Owning the Interface = Owning the User

Whoever controls the touchpoint controls the relationship, and the cash flow.

Executive Summary

Rising system complexity and “prosumer” workflows are turning branded hardware and connectivity moats into recurring cash-flow engines. Each of these firms monetizes the interface between infrastructure and experience, where trust, data, and performance create lock-in.

SNA is expanding beyond tools as diagnostic software and connected systems now outpace hardware growth, validating its shift toward subscription and workflow capture.

LMN SW is compounding through curated travel packaging, converting curation and fulfillment into higher margins and cash build even in a volatile consumer backdrop.

TMUS continues to leverage scale in network quality to lift ARPU and free cash flow through cross-sell (FWA, fiber) and cost-curve efficiency.

Across tools, travel, and telecom physical infrastructure becomes the substrate; recurring, data-rich monetization becomes the product.

Snap-on (SNA): Precision Tools Meet Recurring Workflow Capture

Thesis Summary:

Snap-on has long dominated the professional tool market, but the company’s real transformation lies in its shift toward data-driven diagnostics and recurring software revenues. Its Repair Systems & Information (RS&I) division now leads the growth and margin profile of the business, building off a proprietary dataset that includes over 500 billion diagnostics records and 1.2 billion repair outcomes. In an era where vehicles are increasingly complex, electric drivetrains, ADAS sensors, encrypted ECUs, Snap-on provides not just physical tools but the essential software layer technicians rely on to solve problems quickly and accurately.

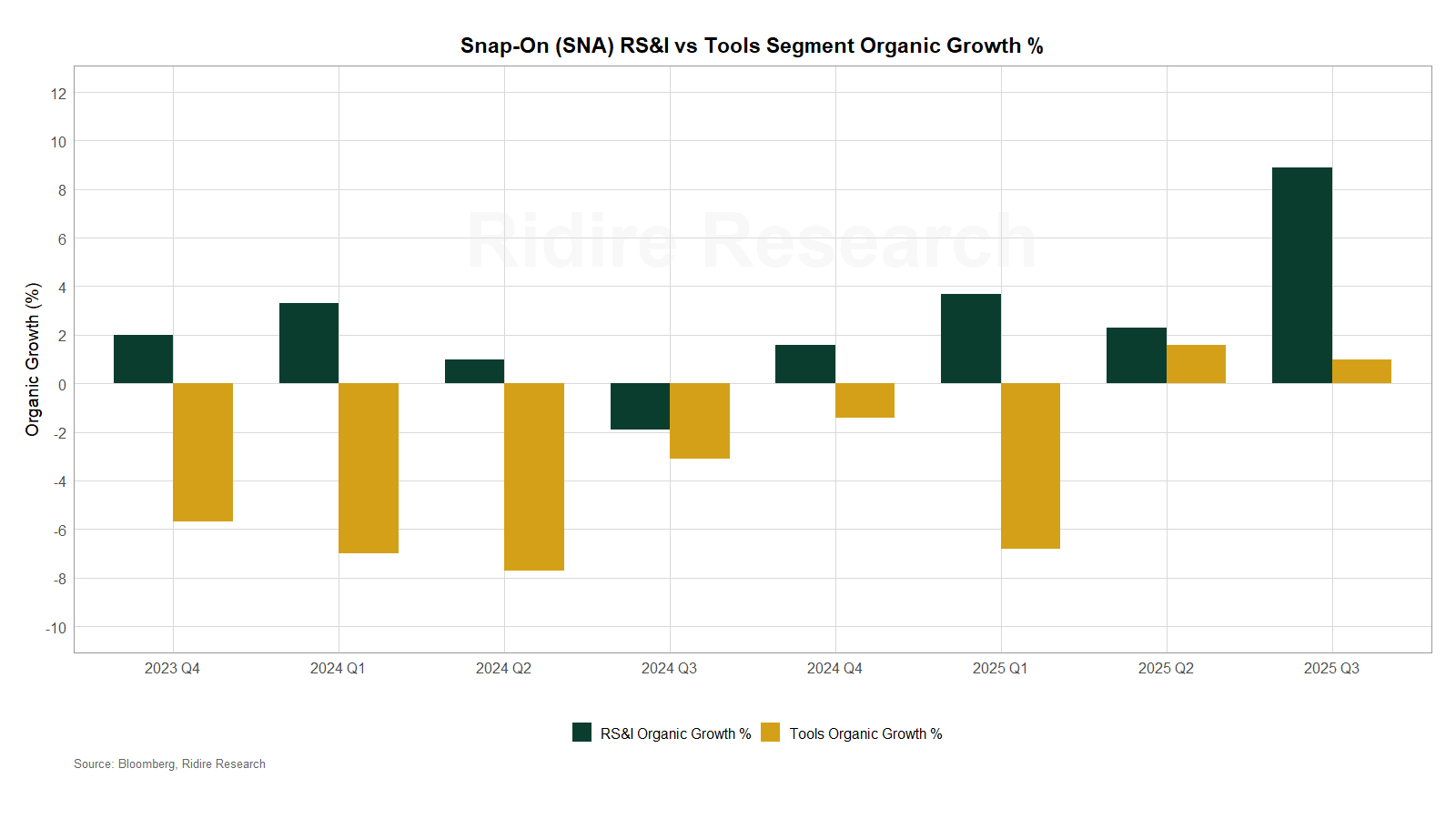

The market still treats Snap-on like a cyclical industrial toolmaker, but it’s increasingly a tech-enabled platform embedded in automotive and heavy equipment maintenance workflows. The RS&I segment has shown 8.9% organic growth in Q3 2025, far outpacing the 1% Tools Group growth. Its diagnostic tools and repair subscriptions, sold on proprietary hardware, have become embedded in independent shops and OEM dealerships alike.

Technicians now subscribe out of necessity, the RS&I software now covers 98% of vehicle types in the U.S., and its constant updates give Snap-on an edge in coverage and accuracy. This subscription model provides durable, high-margin recurring revenue (30%+ segment margin) and positions Snap-on as an irreplaceable node in the maintenance value chain.

Catalysts & Narrative:

Near-term upside could come from multiple directions:

Further growth in EV diagnostics (where Snap-on already offers specialty tools for battery and high-voltage systems)

Increased subscription attach rates as new features roll out.

Macro recovery unlocking deferred capex among independent mechanics.

There’s also a latent capital return angle, the company generates over $1B in annual FCF and maintains a strong balance sheet.

With management guiding toward continued high-single-digit RS&I revenue growth and multiple new product launches slated through 2026, we expect software-led narrative momentum to strengthen.

Key Risks:

EV repair mix could cannibalize some traditional tool demand over time.

OEM restrictions on diagnostics or increasing competition from software-first repair platforms could also compress Snap-on’s data moat.

In a macro downturn, tool purchases (especially big-ticket storage systems or lifts) may be delayed, which could drag on the legacy Tools segment even if RS&I proves resilient.

Lastminute.com (LMN SW): Curated Travel as Workflow Fulfillment

Thesis Summary:

Lastminute.com has repositioned itself as a travel fulfillment engine rather than a generic OTA. It does this by dynamically packaging flights, hotels, and ancillaries into bundled offerings that drive higher conversion, better margins, and stronger customer loyalty. With holiday packages now comprising more than 65% of revenue, LMN has turned curation into monetization, leveraging its legacy brand, a reengineered tech stack, and rising consumer demand for seamless value-focused travel.

Unlike OTAs that optimize for standalone flight or hotel inventory, LMN builds integrated bundles that abstract away the planning headache for customers. These packages have structurally higher take rates (~10%) and more pricing control. H1 2025 revenues were up 11% YoY, with Q3 revenue up 17% YoY and EBITDA up 35%. In addition, management has guided to continued margin expansion into 2026.

Strategically, the firm is broadening its channel mix through white-label deployments (ex. lastminute.ae in the Middle East) and enhancing its mobile stack to drive repeat usage. The recently installed CEO has stabilized governance post-controversy and laid out a clean multi-year roadmap.

Catalysts & Narrative:

Peak season travel demand and continued mix-shift toward packages should support top-line upside in Q4.

On the cost side, recent restructuring has already cut fixed costs by 5%:

With the 2025 buyback program complete and balance sheet in a net cash position, reinstatement of shareholder returns could catalyze re-rating.

Further expansion of loyalty offerings or mobile personalization could also reinforce customer lock-in and raise LTV.

Key Risks:

LMN remains a small-cap European name with legacy baggage, past governance issues still create institutional hesitation.

Travel remains macro-sensitive, especially for European discretionary spend.

Competitive intensity from Booking, Expedia, or eDreams (subscription model) could also pressure CAC and margin.

T-Mobile US (TMUS): Network Moat, Cash Engine, Subscription Flywheel

Thesis Summary:

T-Mobile continues to turn its 5G spectrum scale into a cash compounder. In Q3 2025, it added over 2.3M net postpaid subscribers and raised full-year guidance across nearly every metric. More importantly, it’s transforming from a growth-through-subs model to an ARPU-expanding, multi-service subscription business via FWA, fiber, and enterprise. With $4.8B in Q3 FCF and aggressive buybacks underway, TMUS is monetizing network dominance into shareholder value at scale.

T-Mobile’s mid-band 5G network is materially ahead of peers in speed and coverage, and independent tests continue to confirm this. That network edge underpins customer acquisition, churn suppression, and now ARPU growth.

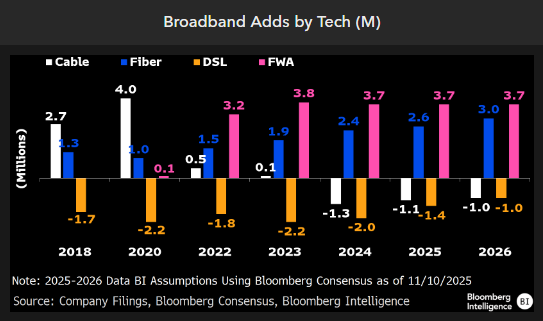

In parallel, T-Mobile is expanding its TAM via FWA (now 4M+ subs), and fiber (via partnerships with Lumos, Metronet). Meanwhile, enterprise wins and AI-driven CRM and pricing systems are enabling operating leverage.

This chart from Bloomberg Intelligence clearly illustrates how FWA has upended US broadband, intensifying competitive headwinds for cable operators:

Catalysts & Narrative:

We see a high-probability path to FY26 guide-ups as integration costs fade, synergy capture accelerates, and ARPU expands via upsell.

A further capital return announcement, or shift to a formal dividend growth policy, could expand the shareholder base.

Near-term, expect margin tailwinds from AI-enabled service stack upgrades (post-$350M billing system impairment) and more efficient network scaling.

Key Risks:

A potential price war (Verizon defensive moves) could pressure net adds and ARPU.

Integration missteps (US Cellular or fiber expansion) could delay synergy realization.

Regulators may scrutinize spectrum holdings if TMUS pursues more M&A or spectrum block wins.

Conclusion

This Tools & Interfaces basket (2% model portfolio weight, 0.66% each) targets recurring cash flows at the interface:

Snap-on (SNA): Diagnostic content layered onto a legacy moat of branded tools and proprietary distribution.

Lastminute.com (LMN SW): Curated travel packaging with defensible take-rates and strong conversion across bundles.

T-Mobile US (TMUS): Network ARPU/ARPA flywheel, now boosted by US Cellular integration and adjacent fiber scale-up.

Each name compounds at the intersection of trust, infrastructure, and embedded monetization.

Disclaimer:

This publication is for educational and informational purposes only. Any performance referenced is illustrative and tracked on a per-article basis, not as part of a model portfolio or investment program. Nothing herein constitutes investment advice, a recommendation, or a solicitation. → Ridire Research Substack Disclaimer