Peptide Overdrive

Why Radioligands and GLP‑1s Have Shifted the Sector from Boutique to Boomtown

Table of Contents:

Why Peptide Demand is Exploding

Tech Primer: Barriers That Create Moats

Company Specific Moats

Where Demand Meets Moats

Model Portfolio Allocation

Conclusion

Note: If the newsletter is truncated in an email, readers can click on "View entire message" and they'll be able to view the entire post in their email app.

1 | Why Peptide Demand Is Exploding

Metabolic megatrend (GLP‑1 drugs).

Weekly GLP‑1 analogues have shifted from a $6bn franchise in 2021 to more than $50bn in 2024 as prescribers embrace them for both diabetes and obesity.

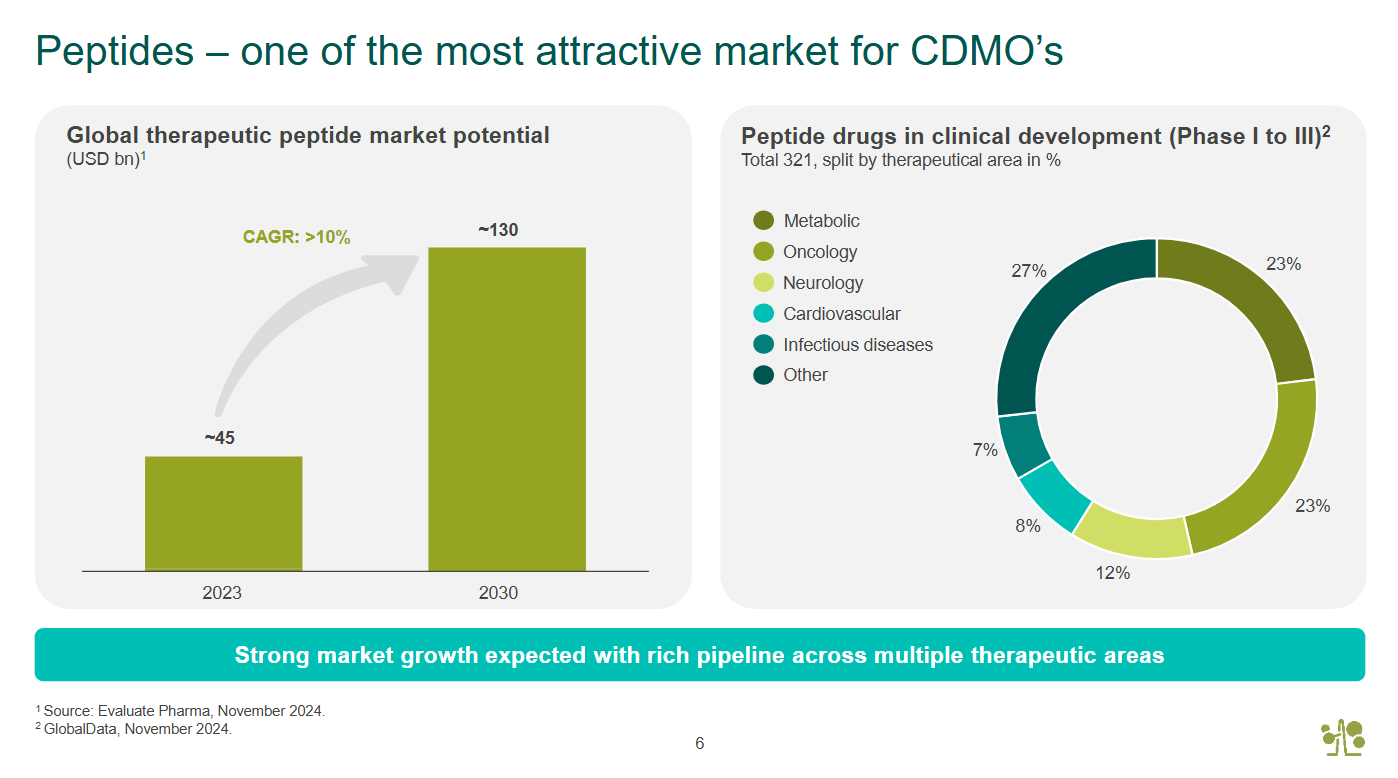

Consensus sell‑side models now pencil in $100 bn - $130 bn global sales by 2030, implying a >10% CAGR and multi‑ton annual API needs because every injection is a 39‑ to 44‑amino‑acid peptide.

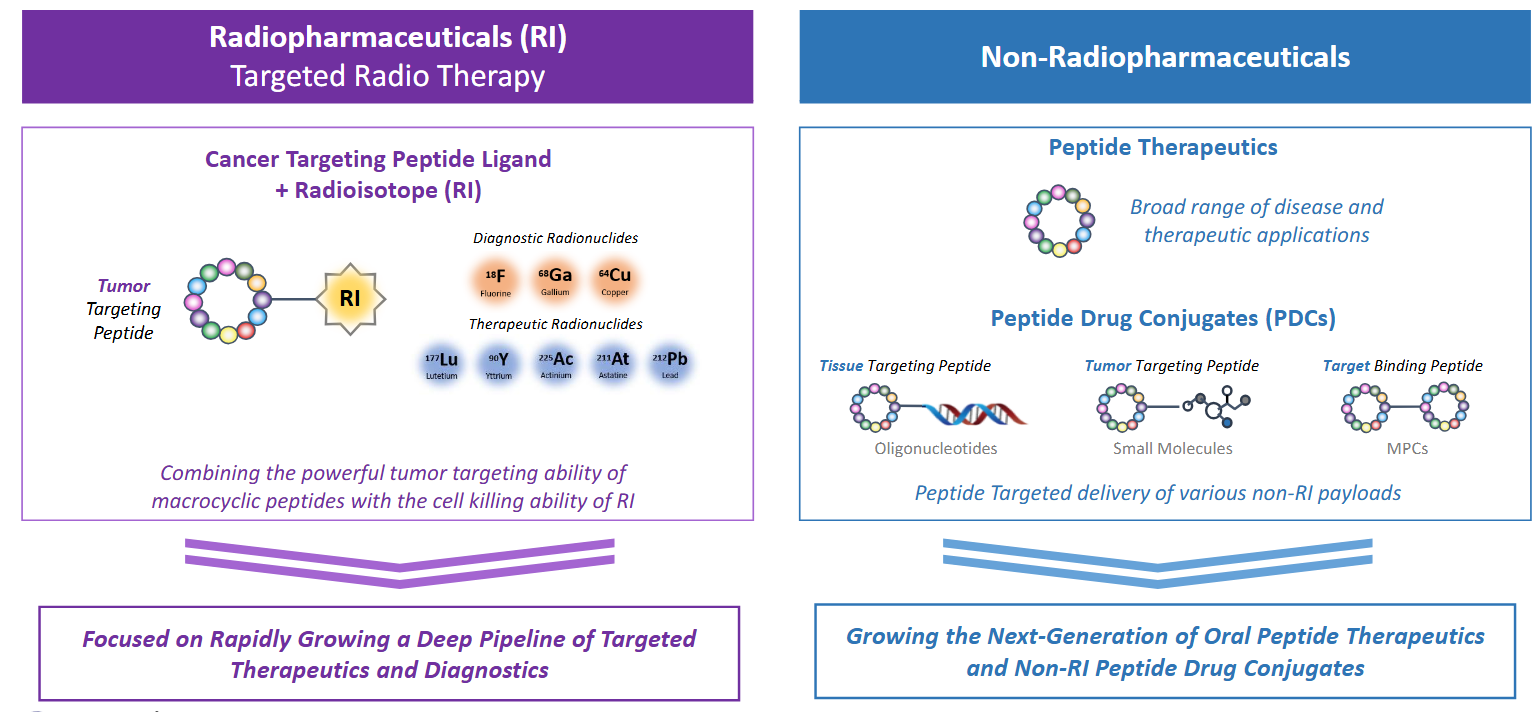

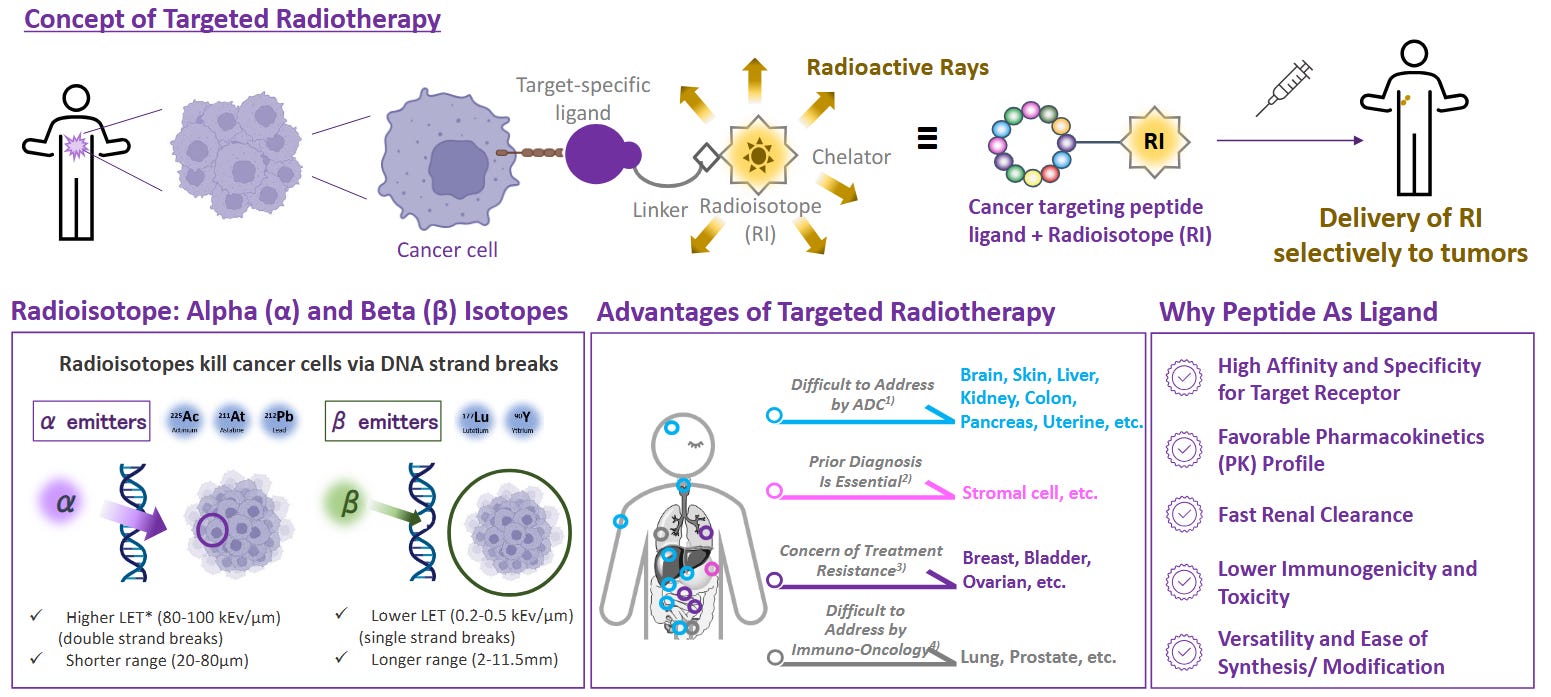

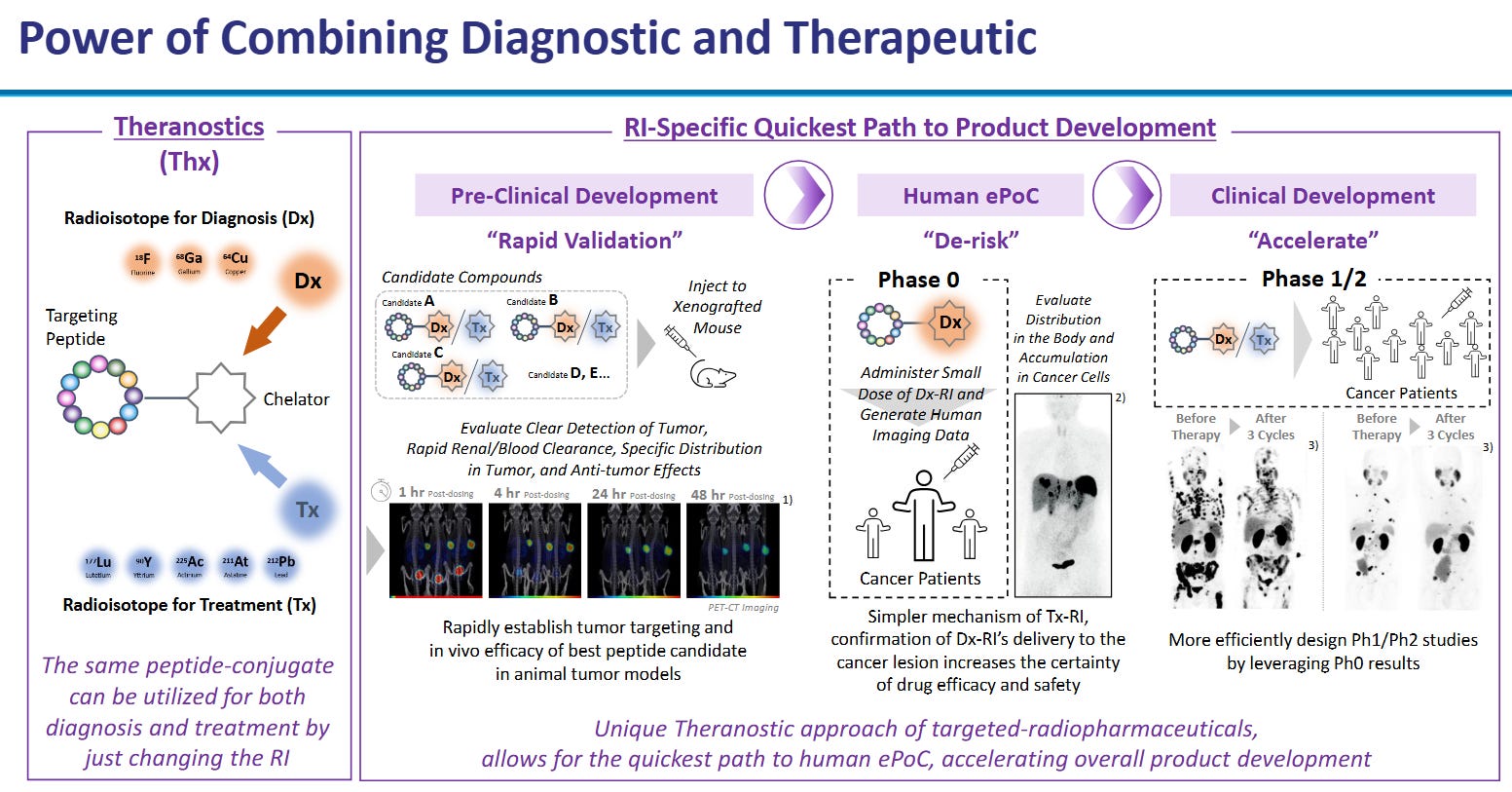

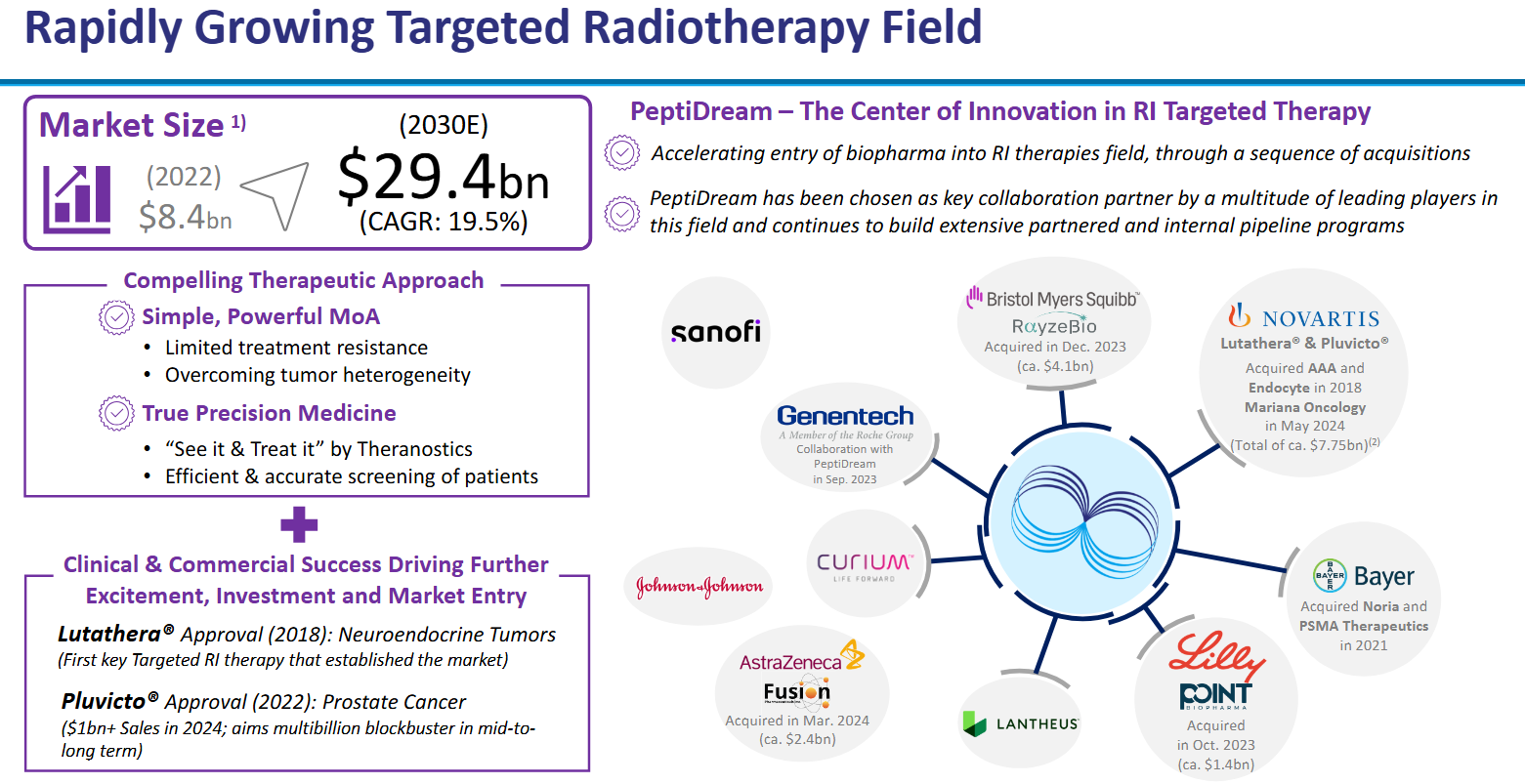

Radioligand therapy (RLT) flywheel.

Peptides that home to tumour receptors are conjugated to α‑ or β‑emitting isotopes, creating “smart bombs” for prostate, neuroendocrine, and solid tumours.

RLT revenue has crossed $2bn; big‑pharma has spent ~$10bn on acquisitions since 2022, guaranteeing a pipeline of new peptide vectors that must be synthesised under GMP.

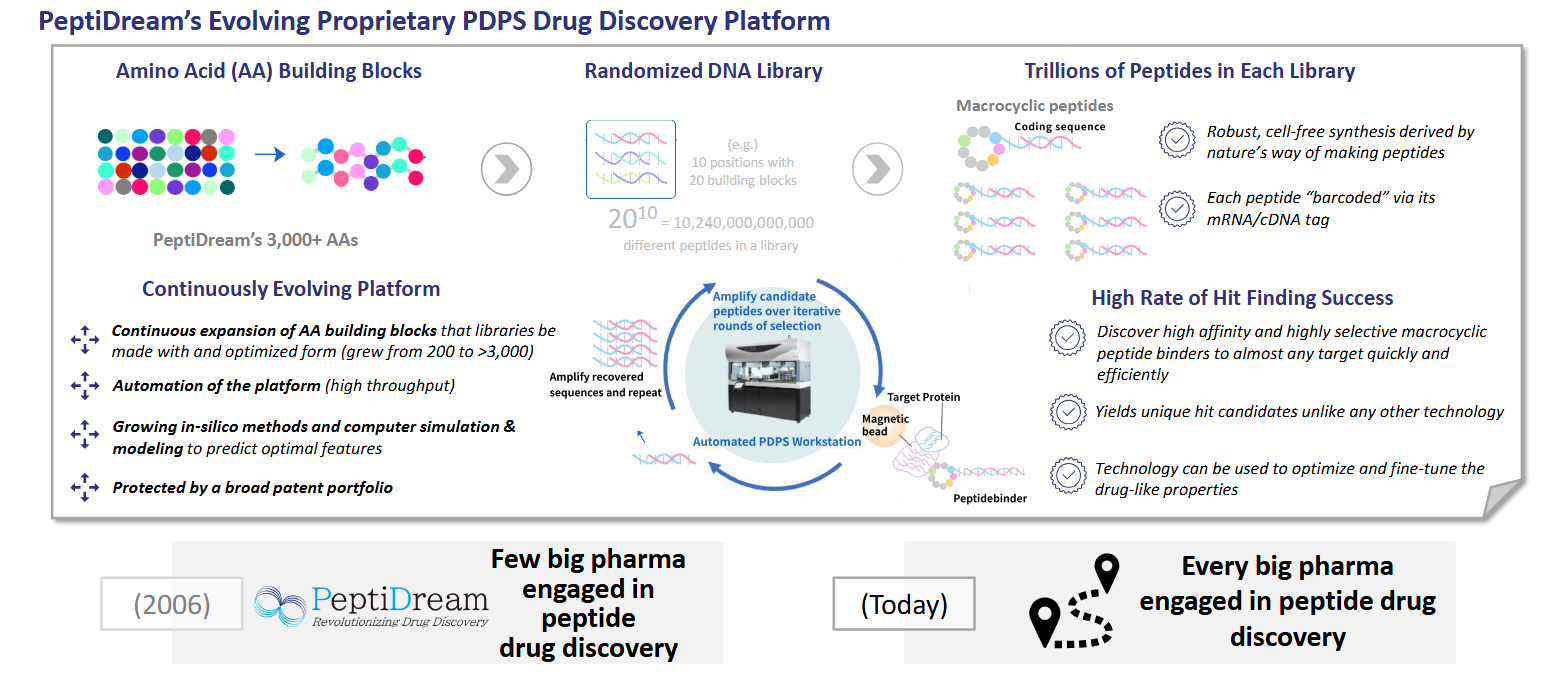

The following slides from PeptiDream give a fantastic overview:

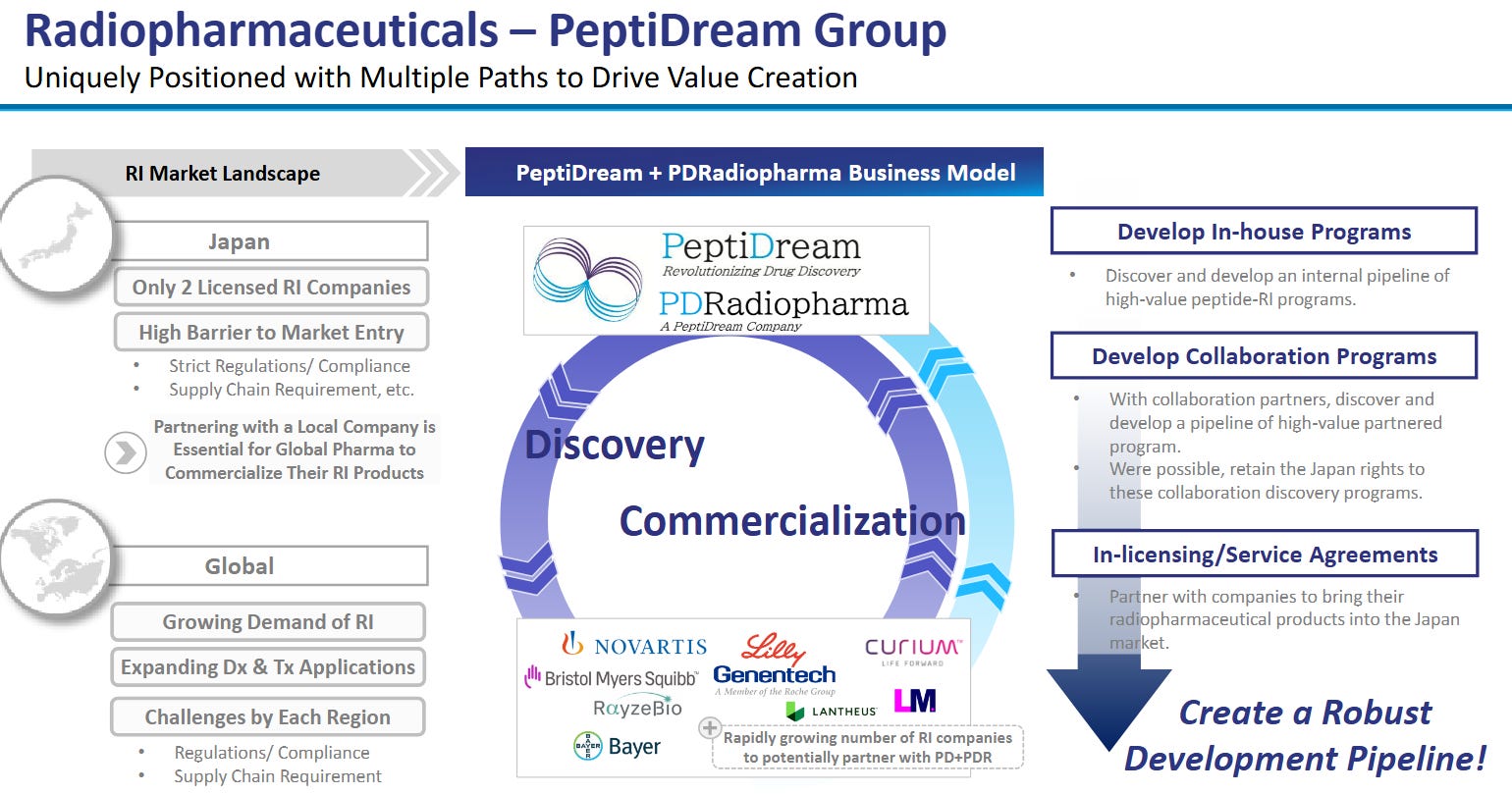

And finally, the flywheel:

Depot & adherence economics.

Long‑acting injectable (LAI) and microsphere depots stretch a dosing interval from daily to monthly, boosting adherence and payer willingness to reimburse.

Formulation advances also let peptides reach new tissues (e.g., sustained‑release exenatide crosses the blood‑brain barrier), expanding addressable indications.

Capacity bottleneck.

Legacy peptide plants were sized for gram‑to‑kilogram annual output; GLP‑1 demand alone now requires hundreds of kilograms per API per year.

Only a handful of Western CDMOs can run ton‑scale solid‑phase peptide synthesis (SPPS) under FDA/EMA standards, making qualified capacity the gating item rather than demand.

2 | Technology Primer — Barriers That Create Moats

Solid‑phase peptide synthesis (SPPS).

Peptides are built residue‑by‑residue on an insoluble resin; wash‑add‑deprotect cycles yield > 99 % stepwise fidelity and allow full automation.

Scaling from a 1‑g R&D batch to a 50‑kg commercial reactor requires deep process engineering (heat removal, solvent flow, in‑process analytics) and capital often north of $250m per site, capital many newcomers can’t rationalise.

Ton‑scale infrastructure.

A true ton‑scale facility combines multi‑1 000 L SPPS trains, continuous chromatography, solvent recycling, and tank farms for reagents and waste.

Because regulatory validation of a new plant can exceed 18 months, pharma locks capacity five years out via “take‑or‑pay” clauses, wedging competitors out of the near‑term pipeline.

Macrocyclic peptide libraries.

Ring‑locked peptides (often containing non‑canonical amino acids) bind flat protein surfaces and can cross membranes, tackling targets undruggable by antibodies or small molecules.

Generating trillion‑member libraries demands specialized ribosome engineering and IP; only a few platforms (notably PeptiDream’s PDPS) possess the chemistry, screening automation, and accumulated SAR data to do so at scale.

Depot microsphere technology.

Microspheres embed peptide crystals in biodegradable polymers that erode predictably, delivering zero‑order release over weeks.

The formulation know‑how, control of polymer molecular weight, particle size distribution, and solvent removal, is protected by composition‑of‑matter and process patents, creating licensing leverage for specialists like Peptron.

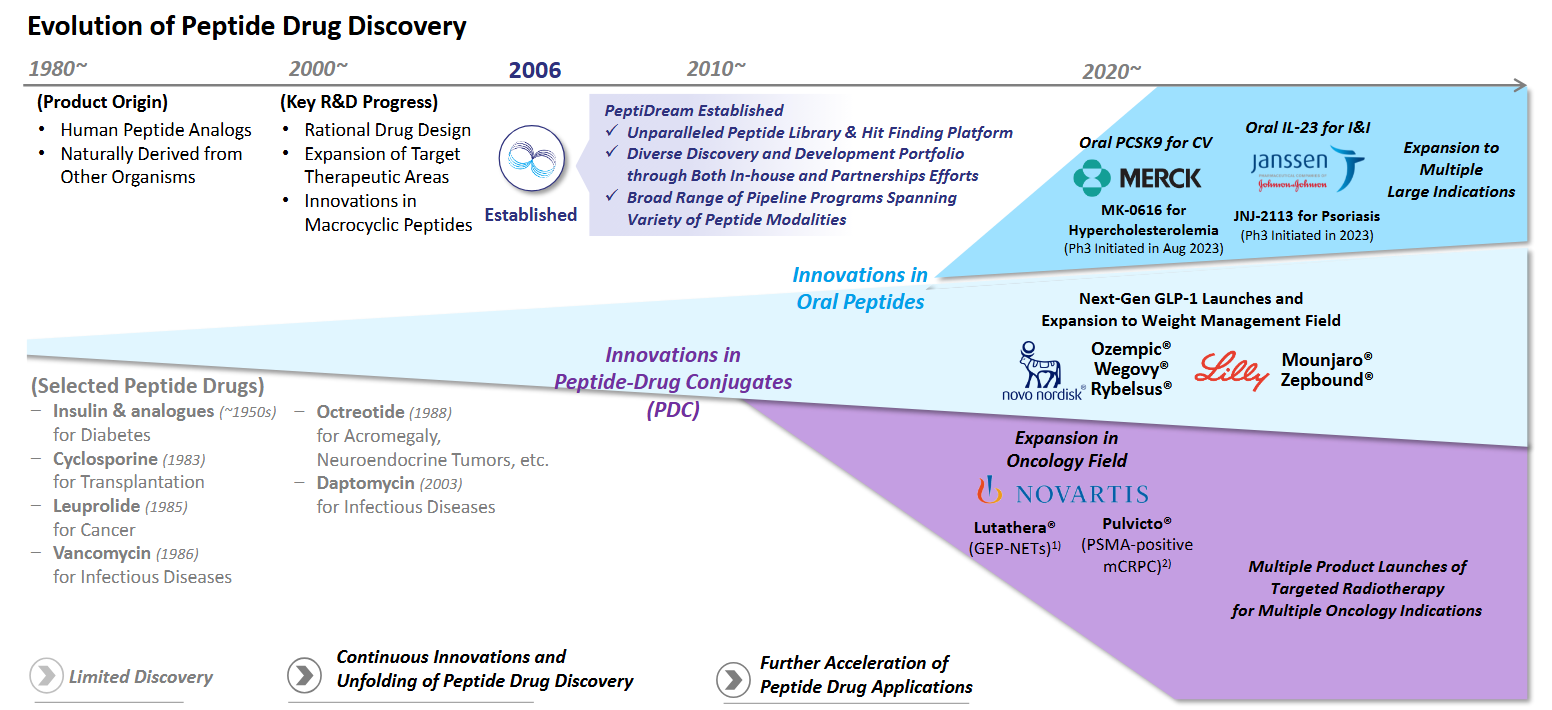

In addition here is an overview of the history of peptide drugs:

3 | Company‑Specific Moats

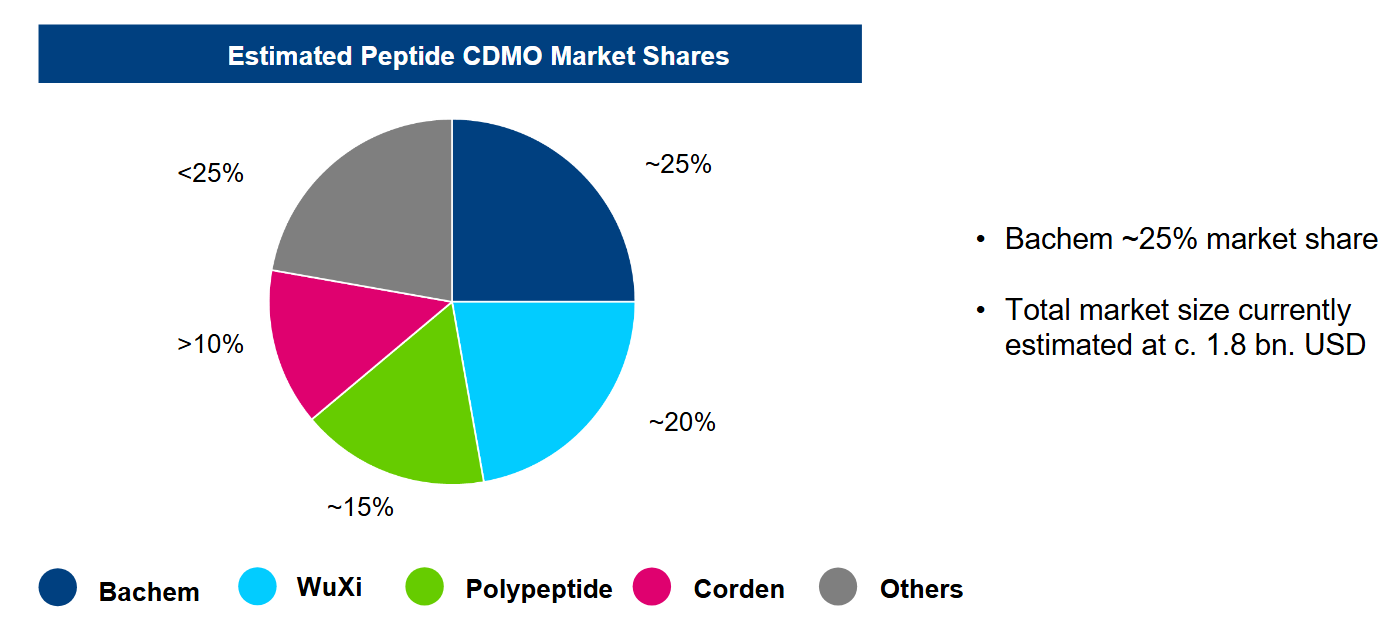

Bachem (BANB SW) — The Industrial Fortress

Scale and forward‑sold capacity.

New Swiss “Building K” and Vista, CA lines will raise annual peptide throughput to ~1 t by late 2025, an order of magnitude above most peers.

Two disclosed “take‑or‑pay” contracts, CHF 1bn (2025‑29) and CHF 0.5bn (2027‑31), secure baseline utilization and pricing visibility for almost a decade.

Regulatory trust & switching costs.

Fifty‑year GMP record means Bachem has sailed through every major regulatory audit; a failed batch at a vendor of this scale is virtually unheard of.

Tech‑transferring a peptide process can take 18 - 24 months and a fresh CMC filing, so customers stick rather than risk supply‑chain gaps.

Process innovation moat.

Continuous chromatography and greener solvent loops cut cost per kilogram and reduce environmental footprint, advantages that widen with volume.

Because capex is front‑loaded, each incremental kilo drops > 70 % gross contribution margin once the plant passes break‑even, reinforcing operating leverage.

PeptiDream (4587 JP) — The IP Flywheel

Unique library chemistry.

PDPS uses engineered ribosomes to insert non‑canonical amino acids, generating trillions of macrocycles inaccessible to ordinary phage or mRNA display.

The platform’s diversity translates into higher hit‑rates on challenging targets (e.g., protein-protein interfaces), compressing Pharma R&D timelines.

Deal economics validate moat.

Novartis paid $180m upfront with up to $2.7bn milestones for radioligand discovery rights, signalling that no internal platform could match PDPS.

Genentech, Lilly, Merck and over twenty other partners have struck similar deals; PeptiDream often retains co‑development or royalty options, converting R&D into annuity income.

Data and know‑how compounding.

Each program enriches PDPS with ADME, toxicology, and structure‑activity data, making the next discovery cycle faster and more predictive.

Competitors would need to replicate not only the chemistry patents but also a decade of accumulated experimental metadata, an intangible moat money alone can’t buy quickly.

PolyPeptide (PPGN SW) — Agile #2 With Global Reach

Geographic redundancy plus breadth.

Six GMP plants across EU, US and India give clients tariff and supply‑chain hedging that single‑site rivals can’t match.

Service breadth spans custom NCEs, cosmetic peptides, and generics, spreading fixed costs and keeping asset utilization high even between big launches.

Contractual catch‑up.

A €100 m‑per‑year GLP‑1 supply deal, ramping from 2024, doubles baseline revenue and funds Belgian “mega‑line” expansion aimed at 25% EBITDA margins by 2028.

Management has stabilized post‑IPO growing pains with lean‑manufacturing upgrades; every incremental percentage point of reactor utilization lifts earnings disproportionately.

Peptron (087010 KS) — Depot Specialist, Asymmetric Upside

Proprietary SmartDepot platform.

Microspheres achieve near‑zero burst release and linear pharmacokinetics, a combination competitors frequently miss, especially for hydrophilic peptides.

LoopOne (sustained‑release exenatide) already approved in Korea proves regulatory viability and gives real‑world manufacturing experience.

Strategic IP in neurodegeneration.

NIH CRADA grants exclusive rights to use SR‑exenatide for CNS disorders, a coveted indication because GLP‑1’s neuroprotective effects are well published but delivery hampered by BBB clearance.

If Phase 2 Parkinson’s data confirm animal models, Peptron can license SmartDepot broadly or retain co‑development economics, offering multi‑bagger potential from a small base.

4 | Where Demand Meets Moat

GLP‑1 tonnage lands at Bachem & PolyPeptide.

Even conservative obesity penetration requires hundreds of metric tons of tirzepatide and semaglutide APIs; no greenfield site can come online before 2027.

With forward‑sold reactors, both CDMOs gain pricing power and volume certainty unmatched in most of specialty pharma manufacturing.

Next‑gen radioligands funnel through PeptiDream.

Radiopharma success is peptide‑vector limited: better affinity extends isotope half‑lives and reduces off‑target dose, crucial for regulatory approval.

PDPS macrocycles excel at tuning affinity and pharmacokinetics, anchoring multi‑billion milestone stacks that produce non‑dilutive cash and perpetual royalties.

Depot reformulations create royalties for Peptron.

Every chronic peptide therapy eventually chases monthly dosing to protect franchise pricing as generics loom; depot know‑how thus becomes lifecycle‑management gold.

Because the polymer science is process‑protected, Peptron licenses its formulation at double‑digit gross‑royalty rates, a margin expansion story if even one blockbuster converts.

Pipeline breadth backstops risk.

Over 150 peptide NCEs are in Phase II or later, covering oncology, endocrine, GI, and infectious diseases, creating a conveyor belt of manufacturing and discovery work.

That breadth diversifies revenue streams for CDMOs and multiplies option value for discovery platforms, cushioning the basket against single‑asset attrition.

5 | Model Portfolio Allocation

1.10% Bachem (BANB SW):

Acts as the cash‑flow anchor; biggest moat, signed contracts, and high‑20s EBITDA margin even during capex surge.

Risk lies primarily in project execution, schedule slips would delay revenue but contract volumetrics remain intact.

0.60% PeptiDream (4587 JT):

Provides high‑beta royalty upside while de‑risked by blue‑chip partner roster and non‑dilutive funding structure.

Milestone timing is lumpy; diversification across >25 programs mutes individual failure impact.

0.20% PolyPeptide (PPGN SW):

Adds manufacturing diversification and potential valuation catch‑up as margin upgrades materialize.

Execution and scaling in Belgium are watch‑points; however, long client relationships reduce competitive churn risk.

0.10% Peptron (087010 KS):

Small position contains binary trial risk yet preserves asymmetric upside if CNS read‑outs hit or SmartDepot sees broader licensing.

6 | Conclusion

Peptide drugs have crossed the chasm: Blockbuster GLP‑1 sales prove mass‑market appetite; next‑wave radioligands and depot versions extend runway into oncology and CNS.

Moats matter more than valuations: Capacity and IP are the real scarcity; price/earnings multiples compress quickly if companies own the choke‑points that pharma cannot replicate in house.

This 2% sleeve is deliberately concentrated: Majority weight sits in fortress assets (Bachem, PeptiDream) for steady compounding; minority weights grant exposure to operational turnarounds (PolyPeptide) and moon‑shot delivery tech (Peptron).

Own the few players that control either the reactors or the intellectual property enabling tomorrow’s peptide blockbusters, because when demand outruns supply and discovery bottlenecks tighten, rents accrue to those with the widest, hardest‑to‑bridge moats.

Disclaimer:

Ridire Research is an independent research publication operated by Ridire Research LLC and affiliated with a private fund, an Exempt Reporting Adviser under the U.S. Investment Advisers Act of 1940. Ridire Research is not registered as an investment adviser and does not provide personalized investment, legal, accounting, or tax advice.Informational & Educational Purpose Only

All materials—including text, charts, model portfolios, and explicit labels such as “Buy,” “Sell,” “Hold,” “Long,” or “Short”—are published solely for general informational and educational purposes. They reflect the author’s views at the time of writing, derived from publicly available data, proprietary frameworks, and market analysis, and are not tailored to any reader’s specific objectives, financial situation, or risk tolerance. Subscription to this Substack does not create an adviser–client relationship with the affiliated private fund or its principals.

No Offer or Solicitation

Nothing herein constitutes (i) an offer to sell or the solicitation of an offer to buy any security or other instrument, (ii) a recommendation to participate in any investment strategy, or (iii) a solicitation for investment advisory services. Any references to trades, allocations, or vehicles should be viewed as hypothetical model illustrations only. Offers, if ever made, will be made solely by confidential offering documents and only to qualified investors in jurisdictions where permitted.

Potential Conflicts of Interest

The affiliated private fund, its affiliates, employees, and related accounts may hold, increase, decrease, initiate, or exit positions, long or short, in securities or digital assets discussed, without notice or obligation to update disclosures. Such positions may be inconsistent with views expressed in this publication. The affiliated private fund, related entities, and personnel may initiate, modify, or exit positions in any mentioned security before or after publication without further notice. We maintain internal policies, including trading blackout windows and conflict reviews, to mitigate potential conflicts of interest.

Accuracy & Forward-Looking Statements

Although we strive for accuracy and analytical rigor, information may become outdated and may contain errors or omissions. Forward-looking statements, projections, or target prices are inherently uncertain and may differ materially from actual results. No warranty, express or implied, is given as to completeness, accuracy, or reliability.

Risk Acknowledgment

Investing involves substantial risk, including the potential for complete loss of capital. Past performance, whether actual, indicated by back-tests, or modeled, is not indicative of future results. Securities, derivatives, and digital assets mentioned may be illiquid, highly volatile, or subject to regulatory change.

Reader Responsibility

Readers should conduct their own due diligence, consider their personal circumstances, and consult a licensed financial professional before acting on any information contained herein. By reading this publication you agree that Ridire Research LLC, the affiliated private fund, and their affiliates accept no liability for any direct or consequential loss arising from reliance on the information presented. This research is not directed at persons in jurisdictions where such distribution would be contrary to local law.

Peptides will be Major. Saw someone get something from Co springs & he got Yoked while staying trim. Boulder Peptide company?

Much appreciated with the article came timely. Bachem up 20% today.