Rare by Design

Where Margin, Moats, and Mispricing Collide

In an environment where biotech volatility is driven more by macro flows and sentiment than fundamentals, we propose a deliberately constructed long/short: long a focused basket of rare-disease leaders (RAREDIS Index), short the SPDR S&P Biotech ETF (XBI). This trade captures structural outperformance rooted in cash flows, pricing power, and execution, and hedges it against speculative beta, dilution, and index churn.

XBI, the SPDR S&P Biotech ETF, is a cap-weighted collection of ~300 biotech names spanning preclinical platforms to commercial-stage companies. It reflects broad sector sentiment more than business fundamentals. Clinical trial blowups, funding conditions, and policy shifts regularly move the ETF, which contains a large proportion of unprofitable or pre-revenue companies. Historical drawdowns of 15–20% are common in macro risk-off environments.

Crucially, XBI’s equal-weight design forces capital into many companies with overlapping therapeutic targets, commodity-like pipelines, and binary risk. Oncology and immunology dominate exposure. As a result, XBI underweights durable, high-margin orphan businesses in favor of speculative platform stories. The result is a diluted signal where even standout names are muted by peer churn.

By contrast, our RAREDIS basket concentrates on 12 companies with strong revenue visibility, orphan exclusivity, proven commercialization, and capital discipline. These names operate in defined niches, rare endocrine, CNS, immunologic, and diagnostic markets, where pricing power and regulatory protection allow for superior economics. Many of them are raising guidance, expanding product franchises, and returning capital. That fundamental traction is being systematically overlooked by investors still chasing biotech beta.

The RAREDIS vs. XBI trade is a simple but asymmetric expression: own the few that compound, short the many that dilute. The opportunity lies in the divergence between repeatable, protected rare-disease cash flows and the low-conviction noise of the biotech index.

BioMarin Pharmaceutical (BMRN)

BioMarin is a pioneer in genetic rare diseases. Its model is to develop high‑barrier orphan drugs for single-gene disorders (PKU, mucopolysaccharidosis, achondroplasia, hemophilia) and monetize them at premium pricing. Its current portfolio includes VOXZOGO for achondroplasia, PALYNZIQ for PKU, and enzyme therapies for lysosomal storage disorders. Rare-disease coverage is broad: e.g. somatic enzyme deficiency disorders and skeletal growth defects.

Pricing Power & Margins: Orphan exclusivity and clinical benefit let BioMarin price in the >$100K–$500K range per patient drug. This yields gross margins ~80% (typical for biologics) and healthy profitability as scale improves. For example, Q4/2024 saw 4Q GAAP net margin ~17% on $747M sales. BioMarin has been slimming SG&A/R&D on terminated projects, further lifting profit (Q4 net income up by $105M YOY from program cuts). Recurring royalty from each launch underpins steady FCF.

Execution: Q4 2024 revenue grew ~16–18% to $747M. Growth was led by VOXZOGO; new achondroplasia starts surged ~40% YoY (global launch expanding) and by broad uptick in its enzyme therapies (Aldurazyme, Brineura, etc). CEO commentary highlighted double-digit overall growth and margin expansion, driven by new patient starts worldwide. BioMarin reaffirmed 2025 guidance, signaling confidence. Importantly, the company is refocusing on core assets (like ROCTAVIAN hemophilia gene therapy) and cutting tail costs, which drove a jump in Q4 net income through lower R&D.

Catalysts & Upside: Upcoming catalysts include new indications and trial readouts: e.g. mid-2025 PALYNZIQ adolescent PKU data could expand labels; VOXZOGO is enrolling hard-to-reach groups (hypochondroplasia, idiopathic short stature), potentially creating multi-year growth. A Duchenne muscular dystrophy oligonucleotide (BMN 351) is first data readout H2’25. Critically, the Inozyme (Everlution) acquisition adds a Phase 2 ENPP1 asset (for calciphylaxis) and ops to BioMarin’s pipeline. If the company wins its Korlym-like patent lawsuit (on Kuvan, BioMarin’s old PKU drug), exclusivity extends further. The market may underappreciate the cumulative runway: patent portfolios of orphan drugs often last a decade, and BioMarin’s $1.8B cash pile funds M&A and gene therapy rollout (e.g. the delayed Roctavian in hemophilia). In short, BioMarin stands out as a cash-generative rare-disease leader building a multi-year franchise of high-barrier therapies.

Halozyme Therapeutics (HALO)

Halozyme is a drug-delivery platform company (hyaluronidase) with an orphan tilt via its high-margin Enhanze® royalty streams. Halozyme’s product “Hylenex” and its Enhanze technology (rHuPH20 enzyme) enables subcutaneous delivery of partnered biologics. It collects royalties (~15%) on blockbuster drugs converted to injection form (e.g. Roche’s Herceptin®, Genentech’s etc) and sells its own Hylenex consumable. Halozyme has minimal standalone R&D risk, its value comes from enabling partners’ therapies, many of which address specialty and immunology/oncology needs.

The Enhanze platform provides recurring, royalty-based revenue with very high gross margins. In Q1 2025 Halozyme grew revenue 35% YoY to $264.9M, driven by escalating royalty income (e.g. Herceptin SC, Teva’s Darzalex SC, Rituxan SC, etc.). Net income surged to $118.1M (on $264.9M sales). The business is asset-light: once the enzyme is approved, virtually every partnership deal boosts margin. SG&A remains low relative to income, yielding exceptionally high EBITDA margins (~50%+). Management has also put $250M into a share buyback, signifying abundant free cash. The result is a structurally profitable growth engine, largely insulated from small-pipeline binary risk.

Execution: Halozyme’s Q1 beat showed “accelerating growth in CABOMETYX demand” for partners (an analogy: as Exelixis sold more, or similar), reflecting strong uptake of partner products. Recently, Halozyme raised 2025 guidance (per PR commentary) in light of robust royalty trends. The pipeline (Halozyme’s own R&D) is modest, mostly focused on new enzyme formulations and high-volume formulations, but not essential to the thesis. The key differentiator is Halozyme’s platform moat: very few competitors offer hyaluronidase tech at scale. This gives Halozyme pricing power in deals, and recurring royalties so long as partners grow their drug sales.

Catalysts: Upside comes from new partnership launches (the next Herceptin-type deals) and geographic expansions. For instance, Halozyme recently signed deals in emerging markets, broadening Enhanze’s base. Any new major biologic adopting subcutaneous delivery (e.g. large new insulin or antibody franchises) boosts royalties. A positive hospital-billing environment (OASIS payment rule, etc.) may also lift utilization of their tech. Halozyme is often lumped with unprofitable pre-revenue biotech, but it’s more akin to an “asset-lite” royalty co. Its cash flows are far more predictable, and with limited R&D overhead, it’s unlike a typical biotech. This hidden stability versus XBI’s volatility is a relative advantage.

Corcept Therapeutics (CORT)

Corcept is focused on endocrine and metabolic disorders, primarily Cushing’s syndrome (cortisol excess). Its flagship is Korlym (mifepristone), approved for hyperglycemia in Cushing’s. Cushing’s is rare (a few thousand U.S. patients), so Korlym has effectively global exclusivity and high pricing (~$17,000/mo). Corcept also re-entered the oncology space with cortisol-modulating cancer drugs, but rare disease is the core cash engine.

Korlym remains the sole therapy in its niche, giving Corcept a captive pricing model. The drug requires a specialty endocrine pharmacist distribution, maintaining high margins on a capital-light asset. In Q1 2025, revenue was $157.2M (+7% YoY), reaffirming management’s $900–950M 2025 target. Critically, Korlym scripts nearly doubled YoY in Q1 due to a big push on screening hypercortisolism (Cushing’s). This “patient funnel” expansion indicates market under-penetration.

Executio: Corcept continues consistent profit (fourth profitable year). Q1 net income grew ~144% to $20.5M. The company managed a temporary pharmacy supply hiccup early in the year, but demand proved strong: by March record pill shipments resumed. Separate from Korlym, Corcept’s pipeline includes relacorilant (a next-gen GR antagonist) with applications in Cushing’s (adult and pediatric) and in oncology (e.g. platinum-resistant ovarian cancer). The pivotal ROSELLA Phase 3 recently reported a 30% reduction in ovarian cancer progression risk with relacorilant, underscoring cortisol modulation’s therapeutic role. This success positions Relacorilant for an NDA potentially in Q4 2025 (Cushing’s) and an additional regulatory path in ovarian cancer, expanding the addressable market far beyond purely rare endocrine disease.

Risks & Catalysts: The main risk is patent challenges: Corcept is fighting Teva’s generic Korlym (they won at district court, appeal pending). If Corcept prevails, generics would be blocked through 2037. A loss could bite revenues, but the company has prepared defenses. Catalysts include NDA outcomes: a Relacorilant approval in Cushing’s (H2’26) would effectively double their endocrine franchise, addressing all adult Cushing’s rather than only diabetic complications. An oncology indication (ovarian) would also be high-margin. Market misunderstanding might underweight Corcept as a one-drug company, but in reality it has two late-stage assets (Relacorilant’s multi-indication trials) and an expanding core business thanks to underdiagnosed Cushing’s.

SOBI (Swedish Orphan Biovitrum) – (SOBI:SS)

SOBI is a specialty pharma veteran devoted to orphan and niche diseases, mainly in hematology, nephrology, and rare immunology. Its strategic portfolio includes hemoglobin disorders and rare blood diseases: drugs like Vonjo (JAK2 inhibitor for myelofibrosis), Aspaveli/Empaveli (PNH), Doptelet (platelet booster), Gamifant (HLH), and Altuviact (formerly Elocta), a long-acting Factor VIII for hemophilia A. SOBI also holds royalties on Sanofi’s Upstaza (Cerezyme oral enzyme for Gaucher). The company systematically acquires or partners for orphan drugs, then drives sales through Europe and emerging markets.

Pricing & Structure: SOBI’s orphan niche affords strong pricing. For instance, factor VIII therapies and PNH drugs command >$300k annual prices. Q4 2024 was a good run: excluding seasonality, Q4 sales ex-RSV portfolio grew ~23%. Hematology was +13% overall, with Hemophilia A (Elocta/Altuvoct) sales +29% at constant FX. Margins are high , the CFO noted ~77% gross margin on Q4 adjusted sales, delivering ~36% adjusted EBITDA. This reflects that many orphan drugs have minimal generic risk and steady demand once launched.

Execution: Altuvoct (long-acting FVIII) launches have been strongly positive for SOBI, as shown by rapid uptake in Europe and conversion of patients. Other launches (Vonjo for myelofibrosis, Upstaza for Gaucher) contribute to durable tails. On Q1 2025 calls, management reports stable demand for key products (Altuvoct, Doptelet) and disciplined expense growth. SOBI has also maintained ~1x net debt on EBITDA leverage, allowing reinvestment. A recent secondary sale by a large shareholder has depressed the stock, but the underlying business continues solid execution.

Catalysts & Mispricings: Catalysts include continued geographic expansion: e.g. new Altuvoct launches and additional label expansions (e.g. prophylaxis in younger HemA). Ongoing R&D (like intramuscular Factor VIII) could unlock new regimens. Also, SOBI is active in M&A, the Advent/GIC takeover bid for SOBI (~$8B in 2021) underscores its value. Key is that the orphan market is growing: diseases like PNH and HLH see more awareness. The market may still under-estimate SOBI’s long-term cash flows, focusing on modest current EPS. But with a 40%+ revenue CAGR in its strategic portfolio recently, SOBI stands out as a well-run, high-leverage rare-disease play.

Exelixis (EXEL)

Exelixis is an oncology-focused developer whose main product Cabometyx® (cabozantinib) spans kidney cancer, liver cancer and thyroid cancer, and newly approved neuroendocrine tumors. Its rare-disease angle is limited (Cometriq® for medullary thyroid carcinoma, a rare tumor), so Exelixis isn’t a pure rare specialist. However, it offers exposure to novel oncologic targets via high-barrier drugs.

Cabometyx is a leading multikinase inhibitor with growing indications. The drug enjoys strong patent protection and is partnered outside the U.S. (Ipsen), with multiple label expansions boosting sales. In Q1 2025, Cabometyx U.S. revenue +X% YOY (noted as “accelerating growth in CABOMETYX demand”). Exelixis’ profitability is excellent: in Q1 net revenues were $555M and they raised FY guidance by $100M. The company has been profitable for years on high-margin sales, plus it now sports a growing pipeline of internally developed TKIs (e.g. zandelisib) and partnered immunotherapies.

The big news was the strong commercial execution on Cabometyx and new indications. CEO Michael Morrissey highlighted “outstanding financial performance… increasing our guidance”. Profit margins remain very high (non-GAAP EPS $0.62 vs $0.55 GAAP in Q1) as R&D is modest relative to sales. The launch in neuroendocrine tumors (a relatively smaller market but growing) was executed rapidly, suggesting the team is adept at expanding use cases.

Catalysts & Risks: Near-term catalysts include next-gen internally developed molecules. For example, the oral TKI zanzalintinib (in collaboration with Merck) has Phase 3 readouts pending (colorectal, non-clear RCC). Positive STELLAR trial outcomes could turn Exelixis into a multi-franchise oncology player. The company also has early work in other cancers (HNSCC trial, etc.). On the flip side, Cabometyx will eventually face competition from new drug combos, and Exelixis has some patent expiry mid-decade. However, with cash reserves and a clean balance sheet, Exelixis can weather setbacks and fund R&D. The company’s differentiation is execution in solid tumors with a proven kinase platform, in short, more “growth oncology” than “rare disease,” but it bolsters portfolio diversification and cash flow power relative to broad biotech risk.

Catalyst Pharmaceuticals (CPRX)

Catalyst is a small specialty pharma that develops and markets treatments for very rare neuromuscular diseases. Its key product is Firdapse® (amifampridine) for Lambert-Eaton Myasthenic Syndrome (LEMS), a condition affecting a few thousand patients. It also launched Agamree® (vodencokinra, a marketed name) in Duchenne Muscular Dystrophy (DMD), another rare disease, in 2024 via acquisition. Thus, Catalyst’s entire portfolio targets high-need orphan niches.

Firdapse is essentially a retail tablet for LEMS, priced at roughly $100,000–$200,000 per patient annually (reflecting its orphan “privilege”). Similarly, Agamree (for certain DMD subtypes) commands a high price per dose. Hence Catalyst enjoys gross margins north of 70%. Q1 2025 results were a surge: total revenue $141.4M (+43.6% YoY). Breaking out, Firdapse was $83.7M (+25% YoY) and Agamree $22.0M (from near zero prior year). Catalyst has no legacy pipeline burn, nearly all spending goes into commercial scaling of these two drugs, enabling EBITDA margins to explode (>60% in Q1).

Catalyst’s Q1 showed “record” growth as expected from Agamree’s roll-out. Management highlighted that Firdapse still has headroom (more neurologists to sign up), while Agamree is a brand-new blockbuster in DMD (they expect a $1B+ market, per commentary). The company reiterated 2025 guidance, indicating confidence in sustaining momentum. Because both drugs have easy distributors (oral pills), execution risk is low. The stock’s valuation reflects that Catalyst is essentially a specialty drug seller: predictable cash flows rather than typical biotech gamble.

Catalysts & Misunderstandings: The next catalysts are pipeline expansions. Catalyst is exploring additional indications (e.g. clinical trials of Firdapse in conditions beyond LEMS) and has signaled interest in more acquisitions (expanding in neurology). Notably, the company sees Agamree’s label as just a start, newer DMD trials (60% recessive) are on the horizon to broaden use. On the flip side, one risk is generic competition for Firdapse; however, Catalyst has fortified its IP (five patents) and has a lawyered-up stance (as with BioMarin/Teva). Investors may overlook how capital-light Catalyst is (today it’s ~2x debt/EBITDA). We believe it merits inclusion for its rare-disease focus and for the pure profit-generating engine it provides. In brief: Catalyst turns high orphan prices into very durable profits, unlike typical cash-burn biotechs.

ADMA Biologics (ADMA)

ADMA Biologics is a plasma-derived biologics manufacturer, focusing on primary immunodeficiency (PID) and other immunocompromised patient populations, indeed a “rare disease” category (PID affects a few per 100k). Its products (e.g. ASCENIV™, a high-titer IVIG for PID) are exotic immunoglobulin products that treat life-threatening rare disorders. ADMA operates U.S.-based plasma collection and fractionation, integrating supply.

ADMA’s IVIG products carry orphan-like status: ASCENIV has orphan designation for RSV/LRI, and they have a pipeline for (pandemic/pediatric RSV) prophylaxis. IVIG pricing is high (often $100K+/year per patient), and ADMA sells through specialty distributors. In Q1 2025, ADMA reported $114.8M in revenue (+40% YoY), driven largely by ASCENIV acceptance. Gross margins rose to ~53% (from 48% prior year) due to a mix of higher-margin products. Importantly, ADMA turned GAAP profitable (NI $26.9M vs $17.8M prior) as volume scaled.

ADMA’s USP is a capped, recurring-immunology franchise with a U.S.-only supply chain (immune products are largely domestic). Management has locked in long-term high-titer plasma contracts and invested in a new manufacturing yield-enhancement (recently FDA-approved) to boost capacity 20%. They are raising guidance, e.g. targeting >$500M revenue in 2025 and $1.1B by 2030, assuming continued PID expansion. The $98.8M Q1 free cash flow and conservative net debt (zero after $500M equity in 2021) give them financial flexibility.

Catalysts: Key catalysts are execution of the new production process (adding supply capacity without needing new plants) and capturing more of the PID market. ADMA recently authorized a massive $500M stock buyback (8% of market cap), a sign the Board views the business as undervalued given its growth outlook. Also, if healthcare policy favors domestic manufacturing, ADMA stands to benefit. Misunderstood aspects include how insulated ADMA is: global IVIG suppliers are often abroad, but ADMA being US-only avoids tariffs and supply chain shocks (management noted this as a strategic advantage). In short, ADMA is not a speculative biotech but a manufacturing play fueling orphan immunoglobulin growth with high barriers and building a fortress balance sheet.

Neurocrine Biosciences (NBIX)

Neurocrine is a midcap pharma focused on central nervous system disorders, notably movement and neuroendocrine conditions. Its main product is INGREZZA (valbenazine) for tardive dyskinesia (TD), a movement disorder (non-rare). However, Neurocrine also markets Orilissa for endometriosis and has more than $1B potential in narcolepsy with Wakix (see Harmony). The reason it appears in RAREDIS may be “specialty CNS,” though it’s not a classic rare disease.

Ingrezza is Neurocrine’s blockbuster, with 2024 rev ~$2.0B. In Q1 2025 it grew 8% YOY to $545M on record new patient starts (expanding screening/treatment of TD). The firm has a strong balance sheet ($1.8B cash, minimal debt) and has used cash to buy back stock ($300M done, $500M new program) as well as fund pipeline. R&D spend is only ~10–15% of sales, so margins are very healthy. The company boasts ~12 consecutive quarters of double-digit revenue growth in Ingrezza.

Neurocrine continues steady growth even as many broad biotech languish. The quarterly press noted “strong momentum” with Ingrezza hitting $545M (8% growth). It also launched a new sleep drug CRENESSITY (a nasal spray for cataplexy in narcolepsy), first quarter sales $14.5M (adding new revenue stream). The expanded insurance coverage (Medicare) for Ingrezza (now 2/3 of TD/HD patients) is a key win that should sustain growth. Neurocrine generated ~$71.5M non-GAAP profit in Q1, albeit down from prior year due to accelerated R&D. Critically, they still turned a GAAP profit ($7.9M Q1).

Catalysts: Neurocrine’s near-term catalysts are all pipelines. Notably, they are testing Ingrezza in new indications (studies for pediatric TS, pediatric TD are done; Parkinson’s trial ongoing). A Phase 3 in Huntington’s disease (tardive-like movements) is planned. They also have novel programs: creatine analog (BP1.15205) for depression (phase 2 soon) and opioid antagonist for binge-eating (in partnership with Ambys). Importantly, none of this is pure “rare,” but it diversifies risk. On the rare side, Neurocrine is moving into pediatric neurology, though such usage might get Orphan creds, it’s modest. In effect, Neurocrine’s inclusion hinges on its disciplined execution: two major products that grow steadily, unlike many XBI names that burn cash. The market often undervalues Neurocrine’s durability; recent profits dipped due to buybacks and one-time write-downs, but those are short-term. Its competitive edge is a defensive CNS pipeline and a strong launch track record.

Hologic (HOLX)

Hologic is a diversified women’s health and diagnostics company (not focused on rare disease per se). Its main businesses are breast imaging (mammography machines), diagnostic tests (STIs, cervical cancer, bone density, COVID-19), and surgical devices (gynecologic). We include it as a “big biotech-lite”, stable revenues, mission-critical products, and healthy cash flows.

Hologic’s products (mammogram scanners, cervical cancer tests) enjoy durable demand and often benefit from reimbursement and guidelines (e.g. women’s screening is mandated). They face some commoditization in imaging, but the shift to digital/molecular tests gives pricing power. Fiscal Q1 2025 saw revenue $1,022M (essentially flat YOY at +0.9%), driven by diagnostic growth (+5.2% in Dx) offsetting slight declines in imaging. They generate very strong operating cash ($189M in Q1) and are aggressively buying back stock ($517M Q1, completing a $250M ASR). Non-GAAP EPS of $1.03 was at the top of guidance, reflecting cost discipline.

Hologic’s non-cyclicality (healthcare capex is sticky, diagnostics grew ~9% ex-COVID) and margins (~37% operating) make it a relatively low-risk “beta” contributor. It also has a rising dividend yield (~1–2%) and recently added shareholder returns via buybacks. Importantly, its diagnostics end-market leverages secular trends (e.g. molecular STD testing, advanced breast health). The cash machine lets it invest in R&D (e.g. new cancer screening tests) without diluting shareholders.

Catalysts: Key near-term drivers are expansion of diagnostics and acquisitions. Hologic acquired Endomagnetics (a lymphatic mapping tech) and saw more procedure volume. They also expect their bone health and cardiovascular screening lines to pick up. On the downside, breast imaging capital sales can be lumpy (weaker Q1 was due to a tough comp). A misunderstanding in the market is treating Hologic as a tech company – it is in fact more like a consumer staple (safe growth, solid cash flows). In the RAREDIS context, Hologic’s stock serves to stabilize a portfolio of riskier small biotech names.

Lantheus Holdings (LNTH)

Lantheus is a leading radiopharmaceuticals and molecular imaging company. It makes contrast agents and tracers that help “find and fight” disease, e.g. PYLARIFY® (PSMA PET for prostate cancer) and DEFINITY® (ultrasound contrast). Its pipeline includes Alzheimer’s amyloid and tau PET tracers, and emerging therapeutics in neuroendocrine tumors. It straddles diagnostics and theranostics (the treatment of disease guided by imaging).

Lantheus is tangentially in rare disease via acquisitions. Most notably, they bought Evergreen Therapeutics (radioactive nanobody for osteosarcoma, an orphan pediatric tumor) and plan to buy Life Molecular Imaging (GLP-1 brain imaging tracer). Osteosarcoma is extremely rare (1,000 cases/year US). These moves are building a “hard-to-treat-cancers” pipeline on top of Lantheus’s core imaging franchise.

PYLARIFY is now the world’s top-selling PET radiotracer (> $1B annual run-rate). In Q1 2025, PYLARIFY sales were $257.7M (down just 0.5% YOY), reflecting steady use. DEFINITY grew 3.5% to $79.2M. Total revenue was $372.8M (+0.8% YOY). Margins are strong, operating income was $102M, with Adj. EBITDA margins near 39%. Lantheus generated $98.8M FCF in Q1. The balance sheet is fortified with $938M cash (and zero debt after acquisitions).

Execution: Management has pivoted to inorganic growth: Q2 2025 closed the Evergreen deal (oseonidangium, orphan designation) and expects Life Molecular soon. The focus is now also on commercialization of MK-6240 tau PET (Phase 3 readout expected 2025). CEO Markison emphasizes leveraging Lantheus’s commercial engine for these niche assets. On core business, Lantheus continues “100% PSMA coverage”, e.g. PYLARIFY is in virtually all U.S. PSMA scan centers.

Catalysts: Approvals and launches of new tracers (MK-6240 in Alzheimer’s tau; upcoming amyloid PET in Japan) are near-term catalysts. The orphan radio-immunotherapies (like the 212Pb-labeled NET therapy from Perspective partnership) could be 2026 catalysts. Lantheus is one of the few healthcare plays with secular tailwinds (aging population, more imaging diagnostics) and also one foot in niche oncology. The market often undervalues what are really high-margin specialty pharmaceuticals: its current multiples (~10x cash flow) may not reflect the long-term monoclonal launch potential and recurring consumable sales.

Camurus (CAMX:SS)

Camurus is a Swedish biotech that commercializes niche drugs using its proprietary “FluidCrystal” delivery platform. Notably, it sells Buvidal® (CAM2038), a long-acting injectable buprenorphine for opioid dependence (and chronic pain), and CAM2039 for pain, both selling in Europe and Australia. Crucially, Camurus also holds rights to Mepsevii® (idursulfase gene therapy for Hunter syndrome) outside the U.S., tapping a classic rare-disease orphan market.

Buvidal revolutionized opioid treatment with monthly subcutaneous dosing; its success is reflected in Camurus’s explosive growth. In Q1 2025, total revenue was SEK 558M (~$55M), up 43% YoY. Product sales (mainly Buvidal) were SEK 485M (+33% YoY). Importantly, royalties from Braeburn’s US launch of Buvidal (Brixadi®) hit SEK 74M (+185% YOY), showing the globalizing reach. These are high-margin sales. The result: profit before tax jumped 162% YoY, to SEK 254M (~45% margin).

Camurus’s rare upside comes from Oczyesa® (CAM2029), a monthly octreotide depot for acromegaly (an orphan endocrine disorder). A positive CHMP opinion was announced post-Q1. If approved, Oczyesa will be the first monthly peptide treatment for acromegaly, a market of ~4,000 patients in the EU alone. They also have a GLP-1 (CAM2056) depot in early phase (obesity/diabetes), though not orphan. The Mepsevii arrangement is a legacy, but less material now; future rare-gene therapy deals (already one for Duchenne antisense) could add to optionality.

Catalysts: Besides Oczyesa’s EU approval, catalysts include continued geographic expansion of Buvidal and new indications. The company is initiating Phase 3 for CAM2043 (postpartum depression neuroactive steroid) and has Phase 1 underway for CAM2056 (GLP-1 depot). Market misunderstanding might understate Camurus: many focus on Buvidal sales, but the pipeline (long-acting neurology/endocrine drugs) is substantial. In summary, Camurus combines a blockbuster opioid franchise (with high barriers) and a foothold in rare endocrine with Oczyesa, meriting its role in a rare-disease strategy.

Harmony Biosciences (HRMY)

Harmony Biosciences specializes in sleep disorders, which are rare or specialty neurology niches. Its approved drug is Wakix® (pitolisant), a novel histamine H3 antagonist for narcolepsy and idiopathic hypersomnia (IHS). Both are rare, chronic CNS disorders (narcolepsy ~20 per 100k, IHS comparably rare). Harmony has no other marketed products, so it is essentially a one-drug company (like Neurocrine).

Wakix is priced at ~$20,000–$30,000 per patient per year, reflecting its orphan-class niche and lack of alternatives (it’s the only FDA-approved narcolepsy pill, aside from stimulants). In Q1 2025, Wakix sales hit $184.7M (+20% YoY), reiterating guidance of ~$820–860M for 2025 (implying >2x revenue in 3 years). Harmony has been consistently profitable (4th year in a row).

Execution: Harmony’s commercial team is driving deeper penetration. By Q1 they had “record new patient starts” for Wakix, aided by expanded formulary access (Medicare now covers two-thirds of narcolepsy and Huntington’s beneficiaries). The company is preparing for a heavy R&D schedule: completing Phase 3 for ZYN002 (a cannabidiol gel in development for Fragile X syndrome) with data due Q3 2025, and initiating next-gen pitolisant trials in pediatric narcolepsy and IHS later in 2025. These are each rare indications: Fragile X is a rare genetic autism spectrum, and the pediatric sleep disorders are very low-incidence. Harmony is also developing an orexin agonist (BP1.15205) for sleep-wake disorders.

Catalysts: The big near-term catalyst is the ZYN002 Fragile X trial readout , positive data would open a vast new rare-disease market. Also, expansion of Wakix into idiopathic hypersomnia (approved in Feb ’24) is still ramping. Harmony’s stock may underappreciate how rapidly Wakix can grow (the CEO projects >$1B narcolepsy market alone). On the risk side, investors worry about generic competition post-patent (2036 at earliest) and the lone-product nature, but Wakix’s novel mechanism and orphan status give it a secure moat for many years. Harmony deserves inclusion for the same reason as Neurocrine: it is a highly profitable, growth-oriented rare-disease specialist. Unlike XBI names, its revenues are well-forecastable and EPS has been reliably positive, backed by a huge cash cushion (major Chinese investor).

Summary:

The RAREDIS basket is intentionally skewed to companies with orphan/ultra-specialty footprints, high pricing power, and recurring revenue streams. Each name, from BioMarin’s genetically-targeted enzyme therapies to Corcept’s endocrine drugs, from SOBI’s hematology franchises to Catalyst’s ultra-niche neurological treatments, shares the common thread of defending or expanding a protected patient base. In every case, recent results underscore operational traction. Forward catalysts (label expansions, trial readouts, acquisitions, reimbursement gains) are well-defined and within 6–18 months. This contrasts with XBI’s “shotgun” exposure to broad biotech, which currently trades on speculative valuations. In sum, our high-conviction rare disease basket is built on defensive cash generation and near-term visibility, a portfolio we believe should outperform the broader biotech index through 2025 and beyond.

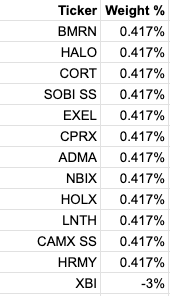

Model Portfolio Weights:

Disclaimer:

Ridire Research is an independent research publication operated by Ridire Research LLC and affiliated with a private fund, an Exempt Reporting Adviser under the U.S. Investment Advisers Act of 1940. Ridire Research is not registered as an investment adviser and does not provide personalized investment, legal, accounting, or tax advice.Informational & Educational Purpose Only

All materials—including text, charts, model portfolios, and explicit labels such as “Buy,” “Sell,” “Hold,” “Long,” or “Short”—are published solely for general informational and educational purposes. They reflect the author’s views at the time of writing, derived from publicly available data, proprietary frameworks, and market analysis, and are not tailored to any reader’s specific objectives, financial situation, or risk tolerance. Subscription to this Substack does not create an adviser–client relationship with the affiliated private fund or its principals.

No Offer or Solicitation

Nothing herein constitutes (i) an offer to sell or the solicitation of an offer to buy any security or other instrument, (ii) a recommendation to participate in any investment strategy, or (iii) a solicitation for investment advisory services. Any references to trades, allocations, or vehicles should be viewed as hypothetical model illustrations only. Offers, if ever made, will be made solely by confidential offering documents and only to qualified investors in jurisdictions where permitted.

Potential Conflicts of Interest

The affiliated private fund, its affiliates, employees, and related accounts may hold, increase, decrease, initiate, or exit positions, long or short, in securities or digital assets discussed, without notice or obligation to update disclosures. Such positions may be inconsistent with views expressed in this publication. The affiliated private fund, related entities, and personnel may initiate, modify, or exit positions in any mentioned security before or after publication without further notice. We maintain internal policies, including trading blackout windows and conflict reviews, to mitigate potential conflicts of interest.

Accuracy & Forward-Looking Statements

Although we strive for accuracy and analytical rigor, information may become outdated and may contain errors or omissions. Forward-looking statements, projections, or target prices are inherently uncertain and may differ materially from actual results. No warranty, express or implied, is given as to completeness, accuracy, or reliability.

Risk Acknowledgment

Investing involves substantial risk, including the potential for complete loss of capital. Past performance, whether actual, indicated by back-tests, or modeled, is not indicative of future results. Securities, derivatives, and digital assets mentioned may be illiquid, highly volatile, or subject to regulatory change.

Reader Responsibility

Readers should conduct their own due diligence, consider their personal circumstances, and consult a licensed financial professional before acting on any information contained herein. By reading this publication you agree that Ridire Research LLC, the affiliated private fund, and their affiliates accept no liability for any direct or consequential loss arising from reliance on the information presented. This research is not directed at persons in jurisdictions where such distribution would be contrary to local law.