Rare by Design 2

Where Margin, Moats, and Mispricing Collide

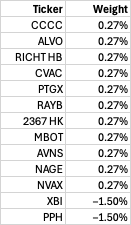

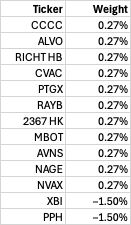

Setup: 3% long sleeve of 11 rare-disease and specialty healthcare names (~0.27% each) vs. -3% short split XBI/PPH (≈50/50) for a near market-neutral expression.

Core thesis: In biotech/medtech, power accrues to bottlenecks: IP chokepoints, regulatory exclusivity, clinician workflow captivity, manufacturing scarcity, and distribution privileges. Own the bottlenecks, short the beta.

Model Portfolio Weightings:

How We Define “Moat” In This Context

Regulatory protection: Orphan exclusivity, Breakthrough/PRV advantages, complex labeling that deters follow-on.

IP choke points: Foundational patents (platforms, adjuvants, process IP) + freedom-to-operate barriers.

Manufacturing scarcity: Biologics/biosimilars scale, high-purity proteins, aseptic complexity, or GMP-qualified capacity.

Clinical workflow lock-in: Installed software/device bases, multi-year hospital contracts, training & data gravity.

Channel & KOL control: Specialist prescriber concentration, advocacy groups, long-tail disease education.

Capital discipline: Non-promotional OPEX, partner leverage, milestone funding, balanced risk budgets.

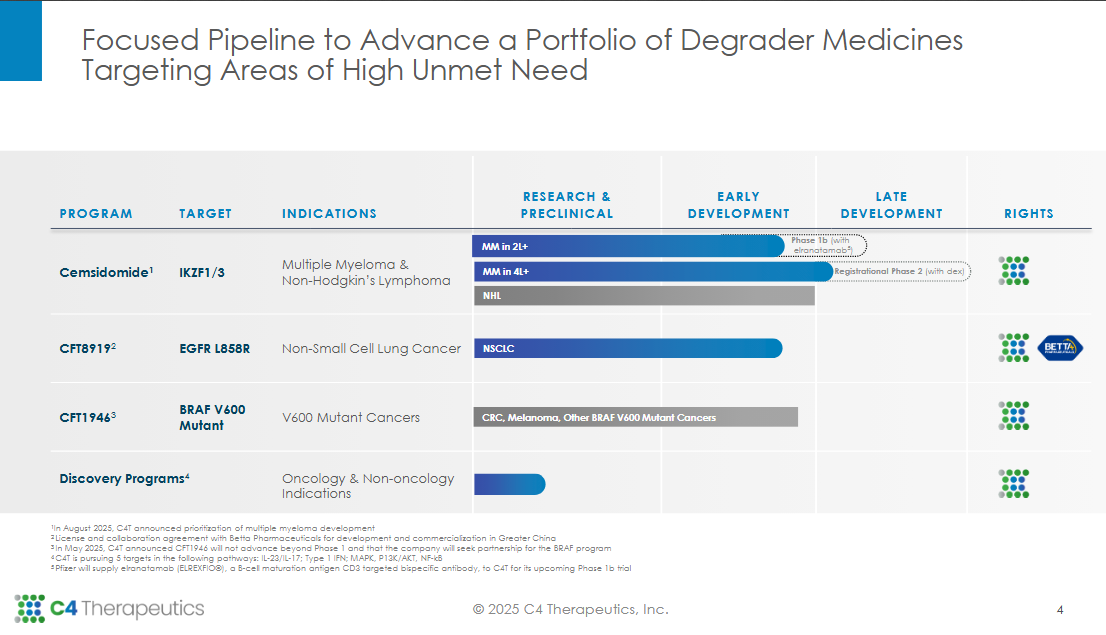

1) C4 Therapeutics (CCCC): Targeted Protein Degraders (TPD)

C4 Therapeutics sits at the intersection of precision oncology and chemical innovation. The company is one of the purest plays on targeted protein degradation (TPD), a modality designed to “tag” disease-causing proteins for destruction rather than inhibition. Where traditional small molecules block activity, degraders remove the protein entirely, offering potency and durability beyond conventional approaches.

C4’s differentiator is its E3 ligase platform chemistry, the cellular machinery that enables targeted degradation, paired with an evolving IP fortress and early proof-of-concept in orphan oncology indications. In a landscape crowded with discovery-stage imitators, C4 has turned platform potential into a replicable drug engine.

Moats

Platform IP & know-how:

C4’s intellectual property around E3 ligase binding and linker design represents a deep, defendable moat. The company’s proprietary TORPEDO platform (Target ORiented ProtEin Degrader Optimizer) provides rational degrader design and in silico screening capabilities, giving it a first-principles edge that shortens the optimization loop from years to months. These capabilities have already attracted blue-chip validation, including collaborations with Pfizer and Biogen, who recognized C4’s medicinal chemistry depth and scalable screening. The chemistry is not plug-and-play; ligase recruitment and linker optimization are empirically hard problems few labs can solve repeatedly.Orphan oncology focus:

Unlike most TPD companies chasing broad oncology markets, C4 has concentrated on rare, genetically defined cancers, such as synovial sarcoma and multiple myeloma, where smaller, faster pivotal trials can lead to exclusivity-driven cash flow. Orphan drug designations for CFT8634 (BRD9 degrader) in synovial sarcoma and CFT7455 (IKZF1/3 degrader) in multiple myeloma not only confer 7 years of U.S. market exclusivity but also ensure regulatory support and pricing inelasticity. This rare-disease lens amplifies the fundamental advantages of the TPD platform, small, stratified patient populations, limited competition, and early commercial validation.Capital discipline:

Unlike many peers that overbuild, C4 has kept its burn rate lean, targeting one to two INDs per year and leveraging partners for risk-sharing. Its deal structures with Pfizer and Biogen provide milestone capital and downstream royalties, a hybrid biotech model that extends runway and keeps ownership optionality.

Bottlenecks

Ligase biology & medicinal chemistry:

Protein degradation is deceptively complex. Potency, selectivity, and pharmacokinetics must balance within narrow ranges, and only a handful of ligases (e.g., CRBN, VHL) have proven tractable. C4’s team has mastered ligase-ligand engineering across multiple E3 ligases, an expertise that forms both a technological and personnel bottleneck. Very few companies possess comparable structure-based modeling and in vivo optimization data at this scale, making C4 one of the only independent pure-plays capable of serial degrader production.Trial access in ultra-rare tumors:

With orphan oncology programs, KOL relationships and site readiness are strategic assets. Running efficient studies in rare tumor subtypes requires established referral networks, trial design expertise, and patient registries, resources C4 has already built through its sarcoma and myeloma collaborations. These networks serve as barriers to entry for newer entrants hoping to replicate the orphan model.Manufacturing and scale-up:

While degraders are small molecules, they often possess complex linker chemistries that strain standard GMP processes. C4’s internal CMC knowledge and supply chain partnerships position it ahead of many TPD competitors that are still scaling pilot batches.

Trip-Wires / KPIs to Monitor

Durable responses in orphan oncology cohorts, especially synovial sarcoma (CFT8634) and multiple myeloma (CFT7455): readouts confirming disease modification over inhibition.

Combination data with standard-of-care (e.g., lenalidomide) validating safety and synergistic efficacy, unlocking broader usage.

Partnership milestone cadence: revenue recognition from Pfizer/Biogen deals will serve as confidence indicators of external validation.

Variant Risk

Class-wide toxicity: TPDs have flirted with IMiD-like or cereblon off-target effects, particularly in immune cells; adverse safety signals could reset investor confidence in the entire modality.

Ligase resistance: Tumors may evolve ligase-binding site mutations or alternative degradation pathways, eroding durability.

Platform crowding: Larger players (Arvinas, Kymera) could absorb capital attention, though their broader indications dilute focus.

Summary View

C4 Therapeutics exemplifies what Rare by Design looks like in early-stage innovation: a company that engineered both a molecular and strategic moat.

Technological moat: Replicable degrader chemistry + platform IP.

Market moat: Orphan oncology focus with exclusivity and limited competition.

Operational moat: Partner funding and data-driven design that compound efficiency.

As the sector evolves, degraders will likely bifurcate, platform owners and product licensees. C4 is built to be the former. Its pipeline depth, orphan execution, and capital prudence make it a long-duration optionality trade within a space most investors treat as binary.

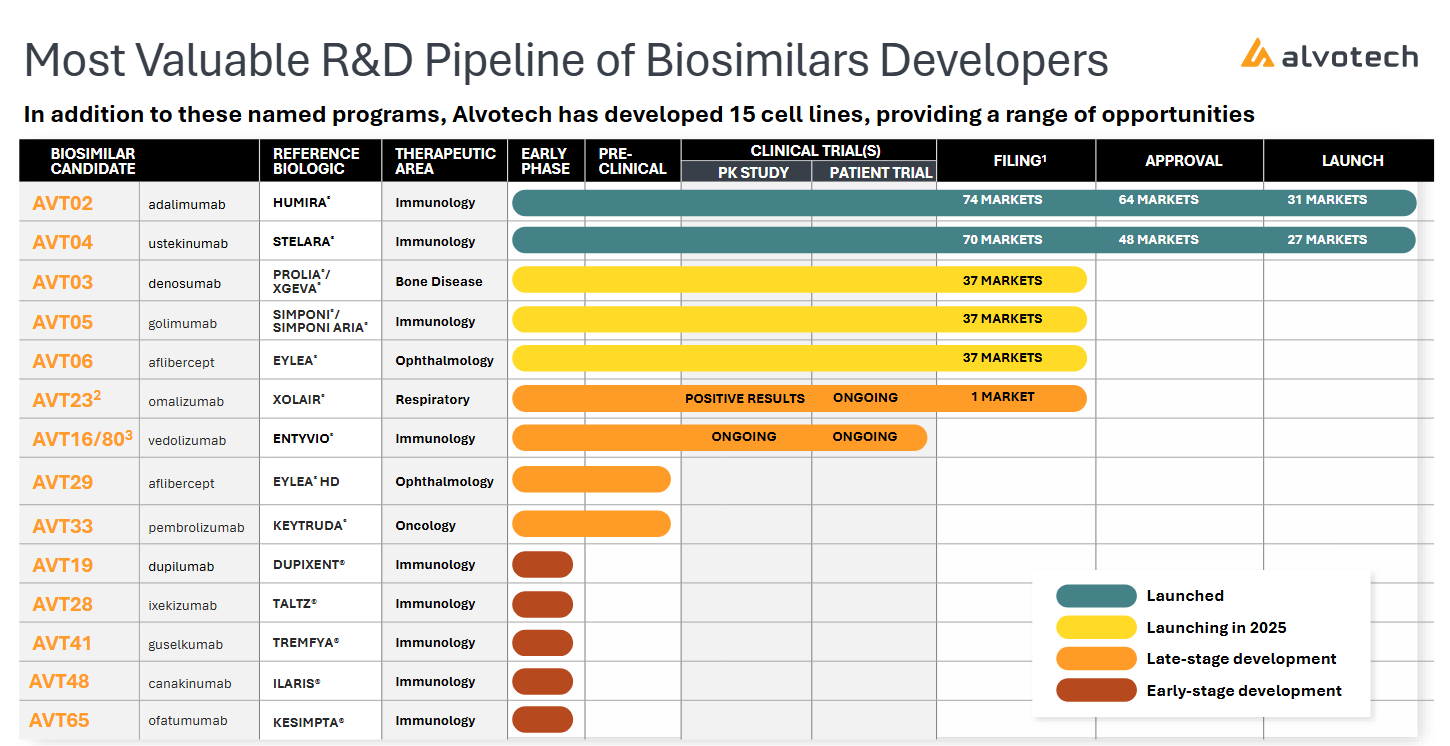

2) Alvotech (ALVO): Biosimilar Foundry with Rare-Disease Reach

Alvotech is quietly building what could become the TSMC of biologics, a fully integrated, globally compliant biosimilar manufacturer with the infrastructure, analytics, and regulatory credibility to operate as a capacity bottleneck in a post-patent world. Where most biotechs are single-asset narratives, Alvotech is a platform in reverse: it starts with proven biologics and competes on cost, quality, and speed at a global scale. Its moat isn’t just about price competition, it’s manufacturing orthodoxy, regulatory intimacy, and network distribution across dozens of payor regimes.

Moats

End-to-end biologics capability:

Alvotech is one of the few independents that controls the entire biosimilar value chain, from cell-line development to purification, analytics, and fill-finish, all within its single-site facility in Reykjavik, Iceland. This vertical control eliminates cross-contamination risk, reduces tech-transfer friction, and allows real-time process optimization. The result: faster global filings, lower COGS, and tighter compliance cycles. For complex molecules (monoclonal antibodies, fusion proteins), reproducibility is the gatekeeper, and Alvotech has proven it can consistently meet EMA and FDA biosimilarity standards, a technical feat most peers still struggle with.Regulatory moat:

Alvotech’s CMC (chemistry, manufacturing, and controls) and analytics infrastructure rivals Big Pharma’s. It has already resolved FDA observations from 2022–23, re-establishing full GMP standing, a testament to quality governance discipline. This matters because biosimilar regulators are risk-averse; once a manufacturer demonstrates reliability, future approvals accelerate.Regulators trust repeat performers, and that trust compounds like credit history.Partner network as distribution flywheel:

Alvotech doesn’t commercialize everything alone. Instead, it licenses commercialization rights regionally, e.g., Teva in the U.S., STADA in Europe, Fuji Pharma in Japan, Advanz in smaller markets. This model decentralizes commercial risk while preserving global penetration. In effect, Alvotech’s partners act as a multi-node sales force, embedding the company across payer systems and formularies. This creates a distribution moat, Alvotech’s partners are incentivized to keep pipelines full, ensuring repeat deals and sticky relationships.Rare- and specialty-bio overlap:

Beyond the blockbuster biosimilars (Humira, Eylea), Alvotech’s pipeline includes biosimilar candidates for orphan and specialty indications. Through its Advanz Pharma collaboration, it’s developing copies of drugs like canakinumab (IL-1 inhibitor for rare autoinflammatory syndromes) and ofatumumab (B-cell therapy for multiple sclerosis). These target markets combine high biologic pricing and low patient counts, allowing biosimilars to enter rare-disease economics without the risk of true novelty R&D. In short: Alvotech leverages its scale into rare biology adjacencies, where pricing power and reimbursement stability mirror orphan-drug dynamics.

Bottlenecks

CMC comparability analytics:

The hardest moat to replicate is statistical similarity.Achieving equivalence across pharmacokinetics, potency, and glycosylation profiles requires proprietary assay systems and seasoned analysts. Alvotech’s analytical team has built internal libraries of reference product variability, allowing it to predict drift and adjust production proactively, a subtle but powerful edge in passing biosimilarity reviews.Sterile fill-finish and purification throughput:

Global sterile fill-finish capacity remains the ultimate bottleneck in biologics.

Alvotech’s integrated, high-yield line can process multiple biosimilars simultaneously, enabling it to time product launches precisely with patent cliffs.

In practice, that means while competitors scramble for contract manufacturing slots, Alvotech hits the market on Day 1 of patent expiry, a margin timing advantage that compounds with every cycle.Global regulatory harmonization:

Alvotech’s team has become fluent in multiple regulatory dialects, FDA, EMA, MHRA, PMDA, each with distinct analytical and validation standards. This multi-jurisdiction competence forms a human-capital bottleneck that can’t be easily poached. Few teams can synchronize filings across four continents while keeping CMC consistency, it’s a quiet, underappreciated moat.

Trip-Wires / KPIs to Monitor

U.S. approval cadence: FDA reinspection milestones (particularly for AVT02, the Humira biosimilar) and speed of post-approval market share gains.

Partner launch velocity: STADA and Advanz execution in Europe; visibility into pricing discipline under tender regimes.

Biosimilar pipeline progression: Transition of canakinumab/ofatumumab programs toward pivotal stages, key to proving rare-disease leverage.

Facility utilization: Degree of production line optimization and throughput increases post-FDA clearance.

Variant Risk

Tender compression: Simultaneous price erosion across top molecules can squeeze blended margins, especially if payors shift faster than volume uptake.

Regulatory reinspection: Any reemergence of compliance findings could reprice execution risk, given single-site dependence.

Partner misalignment: Underperformance or strategy shifts by commercial partners could temporarily mute uptake in key geographies.

Summary View

Alvotech is an industrialized biology story: one site, global compliance, reproducible output. Its manufacturing-first moat creates optionality across molecules and geographies, and its rare-disease biosimilar pivot introduces upside in niche, high-margin categories. In a biotech landscape obsessed with discovery, Alvotech’s edge is execution at scale: control of every molecule, every batch, and every gatekeeper.

This is the antithesis of speculative biotech, tangible cash conversion from process scarcity. Own the factory everyone else must rent.

3) Gedeon Richter (RICHT) — CNS Royalty + Women’s Health

Gedeon Richter is Europe’s best-kept secret in specialty pharmaceuticals, a 120-year-old Hungarian firm that quietly built two enduring profit engines:

(1) a royalty stream from Vraylar (cariprazine), one of the world’s best-selling antipsychotics, and

(2) a deep, defensible franchise in women’s health built on decades of proprietary steroid chemistry.

Where most biotechs chase one molecule or one modality, Richter compounds through royalties, niche innovation, and global distribution. Its moat is structural: protected cash flows, high-margin chemistry, and patient trust built molecule by molecule.

Moats

Blockbuster royalty annuity (CNS):

Vraylar (cariprazine) is co-developed by Richter and Allergan (now AbbVie). It’s approved for schizophrenia, bipolar I disorder, and as an adjunctive treatment for depression, a triple label that has driven explosive adoption. In 2023, U.S. sales exceeded $2.7 billion (+35% YoY), putting it among the top 50 drugs globally. Richter earns a mid-teens royalty on these sales, translating into hundreds of millions in steady, non-dilutive cash annually. The compound’s complexity, cariprazine is a dopamine D3/D2 partial agonist with slow receptor kinetics, makes generic replication difficult. Patents stretch into 2028–2030, with lifecycle extensions likely to protect the U.S. franchise into the early 2030s.

This royalty base functions like an internal bond portfolio, underwriting R&D and BD spend across the rest of the business.Steroid chemistry & women’s health mastery:

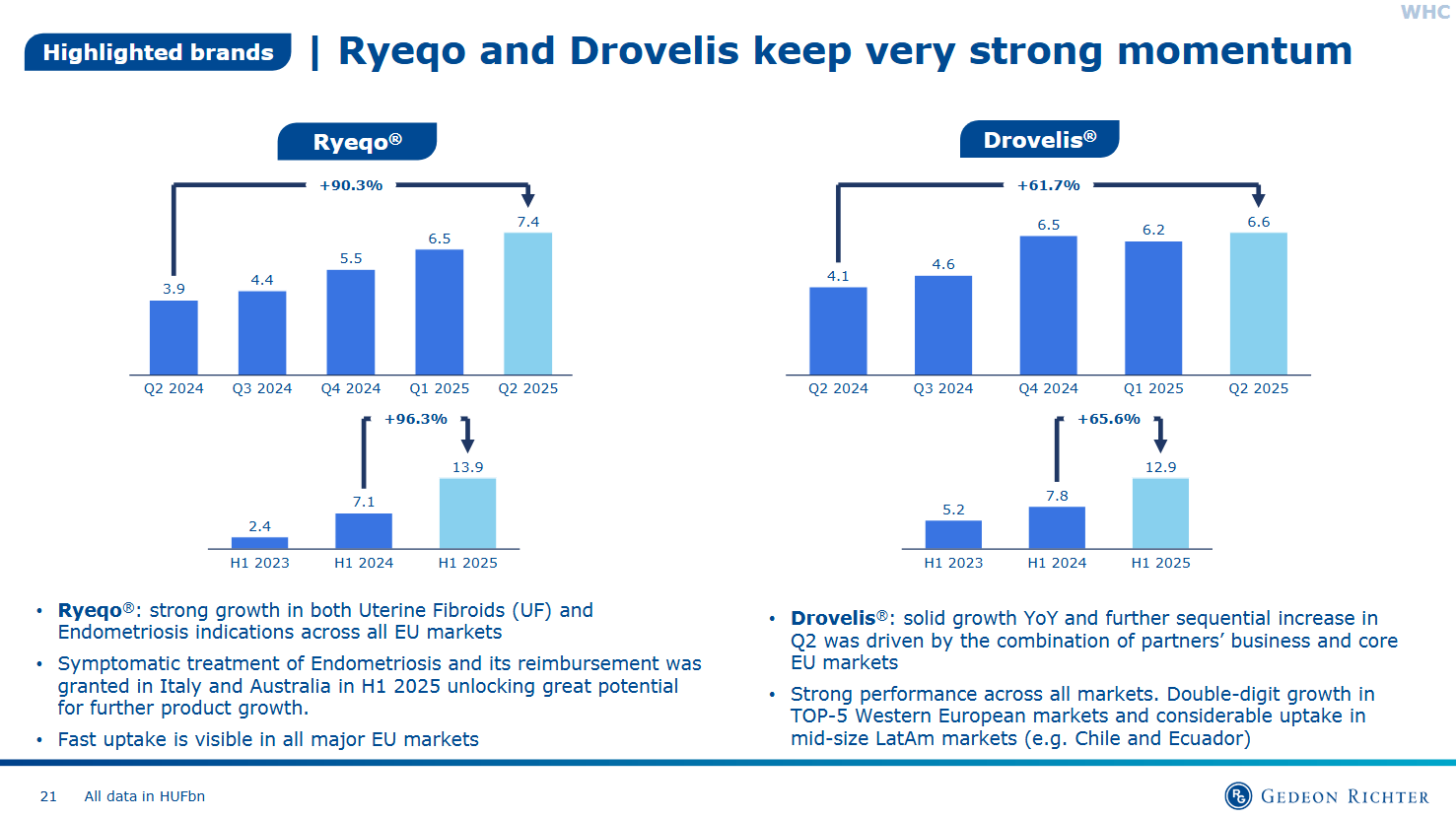

Richter’s second moat is biochemical, not financial. The company has been a global leader in steroid chemistry since the 1950s, one of the few independents capable of producing API-grade synthetic hormones and selective progesterone receptor modulators (SPRMs) at scale. This legacy underpins its market-leading contraceptive and menopause products, as well as new-generation oral therapies for gynecological disorders. Its flagship, Ryeqo (relugolix combination), provides a non-surgical therapy for uterine fibroids and endometriosis, conditions that affect millions but remain under-treated. These franchises enjoy decade-long product cycles, sticky prescriber bases, and strong payer acceptance, all key ingredients for compounding.Dual-channel moat: Royalty + Operating Profit Engine:

The Vraylar royalty stream smooths earnings volatility, while the women’s health division contributes recurring product revenue, a dual-channel model that gives Richter the financial elasticity to invest through downturns. Few mid-cap pharmas have such a balanced setup: one global royalty annuity (CNS) and one fully-owned cash cow (hormone-based therapies).Regulatory and geographic reach:

Operating in 100+ countries, Richter’s in-house EU regulatory and manufacturing infrastructure allows it to launch and distribute without dependency on contract partners. In Europe, it owns its salesforce; in emerging markets, it leverages long-standing joint ventures. This self-sufficiency in both supply chain and regulatory execution creates resilience most small biopharmas lack. EU-specific know-how, navigating national price caps, HTA submissions, and tender cycles, is a competitive advantage in its own right.Balance sheet moat:

Investment-grade rated, net-cash balance sheet, and prudent capital allocation. Richter is reinvesting royalty cash into de-risked adjacencies. The result is compounding without dilution.

Bottlenecks

Neuropsychiatric KOL and payer inertia:

Psychiatry has immense inertia. Once a molecule like Vraylar earns guideline inclusion and physician familiarity, switching costs become psychological as well as clinical. Prescribers and payers both resist disruption, especially in multi-indication therapies with established safety profiles. These entrenched relationships are hard to replicate and slow-moving, a behavioral bottleneck that sustains market share long after patent expiry anxiety begins.Regulatory positioning in women’s health:

The ability to run multi-country trials in reproductive endocrinology, from patient recruitment to regulatory harmonization, is a rare skillset. Richter has built end-to-end regulatory and clinical operations across the EU, Russia, and emerging markets. That infrastructure forms an invisible moat: it’s much faster and cheaper for Richter to bring a new therapy to market in Europe than for a U.S. mid-cap trying to localize operations.API vertical integration:

Richter manufactures its own active pharmaceutical ingredients (APIs), a strategic bottleneck in an industry now riddled with supply shocks. This ensures margin protection, quality control, and pricing leverage across both internal and partnered portfolios.Clinical development expertise in hormone modulation:

Decades of cycle control data and real-world safety outcomes form a proprietary database that newer entrants can’t shortcut. It’s a time moat, 40 years of validated pharmacodynamics data that underpins regulator trust and prescriber confidence.

Trip-Wires / KPIs to Monitor

Vraylar trajectory: Monitor AbbVie’s script growth and any early signs of generic strategy. Each new label expansion or add-on indication compounds the royalty stream’s duration.

Women’s health pipeline: Track adoption curves of Ryeqo and label expansions in uterine fibroids/endometriosis; early physician uptake and reimbursement wins are critical.

Royalty reinvestment rate: How much of the Vraylar cash is plowed into future compounding vs. returned as dividends.

Geographic expansion: Progress in Asia-Pacific and LATAM markets where hormone therapy penetration remains low.

Variant Risk

Patent expiry timing: Accelerated generic entry for Vraylar post-2030 could shorten the cash-flow runway, though complex chemistry reduces immediate threat.

EU pricing pressure: Drug price negotiations across key EU markets could trim margins in the women’s health portfolio.

Geopolitical exposure: Some emerging-market operations (Russia, CIS) introduce FX and regulatory volatility.

Pipeline execution: Delays or underperformance in newer gynecologic products could slow offsetting growth as legacy contraceptives mature.

Summary View

Gedeon Richter is a rare compounder hiding in plain sight, a blend of royalty annuity, chemical craftsmanship, and geographic self-sufficiency.

Its “barbell model”, one side stable (royalties), the other innovative (hormone therapeutics), generates durable returns and cushions volatility. This is a business that monetizes time: the inertia of physicians, the longevity of patents, and the compounding of trust. In the basket, Richter serves as exposure to two secular themes: mental health and women’s wellness. In a market full of pre-revenue promises, Richter is the exception: a cash-flow engine priced like a cyclical, performing like a compounder.

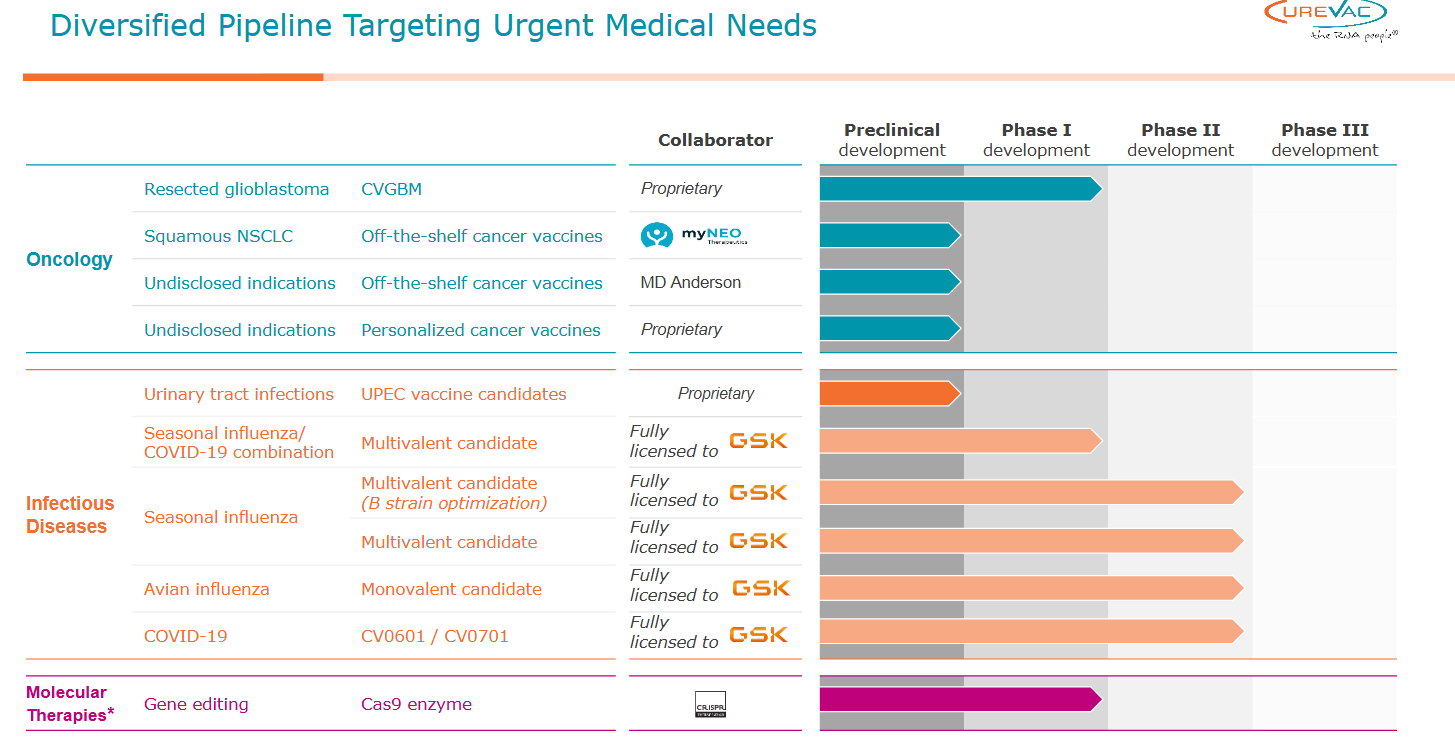

4) CureVac (CVAC) — The mRNA Toll Road

CureVac is the non-U.S. mRNA platform with a credible shot at toll-road economics: foundational sequence/process IP that others may need to license, a refocused Gen-2 pipeline (with GSK) aimed at higher translational efficiency, and a multi-year cash runway to execute in a capital-scarce tape. The setup is asymmetric: IP outcomes + leaner R&D + partnered execution give multiple paths to value creation without chasing volume at any cost.

Moats

Foundational IP & process know-how

Portfolio around sequence engineering (e.g., UTR/poly-A design), codon optimization, and templating that underpins antigen expression and durability.

The moat is a stack (sequence rules + manufacturing controls + QC analytics) that’s hard to replicate cleanly at scale.

Manufacturing orthodoxy (process control as a moat)

mRNA output hinges on tight in-vitro transcription, capping, purification, and LNP formulation windows. CureVac’s internal playbooks target lower batch variability and COGS step-downs, critical for seasonal vaccines and global tenders.

Process reproducibility plus release analytics become the regulatory trust asset (and barrier for fast followers).

Partnership leverage (GSK, EU ecosystem)

Co-development structure that shares wet-lab risk while preserving upside in infectious disease.

Proximity to European academic networks, trial infrastructure, and public health agencies shortens the path from lab → clinic → tenders.

Runway = optionality

A multi-year cash buffer (post-restructuring) in a tight funding regime; the company can sequence milestones rather than sell optionality at a discount.

Lets CVAC run Gen-2 shots on goal (infectious disease + early oncology) while litigating/negotiating IP from a position of time.

Bottlenecks

Sequence → expression translation

The hardest part of mRNA today is predictable in-cell expression across tissue contexts without excessive innate immune activation. CVAC’s rules-of-thumb for UTR/poly-A/codon usage are hard-earned and tacit, a human-capital moat not easily copied.

Scale, purity, and LNP fit

High-throughput enzymatic steps, dsRNA removal, and particle uniformity remain non-commoditized. Fit-for-purpose LNPs (organ tropism, reactogenicity balance) are a rate limiter for many rivals; CureVac’s platform alignment is a hidden gate.

IP navigation as a specialty

Global freedom-to-operate in mRNA is a maze. CVAC’s internal/extern counsel, claim strategy, and data room hygiene are a bottleneck capability, few teams can run offense (assert, settle) while keeping defense (FTO) intact across jurisdictions.

Trip-Wires / KPIs to Monitor

IP milestones: Interim rulings, settlements, or royalty frameworks that monetize platform rights without protracted appeals.

Gen-2 readouts: Early immunogenicity/neutralization vs first-gen baselines; translate into dose-sparing or durability advantages.

COGS trajectory: Evidence of batch yield gains and release-test cycle time reduction (seasonal viability, tender competitiveness).

Partner cadence: GSK co-dev milestones, new co-funded programs (respiratory, pandemic-preparedness), and regional tender wins.

Oncology wedge: First-in-human tumor vaccine signals (antigen presentation, T-cell quality), even in small cohorts, proof of platform versatility.

Variant Risk

Adverse IP outcomes: An unfavorable court sequence could defer or reduce toll-road monetization; optionality persists but timeline/value compresses.

Modality fatigue: Post-pandemic mRNA apathy could weigh on demand narratives; requires COGS + convenience wins (e.g., combo shots) to re-ignite.

Manufacturing shocks: Any CMC or LNP supply disruption would be disproportionately punitive given category perceptions.

Partner concentration: Execution risk if a major partner reprioritizes or slows funding cadence.

Competitive curves: Rivals’ self-amplifying RNA or next-gen delivery may reframe the efficiency frontier; CVAC must show delta, not parity.

Summary View

CureVac’s edge is platform law, not product lore: codified rules of sequence, process, and quality that can be monetized via toll-roads (IP), tenders (COGS), or translation (better Gen-2 data). With time on the balance sheet, credible partners, and a litigation/BD playbook, CVAC is positioned to harvest value from the plumbing of mRNA while keeping upside to category-expanding readouts. Own the mRNA toll-road: monetize the rules, scale the process, partner the products.

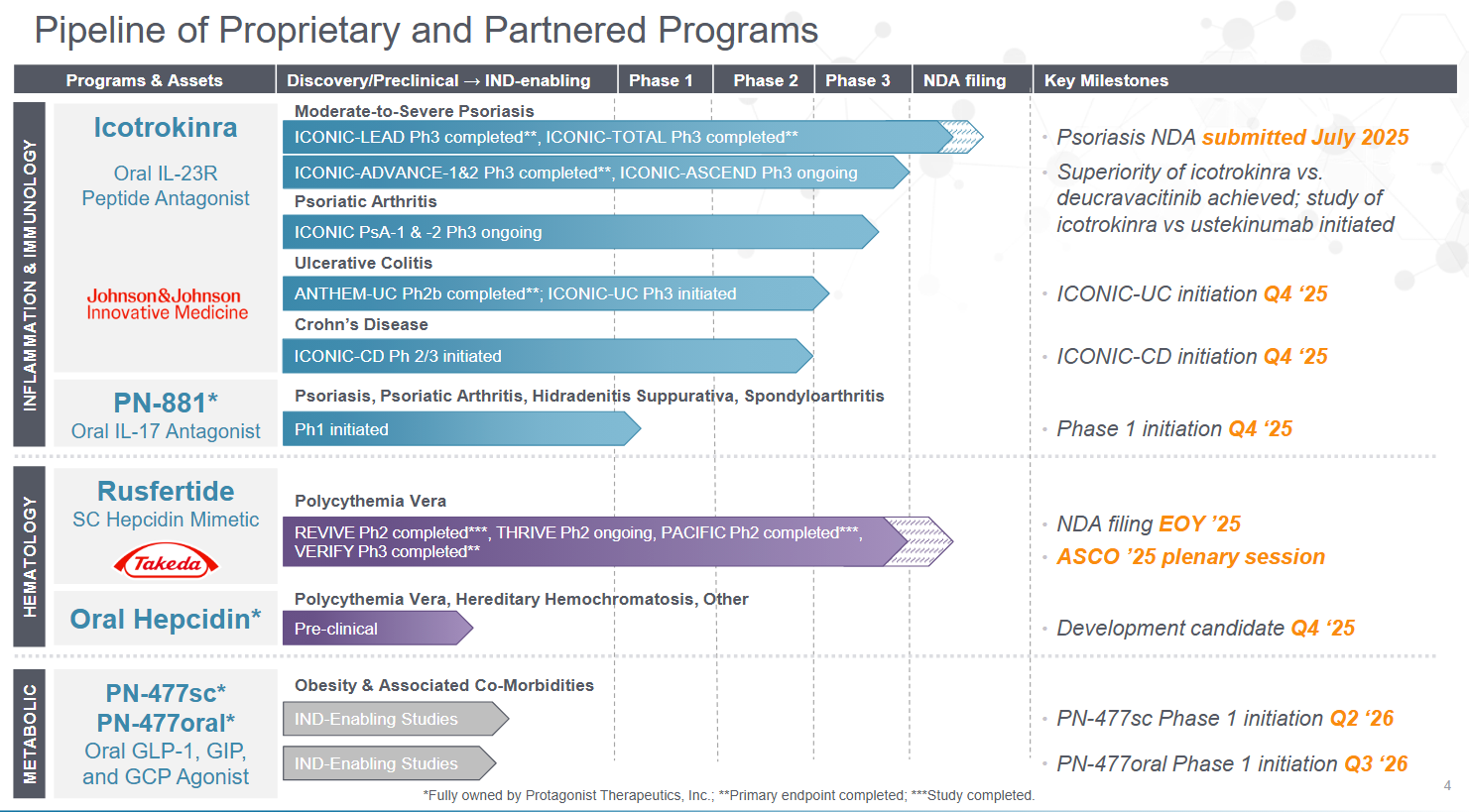

5) Protagonist Therapeutics (PTGX) — Peptides Become Products

Protagonist represents a rare bridge between biotech science and pharmaceutical discipline, a peptide engineering platform that has already delivered multiple clinical-stage assets and one nearing approval. Its lead program, rusfertide (PTG-300), has achieved Phase 3 success in polycythemia vera (PV) and secured both Breakthrough Therapy and Orphan Drug designations. With commercialization to be led by Takeda, the company is set to transition from R&D story to cash-flowing rare-disease player within two years. The broader moat lies not just in one molecule but in its proprietary peptide design engine, chemistry few competitors can match in scalability or stability.

Moats

First-in-class hepcidin mimetic:

Rusfertide is the first injectable peptide that mimics hepcidin, the master regulator of iron homeostasis.

In PV, a chronic myeloproliferative disorder with too many red blood cells, rusfertide normalizes iron balance and reduces or eliminates the need for phlebotomy, the current standard of care.

This mechanistic innovation is defensible; it’s not a reformulation or me-too drug, but a new biological class that reprograms the body’s feedback loop on erythropoiesis.

Orphan-drug economics:

PV affects roughly 100,000 patients globally, most inadequately controlled with outdated therapies.

With Orphan Drug and Breakthrough Therapy designations, rusfertide should secure 7 years of U.S. exclusivity (plus patent coverage into the mid-2030s) and premium pricing justified by chronic administration.

Its small, defined patient population makes it ideal for high-value specialty distribution, high-margin revenue with minimal sales infrastructure.

Partnered launch with Takeda:

Takeda’s rare-disease salesforce, payer access, and manufacturing infrastructure give rusfertide a global launch platform without balance-sheet dilution.

This partnership transforms PTGX’s profile from binary biotech to royalty-bearing cash compounder, letting management allocate capital toward pipeline expansion rather than commercialization risk.

Platform moat in peptide chemistry:

Beyond rusfertide, PTGX has engineered peptide scaffolds with drug-like half-lives, oral bioavailability, and tissue selectivity, solving one of biotech’s hardest problems.

This expertise, honed over a decade, enables the company to design peptides that combine biologic specificity with small-molecule pharmacokinetics, a “middle path” modality few can replicate.

The technology has already yielded validated assets, including an IL-23 receptor antagonist (JNJ-2113) that hit efficacy endpoints in psoriasis before Janssen returned rights (due to portfolio reprioritization, not data failure).

Bottlenecks

Peptide discovery & CMC expertise:

Rational design of constrained peptides , balancing structure, stability, and absorption, is an art form.

PTGX’s structure-guided design algorithms and proprietary linker chemistries are trade secrets, built through trial, error, and data.

Manufacturing complexity (solid-phase synthesis, purification yields) creates natural scarcity; few CDMOs can handle it efficiently.

Hematology KOL network:

PV is managed by a relatively small group of hematologists concentrated at academic and regional centers.

PTGX’s clinical team has spent years cultivating these networks through early-access programs and investigator-sponsored trials, relationships that act as a barrier to entry for any future hepcidin competitors.

Clinical access bottleneck:

Running trials in rare hematologic disorders demands both registry access and diagnostic precision.

PTGX’s long-term collaboration with Takeda ensures global trial continuity, patient recruitment velocity, and regulatory advocacy across regions, logistical advantages that take years to reproduce.

Trip-Wires / KPIs to Monitor

Regulatory milestones: NDA submission for rusfertide and acceptance by the FDA.

Commercial launch prep: Takeda’s market-access work (payer formulary inclusion, distribution setup, patient-assistance programs).

Label expansion: Exploratory trials in other erythrocytosis or iron-regulation disorders (e.g., β-thalassemia, hereditary hemochromatosis).

Cash cadence: Quarterly burn trajectory and milestone inflows; confirmation of >18 months cash post-NDA without equity raise.

Variant Risk

Safety & tolerability: Chronic injectable peptides can encounter injection-site reactions or long-term tolerability issues that require label mitigation.

Competition: Other iron-modulating drugs could emerge from larger hematology players; differentiation must remain clear on efficacy and compliance.

Regulatory timing risk: Any FDA data-request cycles could push out approval into 2027, deferring revenue inflection.

Partner concentration: Takeda controls launch pacing and marketing focus; any reprioritization could slow adoption.

Platform risk: Delays in pipeline partnering or setbacks in peptide oral delivery (e.g., PN-943) could limit diversification.

Summary View

Protagonist has out-engineered risk, de-risked clinical validation, orphan exclusivity, and a cash-rich partnership model that smooths the path from science to revenue.

The company now sits on the edge of its transition moment: from R&D cost center to rare-disease royalty machine, with pipeline optionality to follow. Its peptide platform is the kind of applied innovation moat Wall Street overlooks, chemically complex, capital-efficient, and scalable once the template is proven. Own the company turning peptides into a durable business model, first to market, first to cash flow, and first to repeat it.

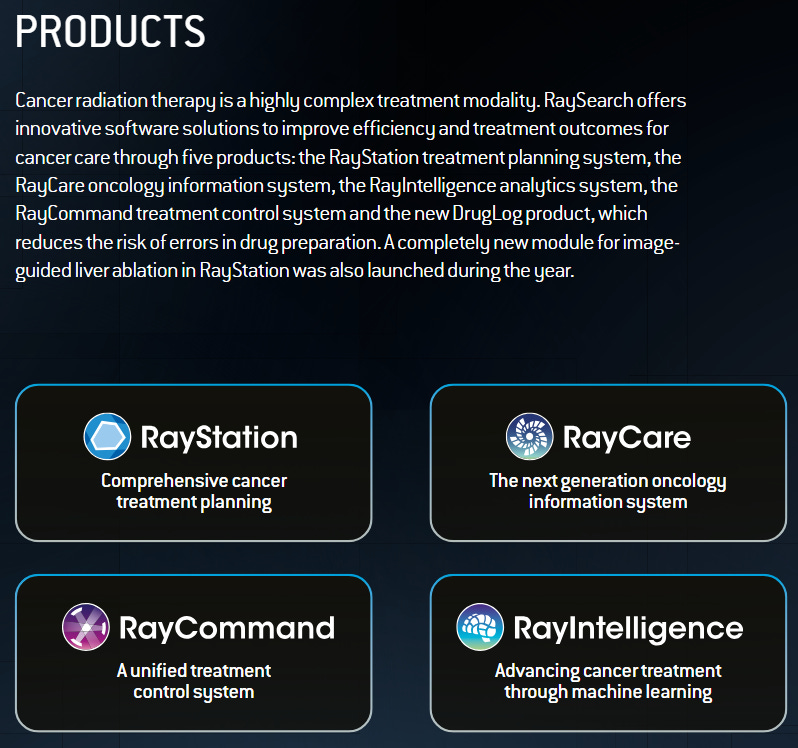

6) RaySearch Laboratories (RAYB) — Software as Infrastructure

While most of healthcare innovation happens at the molecular level, RaySearch Laboratories built a fortress in bits and bytes, dominating the invisible layer of cancer treatment planning software that radiation oncologists use every day. Its flagship platform, RayStation, sits at the center of radiotherapy workflows, embedded across more than 1,000 cancer centers in 46 countries. Once installed, it becomes part of the hospital’s nervous system, impossible to rip out without retraining entire departments and rewriting decades of protocols.

RaySearch sells control over precision, safety, and reimbursement compliance in one of the highest-value, lowest-error-tolerance corners of medicine. It’s a mission-critical monopoly hiding in plain sight.

Moats

Installed-base captivity (the real fortress wall):

RayStation and its companion system RayCare are deeply integrated into radiotherapy departments, linking linear accelerators (linacs), imaging systems, and hospital EHRs into a unified planning ecosystem.

Once deployed, the switching cost is massive: migrating away requires retraining clinicians, revalidating every treatment plan with regulators, and re-certifying billing workflows.

This results in decade-long customer relationships and near-100% renewal rates.

Proton therapy dominance:

RaySearch has an 85% market share in proton therapy centers, the fastest-growing, highest-value modality in global radiotherapy.

Out of the 46 proton centers in the U.S. and Canada, 43 use RayStation as their planning backbone.

Proton therapy’s precision and cost require software that minimizes margin-of-error at the submillimeter level. RaySearch has become the regulatory default, the planning system every new proton center must prove compatibility with to get licensed.

Cross-hardware interoperability:

RaySearch’s systems are vendor-agnostic, compatible with all major linac and imaging OEMs (Varian, Elekta, IBA, Mevion, Siemens).

This is crucial because many OEMs try to “bundle” their own proprietary software to lock in hardware sales. Hospitals, however, prefer flexibility, and RaySearch is the only truly multi-vendor-certified platform.

That means RaySearch sits in the middle of the radiotherapy stack, connecting devices from rival manufacturers that can’t easily talk to one another.

Every incremental OEM partnership strengthens this neutrality moat.

R&D depth and regulatory flywheel:

With 20+ years of accumulated datasets, RaySearch continuously updates its dose-optimization algorithms, adaptive planning modules, and machine-learning contouring tools.

Its regulatory-clearance rhythm (FDA, EMA, Japan PMDA) gives it first-mover advantage in adopting new modalities (e.g., FLASH radiotherapy).

The result is an R&D cadence that compounds defensibility: every new clinical feature expands switching costs and drives recurring upgrade revenue.

Recurring revenue and pricing power:

Software licenses are sold under multi-year contracts with ongoing support and maintenance fees.

As treatment complexity rises (AI planning, adaptive radiotherapy, hypofractionation), hospitals must keep systems current, giving RaySearch built-in recurring revenue with inflation-indexed pricing.

It’s a razor-and-blade model, sell the license once, monetize upgrades forever.

Bottlenecks

Regulatory-cleared innovation:

Every algorithm, module, and interface in radiotherapy must be clinically validated and regulator-approved before deployment.

RaySearch’s in-house regulatory team has become an invisible moat, a global compliance engine fluent in FDA, CE, and PMDA pathways.

Competitors (including OEMs) can’t move at this pace because they lack dedicated regulatory bandwidth; RaySearch ships faster and scales globally.

Integration inertia (workflow as gravity):

Radiotherapy departments are ecosystems with fixed workflows, staffing hierarchies, and treatment protocols.

Once RayStation defines those workflows, it becomes the standard of care within the institution, physicians are trained on it, templates are built around it, and billing codes reference it.

This inertia compounds adoption: when staff migrate to other hospitals, they advocate for the same system they already know.

Data ownership and analytics lock:

RaySearch accumulates anonymized treatment data across modalities and centers, allowing machine-learning optimization unavailable to newcomers.

This growing data corpus is both an innovation engine and a defensive shield, no new entrant can replicate 20 years of annotated radiation-dose outcomes.

Trip-Wires / KPIs to Monitor

Net new center wins: Growth in global radiotherapy footprint, particularly in emerging markets (India, China, Latin America) where new centers are being built from scratch.

Module attach rates: Upgrades from planning-only (RayStation) to full workflow (RayCare) and analytics packages, a key driver of ARR growth.

AI-enabled feature launches: Adoption of auto-contouring and adaptive planning modules; a leading indicator of long-term lock-in.

Proton therapy expansion: New center openings using RayStation as the default; expansion into heavy-ion therapy planning could be the next catalyst.

Recurring revenue mix: Monitor subscription vs perpetual license ratio; higher maintenance share = higher margin durability.

R&D cadence: Regulatory approvals for FLASH or carbon-ion therapy planning, next-generation modalities that could open new markets.

Variant Risk

Vendor bundling threats: Large OEMs (Varian/Siemens) could attempt to enforce tighter integration between their hardware and proprietary software.

However, hospitals value independence; RaySearch’s neutrality remains its best defense.

Hospital budget pauses: Radiotherapy software is capital expenditure; prolonged macro tightening could delay upgrades, though maintenance renewals remain steady.

Technological displacement risk: Long-term emergence of AI-native planning systems could disrupt parts of the workflow, though RaySearch is already embedding ML into its core engine.

Summary View

RaySearch is a critical-utility business inside oncology, with economic characteristics closer to enterprise software than biotech. It benefits from structural switching costs, cross-hardware compatibility, and regulatory entrenchment that make it almost impossible to displace once installed. While most investors chase molecules, RaySearch captures perpetual royalties on radiation therapy itself, not per dose, but per workflow. It’s the definition of a “mission-critical moat” in healthcare software: essential, invisible, and compounding. Own the picks-and-shovels of oncology, a global software monopoly on the infrastructure of precision cancer treatment.

7) Giant Biogene (2367 HK) — Collagen as an Enduring Franchise

Giant Biogene has quietly established itself as China’s recombinant collagen champion, commanding dominant share in medical-grade skincare, wound care, and aesthetic dermaceuticals. It’s a biotech manufacturer disguised as a consumer healthcare brand, combining IP, production scale, and clinical credibility into one of Asia’s most profitable healthcare franchises. Its moat stems from proprietary collagen synthesis technology, high regulatory barriers, and a unique dual exposure to medical and aesthetic markets that yield pricing power and diversification.

Moats

Process IP & manufacturing scale:

Proprietary recombinant yeast-expression system for human collagen eliminates animal-derived inputs, giving Giant Biogene a purity and consistency advantage critical for medical-grade use.

The company owns hundreds of patents covering strains, purification, and formulation. Replicating this end-to-end process requires years of strain engineering and GMP validation.

Dual-channel model (medical + aesthetic):

The company sells collagen wound dressings and gels through hospitals while also marketing high-end dermaceutical products for post-procedure recovery and sensitive skin.

Medical distribution provides stable, policy-backed revenue, while aesthetic skincare captures consumer-margin upside.

This mix reduces cyclicality, a rarity among Chinese health and beauty peers.

Regulatory moat:

Operating in China’s tightly regulated medical device and cosmetics ecosystem, Giant Biogene has built first-mover licenses and quality certifications that take competitors years to replicate.

Its long relationship with provincial health bureaus ensures fast-track product approvals and hospital tender wins, an institutional moat beyond patents.

Brand equity & trust:

The company’s products are prescribed by clinicians for wound healing and post-surgical recovery, conferring a halo of clinical legitimacy to its consumer line.

This “medicalized skincare” positioning commands premium pricing in a crowded cosmetic market.

Bottlenecks

Strain reproducibility:

Consistent recombinant yield requires proprietary bioprocessing controls; not all CDMOs can replicate the same expression levels or purity.

Clinical tender access:

China’s hospital system is relationship- and documentation-heavy; the company’s established KOL network acts as a gatekeeper for new entrants.

Regulatory cadence:

Each new product class demands fresh local clinical validation, a process where experience and data archives become competitive armor.

Trip-Wires / KPIs

Hospital penetration: Number of new tenders/hospitals added per quarter; proxy for share expansion in wound care.

Export pipeline: Entry into Southeast Asian and Middle Eastern markets through licensing; optionality for revenue diversification.

Margin stability: Maintaining 80%+ gross margins as consumer mix rises; a test of pricing power and product loyalty.

Variant Risk

Policy-driven price compression: Centralized tenders could lower medical collagen ASPs.

Macro sensitivity: Aesthetic skincare may soften during consumption slowdowns.

Regulatory drift: Stricter cosmetics oversight could delay new SKU launches.

Summary View

Giant Biogene owns the collagen supply chain end to end, from proprietary yeast strains to hospital distribution. It’s less a cosmetics play than a regulated biotech franchise monetizing medical-grade IP at consumer multiples. With entrenched hospital ties, unmatched margins, and a hybrid revenue model, the company epitomizes “rare by design” in Asia’s healthcare landscape. Own the collagen monopoly, biotech precision, consumer scale, medical trust.

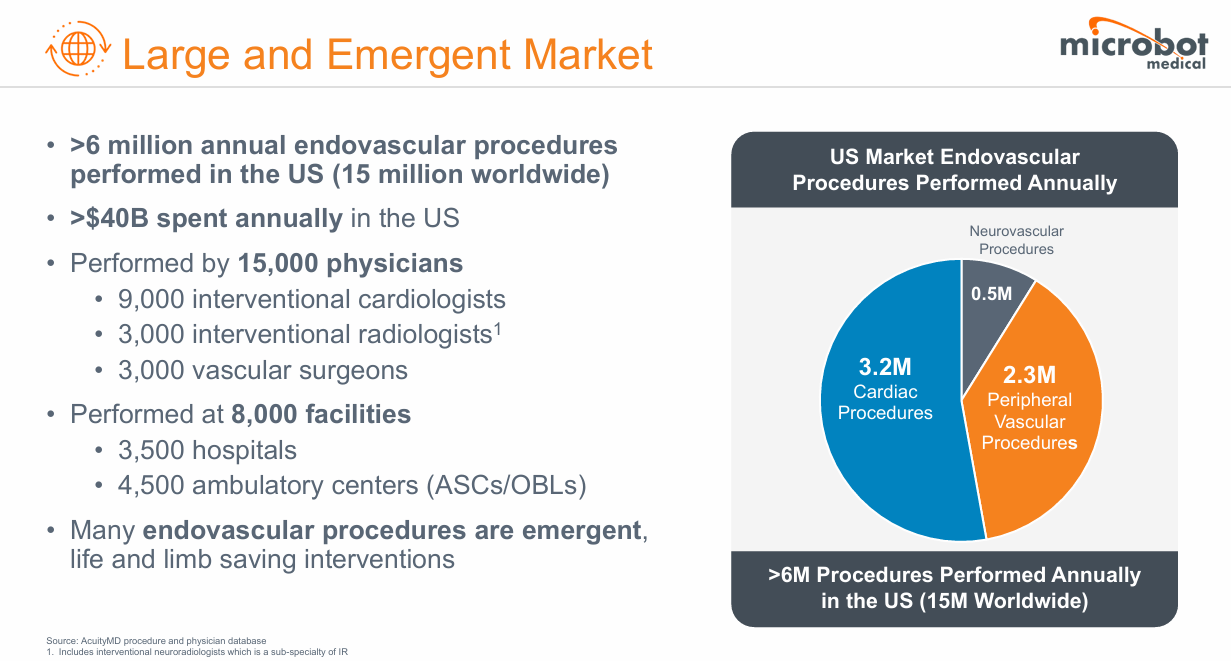

8) Microbot Medical (MBOT) — Disposable Robotics, Infinite Leverage

Microbot Medical is pioneering the first fully disposable endovascular micro-robotic system, a concept that could democratize interventional care the way single-use laparoscopic tools transformed surgery. Its flagship device, LIBERTY, is designed to perform remote, minimally invasive vascular procedures without large capital robots or on-site specialists. The opportunity is binary but asymmetric: if FDA clearance arrives on schedule, MBOT could own the intellectual and regulatory ground floor of a new medical device category.

Moats

Category-creating IP:

LIBERTY’s broad patent estate covers mechanical design, navigation algorithms, and disposable robotic actuation, effectively blocking fast followers from entering the same design space.

The concept merges robotic precision with single-use economics, addressing infection control, setup time, and capital cost barriers that limit robotic surgery adoption today.

Regulatory first-mover advantage:

LIBERTY holds FDA Breakthrough Device designation, enabling priority review and streamlined clinical dialogue.

Being first through the FDA pathway creates a de facto regulatory moat, future entrants must conform to the standards MBOT sets.

Workflow moat (access expansion):

By eliminating bulky consoles and infrastructure, LIBERTY allows small hospitals and rural centers to perform neurovascular and peripheral interventions remotely.

This expands the TAM rather than cannibalizing existing robotics players like Intuitive Surgical or Corindus (Siemens).

Bottlenecks

Human-factors reliability:

Single-use robotics must prove consistency across thousands of disposables; scaling precision manufacturing and QC is a nontrivial engineering challenge.

Reimbursement coding:

The path to adoption depends on CPT/DRG code assignment — without it, hospitals can’t bill. MBOT’s early engagement with payors is essential.

Capital access:

As a pre-revenue microcap, progress hinges on bridge financing or strategic partnerships post-FDA clearance.

Trip-Wires / KPIs

Pivotal trial milestones: Enrollment completion and top-line data in 2025.

FDA submission/decision: Potential 2025–26 approval under Breakthrough review track.

Partnership announcements: OEM alliances or distribution deals with major medtechs.

Cash runway: At least 12 months post pivotal readout.

Variant Risk

Execution risk: Manufacturing scale-up or trial complications could defer clearance.

Dilution risk: Additional capital raises likely pre-launch.

Competitive re-entry: Larger device makers may respond with semi-disposable systems once the category proves viable.

Summary View

Microbot is a convex bet on procedural access: one FDA win could unlock a multibillion-dollar procedural TAM with modest capital intensity. It’s speculative but structurally original, a disposable robotics model that could define a new subfield. First to file, first to clear, first to scale, own the blueprint for disposable surgical robotics.

9) Avanos Medical (AVNS) — The Quiet Fortress in Pain & Care

Avanos is a steady compounder hiding inside healthcare’s most entrenched infrastructure, pain management and enteral feeding systems. Spun out of Kimberly-Clark, it operates in slow-moving, regulation-heavy niches where safety, clinician familiarity, and reimbursement stability create natural barriers to entry. It’s not a growth rocket; it’s a formulary fortress that compounds through procedural inertia and steady policy tailwinds away from opioids.

Moats

Formulary & training lock:

Avanos’s Coolief radiofrequency ablation system and On-Q pain pumps are embedded in hospital pain protocols nationwide.

These devices are included in standard-of-care guidelines and bundled reimbursement codes, once adopted, switching costs span retraining, credentialing, and new approvals.

In enteral feeding, its Corpak brand commands trust among dietitians and ICU staff, cemented by years of safe-use data.

Regulatory & brand credibility:

Medical device regulation favors incumbents. Coolief was the first FDA-cleared RF system for osteoarthritis pain, and that regulatory first-mover status sustains payer recognition and physician loyalty.

The company’s reliability in high-risk care settings (ICU, post-op, long-term feeding) gives it a brand moat built on safety, not marketing.

Macro tailwinds:

The global shift toward non-opioid pain interventions and aging demographics expands demand for Avanos’s core offerings.

Hospitals value predictability and compliance more than disruption, a structural advantage for incumbents like Avanos.

Bottlenecks

Clinical inertia:

Procedures and device preferences in pain management evolve slowly; this inertia preserves Avanos’s installed base.

Procurement friction:

Hospital supply contracts renew infrequently and require vendor audits, creating long replacement cycles that insulate market share.

Trip-Wires / KPIs

Coolief utilization growth across orthopedic and spine centers.

Gross margin trajectory as product mix shifts toward higher-margin pain therapies.

Recall-free operation, execution quality is the moat’s daily test.

Variant Risk

Pricing pressure: Hospital procurement could push for incremental discounts.

Volume stagnation: If elective procedures slow, near-term utilization softens.

Acquisition premium risk: Larger medtechs could buy Avanos before market fully prices in its stability.

Summary View

Avanos is quietly monetizing the status quo of safe, reimbursed, repeatable care. It adds stability and low beta to the RAREDIS² sleeve, balancing the higher-volatility biotech names. In a sector chasing novelty, Avanos compounds by being the brand hospitals don’t replace. Own the pain franchise no one wants to switch from, a steady earner in an opioid-averse world.

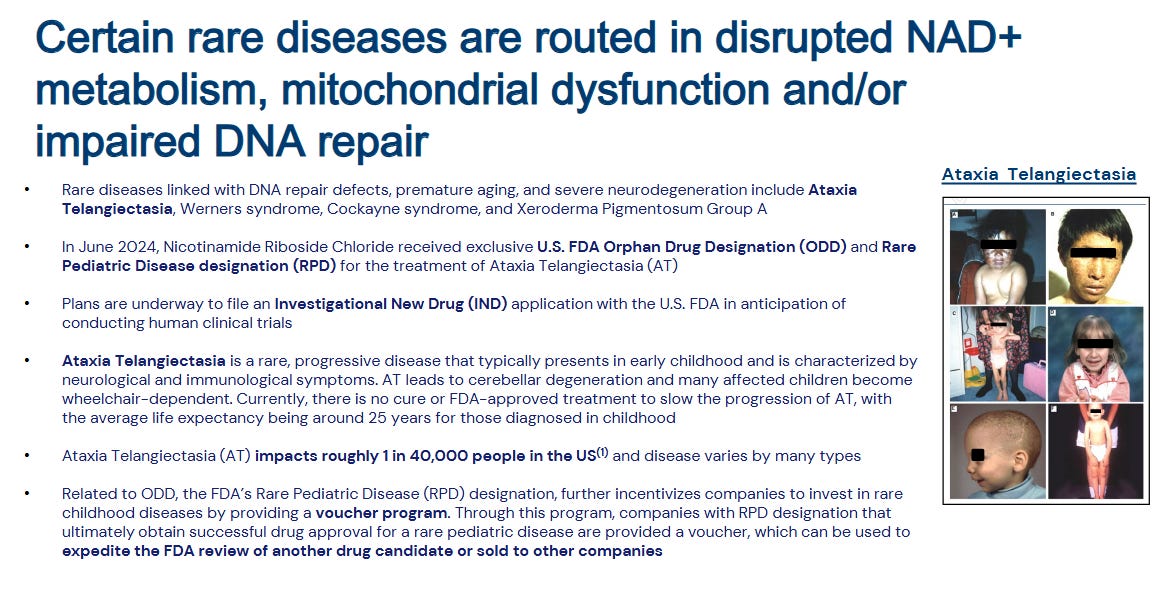

10) Niagen Bioscience (NAGE) — Patented Longevity in a Capsule

Niagen Bioscience (formerly ChromaDex) is the purest intellectual-property play on NAD⁺ biology, the cellular coenzyme tied to energy metabolism, aging, and repair. Its patented compound, nicotinamide riboside (NR), branded as Niagen®, is the only FDA-vetted NAD⁺ precursor with GRAS status and a clean human-safety dossier. Unlike speculative “longevity” plays, Niagen already sells a profitable product line and supplies ingredient partnerships to major CPG and nutrition brands. It’s a cash-generating moat built on regulatory legitimacy and scientific credibility.

Moats

Ingredient IP + safety dossier:

Niagen holds composition-of-matter and use patents around NR production and absorption pathways, defended successfully against multiple challengers.

It is the only NAD⁺ precursor recognized as Generally Recognized as Safe (GRAS) by the FDA, a regulatory barrier competitors can’t easily breach.

That certification allows Niagen to sell into both nutraceutical and pharmaceutical channels without re-validation.

Science & credibility moat:

Backed by over 100 peer-reviewed studies and 25+ clinical trials, NR’s effects on mitochondrial efficiency, muscle recovery, and metabolic health make it the benchmark compound in the NAD⁺ category.

Competitors like NMN and NRH remain unapproved or untested in humans, giving Niagen category authority among physicians and researchers.

Dual-channel monetization:

Operates a hybrid model: B2B ingredient supply (to Nestlé and Thorne) and direct-to-consumer brand (Tru Niagen).

This structure compounds margin leverage, ingredient sales scale with partners, while the DTC channel captures premium brand value.

Gross margins above 60% and consistent free cash flow make NAGE a profitable outlier in biotech-adjacent wellness.

Distribution & brand moat:

Years of consumer education, FDA correspondence, and supply reliability have created channel lock-in with retailers and supplement partners.

Shelf space and brand trust in the supplement sector are slow-cycle assets, once established, they rarely change hands.

Bottlenecks

Manufacturing purity:

Pharmaceutical-grade NR requires high-precision crystallization and stability control; only Niagen’s facility and contracted GMP partners can consistently meet specs.

Scientific validation cadence:

Each new claim (e.g., cognitive health, metabolic support) requires multi-year trials, Niagen’s existing safety data accelerates this loop, forming a time-based moat competitors can’t shortcut.

Trip-Wires / KPIs

New B2B launches with global CPG partners expanding beyond the U.S.

Clinical readouts confirming therapeutic potential in rare mitochondrial or aging-related disorders (e.g., Cockayne syndrome).

Margin resilience as ingredient volumes scale faster than marketing spend.

Regulatory posture: Continued FDA acceptance of NR as supplement-safe amid tightening oversight on NMN.

Variant Risk

Category confusion: Shifting consumer interest toward unregulated NMN compounds could divert near-term retail demand.

Policy risk: Changes to supplement-drug classification could raise compliance costs.

Science perception: A failed or inconclusive longevity trial could momentarily dampen investor sentiment.

Summary View

Niagen Bioscience monetizes aging science without the binary risk, a patented molecule, proven safety, and growing consumer adoption. It’s a compounder of trust: recurring ingredient royalties, expanding DTC margins, and embedded regulatory advantage. NAGE provides low-beta, cash-positive exposure to a megatrend, cellular rejuvenation, anchored by real IP and real profits. Own the only longevity molecule with patents, profits, and permission.

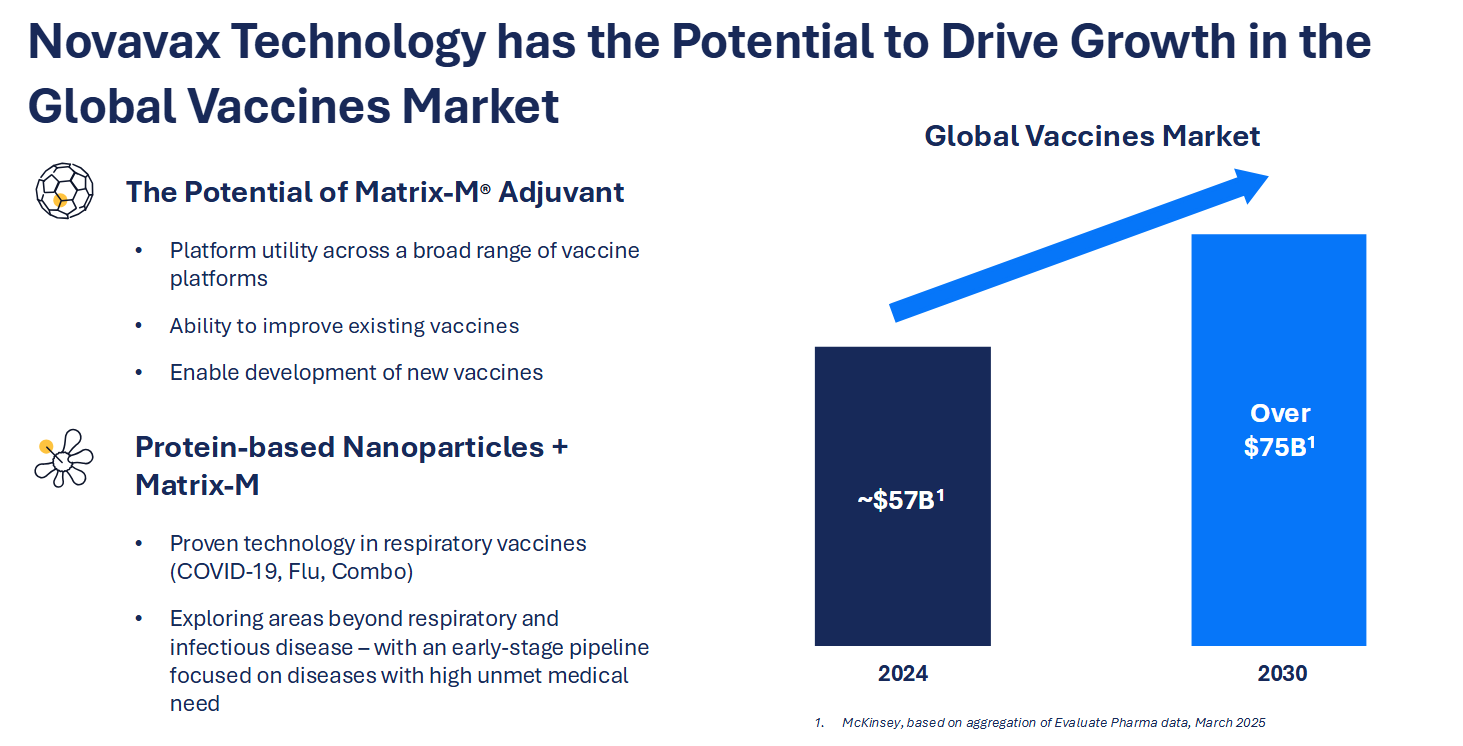

11) Novavax (NVAX) — The Protein Vaccine Countertrade

Novavax remains one of the few independent vaccine makers with a proven, scalable alternative to mRNA, a recombinant protein platform paired with its proprietary Matrix-M adjuvant. Post-COVID, it has refocused on sustainable markets: combination respiratory vaccines, global booster contracts, and adjuvant licensing. Beneath the volatility, Novavax owns a rare asset trifecta, a validated antigen production process, a differentiated adjuvant with external royalties, and an FDA-approved manufacturing network. The story now is less redemption, more re-industrialization of vaccines.

Moats

Adjuvant IP (Matrix-M):

Derived from Quillaja saponaria, Matrix-M enhances immune response at lower antigen doses.

It is already licensed into Oxford/Serum Institute’s malaria vaccine, generating royalties and giving Novavax credibility as a technology provider, not just a manufacturer.

Only a handful of adjuvants are globally approved; this is one of them — a toll-road asset other vaccine developers must rent.

Platform flexibility:

Protein subunit vaccines have simpler storage, better thermostability, and lower reactogenicity than mRNA, critical for global tenders.

The same core process can produce COVID, flu, RSV, or combination vaccines by swapping antigens, a modular manufacturing moat with minimal retooling costs.

Manufacturing scale & regulatory goodwill:

After ramping during the pandemic, Novavax owns FDA-approved, WHO-qualified facilities and validated global supply chains.

That infrastructure is costly to rebuild; many peers are outsourcing or mothballing. Novavax now rents its excess capacity, turning fixed cost into optionality.

Non-mRNA market positioning:

As skepticism toward mRNA’s side-effect profile persists in parts of the world, Novavax captures vaccine-hesitant and government diversification demand.

This creates durable niche demand even in a post-pandemic market.

Bottlenecks

Regulatory dependency:

Respiratory vaccine cycles hinge on annual strain selection; regulatory coordination is a timing bottleneck.

Working-capital sensitivity:

Inventory and tender schedules create short-term balance-sheet swings; disciplined production planning is key.

Adjuvant scaling:

Matrix-M’s natural raw materials and extraction complexity limit how fast capacity can expand.

Trip-Wires / KPIs

Combo COVID-Flu (CIC) trial readouts, proof of platform breadth.

RSV Phase 3 data and regulatory filings in adults.

Adjuvant licensing deals beyond malaria; royalties are the cleanest margin.

Cash balance trajectory, maintaining positive free cash flow post restructuring.

Global procurement contracts for 2026-27 seasonal vaccines.

Variant Risk

Demand volatility: COVID booster orders remain unpredictable; any mismatch between production and tenders hits cash flow.

Execution risk: Repeated delays or manufacturing miscues could re-ignite credibility concerns.

Competition: Combined vaccines from Pfizer/Moderna could crowd the respiratory space.

Policy exposure: Government tender pacing drives quarter-to-quarter earnings volatility.

Summary View

Novavax is evolving from pandemic boom-bust to steady platform operator: a royalty-earning adjuvant supplier, lean vaccine producer, and optional call on new outbreaks.

It’s under-owned, cash-positive, and uncorrelated to both mRNA hype and biotech beta, an asymmetric recovery trade inside a proven global infrastructure. Own the anti-mRNA toll road, a proven adjuvant, modular vaccine platform, and balance-sheet leverage to the next respiratory cycle.

Why Short Both XBI and PPH (50/50)

XBI (equal-weight biotech)

What we hedge: Pre-revenue churn, clinical blow-ups, meme squeezes, factor rotations.

Equal-weighting forces buy/hold of lower-quality tails; rebalance mechanics buy losers.

Offsets sector-wide drawdowns that do not impair our moats.

PPH (mega-cap pharma/biotech)

What we hedge: Crowded mega-cap narratives (GLP-1, Alzheimer’s) + drug-pricing regimes.

Top-heavy baskets can unwind sharply on single trial or policy shock.

Lower beta than XBI dampens hedge vol while catching policy/pricing risk.

Our longs span software, devices, orphan therapies, IP toll-roads, low overlap with both ETFs. The pair neutralizes junk beta and crowded mega-cap beta simultaneously.

Conclusion

This index concentrates on companies that control bottlenecks: IP toll roads, orphan exclusivity, installed clinical software, and specialized manufacturing and hedges sector noise with XBI/PPH shorts. This construct seeks repeatable alpha from durable moats while muting macro/policy beta and ETF factor churn.

Basket Weighting Recap:

Disclaimer:

Ridire Research is an independent research publication operated by Ridire Research LLC and affiliated with a private fund, an Exempt Reporting Adviser under the U.S. Investment Advisers Act of 1940. Ridire Research is not registered as an investment adviser and does not provide personalized investment, legal, accounting, or tax advice.Informational & Educational Purpose Only

All materials—including text, charts, model portfolios, and explicit labels such as “Buy,” “Sell,” “Hold,” “Long,” or “Short”—are published solely for general informational and educational purposes. They reflect the author’s views at the time of writing, derived from publicly available data, proprietary frameworks, and market analysis, and are not tailored to any reader’s specific objectives, financial situation, or risk tolerance. Subscription to this Substack does not create an adviser–client relationship with the affiliated private fund or its principals.

No Offer or Solicitation

Nothing herein constitutes (i) an offer to sell or the solicitation of an offer to buy any security or other instrument, (ii) a recommendation to participate in any investment strategy, or (iii) a solicitation for investment advisory services. Any references to trades, allocations, or vehicles should be viewed as hypothetical model illustrations only. Offers, if ever made, will be made solely by confidential offering documents and only to qualified investors in jurisdictions where permitted.

Potential Conflicts of Interest

The affiliated private fund, its affiliates, employees, and related accounts may hold, increase, decrease, initiate, or exit positions, long or short, in securities or digital assets discussed, without notice or obligation to update disclosures. Such positions may be inconsistent with views expressed in this publication. The affiliated private fund, related entities, and personnel may initiate, modify, or exit positions in any mentioned security before or after publication without further notice. We maintain internal policies, including trading blackout windows and conflict reviews, to mitigate potential conflicts of interest.

Accuracy & Forward-Looking Statements

Although we strive for accuracy and analytical rigor, information may become outdated and may contain errors or omissions. Forward-looking statements, projections, or target prices are inherently uncertain and may differ materially from actual results. No warranty, express or implied, is given as to completeness, accuracy, or reliability.

Risk Acknowledgment

Investing involves substantial risk, including the potential for complete loss of capital. Past performance, whether actual, indicated by back-tests, or modeled, is not indicative of future results. Securities, derivatives, and digital assets mentioned may be illiquid, highly volatile, or subject to regulatory change.

Reader Responsibility

Readers should conduct their own due diligence, consider their personal circumstances, and consult a licensed financial professional before acting on any information contained herein. By reading this publication you agree that Ridire Research LLC, the affiliated private fund, and their affiliates accept no liability for any direct or consequential loss arising from reliance on the information presented. This research is not directed at persons in jurisdictions where such distribution would be contrary to local law.

Hey, great read as always, thanks for breaking down these bottlenecks so clearly, it's truely fascinating how crucial those 'moats' are for true innovation.