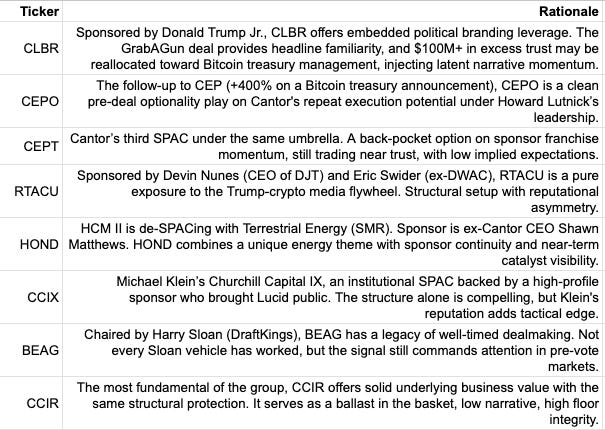

SPAC Arbitrage Basket

8 SPACs @ 0.25% each = 2.0% total exposure

Each selection meets three criteria:

Pre-vote status with intact trust floor

Strong or politically relevant sponsor network

Compelling asymmetric setup via potential deal optics or narrative power

Why It Belongs

Each name is a controlled asymmetric bet: you are either buying the sponsor's next act or the market’s mispricing of future narrative momentum. No leverage. No timing stress. No need to "believe."

When risk is limited and reward is reputational, the real game is how much you commit.

We’re not looking to ride the next SPAC mania, we’re looking to own clean convexity with a known floor and a catalyst-rich ceiling.

Risk Considerations

Sponsor Execution Risk – Not every name will announce a compelling deal. That’s why we diversify and stay pre-vote.

Post-Vote Collapse Risk – We avoid the decay phase by limiting to intact trust structures.

Narrative Fatigue – Many SPACs never regain attention. We prioritize sponsor lineage and reputational capital.

Market Illiquidity – Our sizing (0.25% per name) inherently controls for thin volume across names.

Conclusion

Optionality with Training Wheels is about applying discipline to chaos. It is one of the rare ways public equity investors can manufacture convexity without derivatives or leverage, just through positioning within contract structure and sponsor incentives.

Disclaimer:

Ridire Research is an independent research publication operated by Ridire Research LLC and affiliated with a private fund, an Exempt Reporting Adviser under the U.S. Investment Advisers Act of 1940. Ridire Research is not registered as an investment adviser and does not provide personalized investment, legal, accounting, or tax advice.Informational & Educational Purpose Only

All materials—including text, charts, model portfolios, and explicit labels such as “Buy,” “Sell,” “Hold,” “Long,” or “Short”—are published solely for general informational and educational purposes. They reflect the author’s views at the time of writing, derived from publicly available data, proprietary frameworks, and market analysis, and are not tailored to any reader’s specific objectives, financial situation, or risk tolerance. Subscription to this Substack does not create an adviser–client relationship with the affiliated private fund or its principals.

No Offer or Solicitation

Nothing herein constitutes (i) an offer to sell or the solicitation of an offer to buy any security or other instrument, (ii) a recommendation to participate in any investment strategy, or (iii) a solicitation for investment advisory services. Any references to trades, allocations, or vehicles should be viewed as hypothetical model illustrations only. Offers, if ever made, will be made solely by confidential offering documents and only to qualified investors in jurisdictions where permitted.

Potential Conflicts of Interest

The affiliated private fund, its affiliates, employees, and related accounts may hold, increase, decrease, initiate, or exit positions, long or short, in securities or digital assets discussed, without notice or obligation to update disclosures. Such positions may be inconsistent with views expressed in this publication. The affiliated private fund, related entities, and personnel may initiate, modify, or exit positions in any mentioned security before or after publication without further notice. We maintain internal policies, including trading blackout windows and conflict reviews, to mitigate potential conflicts of interest.

Accuracy & Forward-Looking Statements

Although we strive for accuracy and analytical rigor, information may become outdated and may contain errors or omissions. Forward-looking statements, projections, or target prices are inherently uncertain and may differ materially from actual results. No warranty, express or implied, is given as to completeness, accuracy, or reliability.

Risk Acknowledgment

Investing involves substantial risk, including the potential for complete loss of capital. Past performance, whether actual, indicated by back-tests, or modeled, is not indicative of future results. Securities, derivatives, and digital assets mentioned may be illiquid, highly volatile, or subject to regulatory change.

Reader Responsibility

Readers should conduct their own due diligence, consider their personal circumstances, and consult a licensed financial professional before acting on any information contained herein. By reading this publication you agree that Ridire Research LLC, the affiliated private fund, and their affiliates accept no liability for any direct or consequential loss arising from reliance on the information presented. This research is not directed at persons in jurisdictions where such distribution would be contrary to local law.