Own the Casino

Platforms That Earn the Rake

Executive Summary

Theme: Own the platforms that structurally profit from trading and investment activity.

Basket (equal-weight, long-only, 2% model portfolio allocation):

Monex Group (8698 JP)

iFAST (IFAST SP)

MarketAxess (MKTX US)

Intercontinental Exchange (ICE US)

IG Group (IGG LN)

These primary five companies are the casino owners of finance. They don’t speculate; they monetize volume, flow, and balances through fees, spreads, and subscriptions. Their moats are built on network effects, regulatory licenses, sticky client relationships, and scale infrastructure. Growth comes from electronification, retail adoption, new asset classes, and platform expansion.

Owning this basket is a way to consistently collect the “house edge” of global speculation and investing.

Bonus mentions: HYPE and CARDS.

Intercontinental Exchange (ICE): The All-Weather Operator

Moat: ICE combines exchange franchises, exclusive listings, and clearinghouses with a global data subscription business. Its NYSE listings are defensible because issuers value prestige, liquidity, and index inclusion; rivals can’t replicate that network. Clearinghouses create regulatory and capital moats, once a firm clears through ICE, switching is impractical. The data arm is sticky: risk managers, banks, and asset managers embed ICE’s pricing/indices into workflows, paying recurring fees regardless of volumes.

Why it’s “own the casino”: Every trade on ICE futures, every stock listed on NYSE, every data feed consumed, ICE collects a toll. It thrives in any market regime: volatility drives futures/derivatives activity, while calmer markets still pay for data, listings, and mortgages tech. ICE earns the casino rake whether traders win, lose, or sit on data subscriptions.

Growth opportunity: Digitization of mortgages (multi-trillion-dollar U.S. market), expansion in ESG/Carbon markets, and broadening fixed-income execution. ICE isn’t just the house, it’s building new casinos in adjacencies where it can transplant its model.

MarketAxess (MKTX): Network Effects in Bond Trading

Moat: MKTX’s moat is its liquidity network. By pioneering all-to-all credit trading, it became the natural venue where dealers and asset managers meet. Liquidity attracts liquidity, once open interest builds, switching costs are high because clients need depth, not just low fees. The platform is also a data monopoly in certain bonds: its pricing feeds are embedded across buy-side risk systems.

Why it’s “own the casino”: MKTX doesn’t take bond risk; it skims a commission on every match. It benefits from the structural electronification of a $30T+ market that is still <50% electronic. As volumes migrate, MKTX’s “take rate” applies to a growing pie. The house here is the digital bond pit, the more players enter, the more indispensable MKTX becomes.

Growth opportunity: Expansion in portfolio trading (bond baskets), emerging markets, and Treasuries. Each adds a new “game” to the casino, widening its rake. Its data and post-trade services reinforce stickiness, giving MKTX multiple ways to monetize participants.

IG Group (IGG LN): The Retail Trading House

Moat: IG benefits from regulatory licenses, risk management systems, and brand scale that are hard for new entrants to replicate. Its moat is statistical: most retail CFD and spread-bet traders lose money over time, but IG earns consistently from spreads, financing charges, and fees. Its technology stack and global licenses (20+ jurisdictions) create both barriers and trust.

Why it’s “own the casino”: IG is the literal casino in retail trading. It prices the tables (spreads), sets leverage caps, and manages risk. While some clients win occasionally, the aggregate flow reliably yields profits. Like a sportsbook or poker room, IG always takes its cut, and its risk systems hedge outliers.

Growth opportunity: Expanding in the U.S. (tastytrade options), onboarding younger equity investors via Freetrade, and upselling them into leveraged products. More games, more players, same house edge.

iFAST (IFAST SP): AUA-Based Fee Machine

Moat: iFAST’s moat is recurring AUA-based fees and sticky advisor relationships. Once assets are custodied on iFAST, moving them is cumbersome for advisors and clients. Its pension administration (Hong Kong ePension) locks in decades-long contracts. The platform also now embeds a digital bank, capturing cash balances with regulatory protection.

Why it’s “own the casino”: iFAST is the casino cage, every dollar of client assets generates a predictable “cut” via platform fees and fund trailers. Whether clients gain or lose on investments, iFAST earns the toll on custody, admin, and services. With pensions and banking, it extends this edge deeper into the financial stack.

Growth opportunity: Scaling Asian wealth flows, leveraging the HK ePension mandate, and building banking into a second profit engine. As more chips sit in the cage, iFAST automatically takes its cut.

Monex Group (8698 JP): Brokerage with Crypto Optionality

Moat: Monex has a diversified brokerage base in Japan/US and a stake in crypto exchange Coincheck. Its moat comes from licenses, existing client relationships, and distribution partnerships (e.g. NTT Docomo). While crypto revenues are cyclical, Monex’s traditional brokerage provides a stable fee floor.

Why it’s “own the casino”: Monex collects fees on retail stock trades, FX trades, and crypto activity. Especially in crypto, where most retail traders churn capital, Coincheck’s fee rake is textbook “house” economics. Monex itself doesn’t gamble on direction; it earns whether the client wins or loses.

Growth opportunity: Upside comes if crypto trading volumes rebound. A new bull cycle would dramatically lift Coincheck, giving Monex a high-beta boost layered on top of stable brokerage rake.

Common Traits Across the Basket

They sell shovels in a gold rush: volume, activity, or AUA expansion = higher fees, regardless of client outcome.

Structural moats: network effects (MKTX), regulatory licenses (IG, ICE, Monex), sticky platforms (iFAST).

Growth by adding new tables to the casino: new asset classes, new geographies, adjacent workflows.

Defensive compounding: high margins, recurring revenue, strong cash returns.

Bonus: On-Chain “Casinos”: HYPE & CARDS

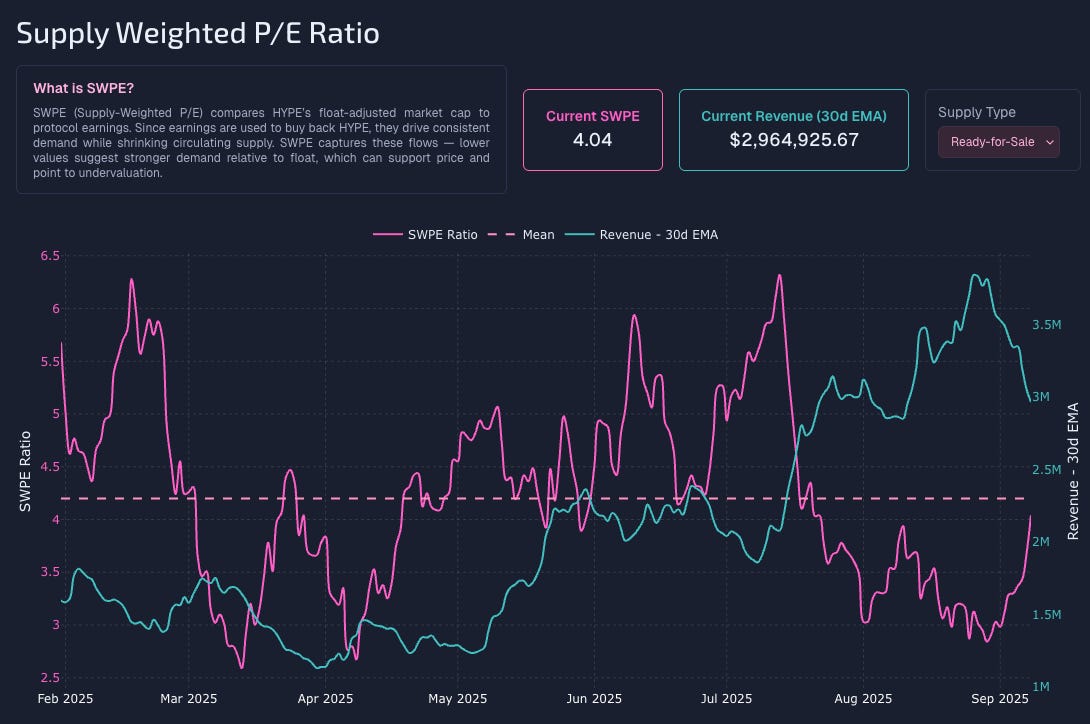

HYPE (Hyperliquid): A perp DEX where ~97% of fees are recycled into daily token buybacks. Trader fees and losses become permanent buy pressure, making HYPE a direct claim on the casino rake. What’s amazing is this trades at a low single digit (currently 4x) supply weighted P/E.

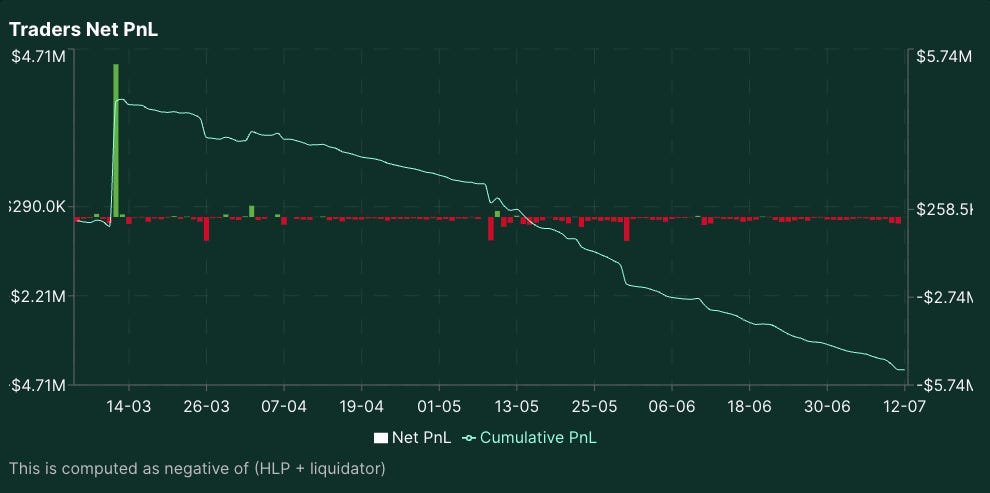

When you look at net trader P&L the thesis becomes obvious: most gamblers lose, so own the casino:

CARDS (Collector Crypt): A gacha model for Pokémon cards. Players sell back pulls at 85–90% of value; the 10–15% spread is the house edge used to buy/burn CARDS tokens. Player “losses” are systematically funneled into tokenholder gains.

For a thorough writeup on this token I recommend you read this piece by 0xKyle:

Both mirror the equities: activity → protocol rake → owner returns.

The risk: crypto cycles and regulatory scrutiny.

The lesson: whether regulated exchanges or on-chain casinos, the house wins.

Conclusion

Owning this basket means owning the economic infrastructure of speculation. Each company has a defensible moat ensuring it can keep charging fees, and clear growth vectors to expand its rake. In equities, bonds, retail trading, or crypto, the gambler may lose, but the house always collects.

Disclaimer:

Ridire Research is an independent research publication operated by Ridire Research LLC and affiliated with a private fund, an Exempt Reporting Adviser under the U.S. Investment Advisers Act of 1940. Ridire Research is not registered as an investment adviser and does not provide personalized investment, legal, accounting, or tax advice.Informational & Educational Purpose Only

All materials—including text, charts, model portfolios, and explicit labels such as “Buy,” “Sell,” “Hold,” “Long,” or “Short”—are published solely for general informational and educational purposes. They reflect the author’s views at the time of writing, derived from publicly available data, proprietary frameworks, and market analysis, and are not tailored to any reader’s specific objectives, financial situation, or risk tolerance. Subscription to this Substack does not create an adviser–client relationship with the affiliated private fund or its principals.

No Offer or Solicitation

Nothing herein constitutes (i) an offer to sell or the solicitation of an offer to buy any security or other instrument, (ii) a recommendation to participate in any investment strategy, or (iii) a solicitation for investment advisory services. Any references to trades, allocations, or vehicles should be viewed as hypothetical model illustrations only. Offers, if ever made, will be made solely by confidential offering documents and only to qualified investors in jurisdictions where permitted.

Potential Conflicts of Interest

The affiliated private fund, its affiliates, employees, and related accounts may hold, increase, decrease, initiate, or exit positions, long or short, in securities or digital assets discussed, without notice or obligation to update disclosures. Such positions may be inconsistent with views expressed in this publication. The affiliated private fund, related entities, and personnel may initiate, modify, or exit positions in any mentioned security before or after publication without further notice. We maintain internal policies, including trading blackout windows and conflict reviews, to mitigate potential conflicts of interest.

Accuracy & Forward-Looking Statements

Although we strive for accuracy and analytical rigor, information may become outdated and may contain errors or omissions. Forward-looking statements, projections, or target prices are inherently uncertain and may differ materially from actual results. No warranty, express or implied, is given as to completeness, accuracy, or reliability.

Risk Acknowledgment

Investing involves substantial risk, including the potential for complete loss of capital. Past performance, whether actual, indicated by back-tests, or modeled, is not indicative of future results. Securities, derivatives, and digital assets mentioned may be illiquid, highly volatile, or subject to regulatory change.

Reader Responsibility

Readers should conduct their own due diligence, consider their personal circumstances, and consult a licensed financial professional before acting on any information contained herein. By reading this publication you agree that Ridire Research LLC, the affiliated private fund, and their affiliates accept no liability for any direct or consequential loss arising from reliance on the information presented. This research is not directed at persons in jurisdictions where such distribution would be contrary to local law.

Excellent!

Any reason you didn’t include CBOE and CME group ?