Ridire Research: Year in Review

Best Ideas, Worst Ideas, and Biggest Fades

Table of Contents

Introduction

Top 5 Ideas of the Year

Worst 5 Ideas of the Year

Biggest Fades

What This Year Reinforced

Introduction:

This year some ideas worked exceptionally well. Others didn’t. Both outcomes matter.

What follows is a transparent review of the top 5 performing ideas and worst 5 performing ideas published this year, measured from publication to end of year. All links are included so readers can review the previous articles.

A dedicated section for Biggest Fades sits at the bottom, ideas I watched work in real time without ever stepping in. In many ways, these missed opportunities are more painful than the ideas that didn’t work.

Top 5 Ideas of the Year

These ideas shared a common thread: structural tailwinds + mispriced narratives + asymmetric setups.

1. January 26 Calls on LC US +342.1%

This idea focused on a perceived valuation and classification mismatch rather than a directional macro call. The central observation was that LendingClub continued to be valued like a traditional regional lender, despite already operating as a profitable, AI-enabled digital bank with scale.

At the time of publication, LendingClub was originating more than $2 billion in loans per quarter, growing volumes at a double-digit rate, yet trading near tangible book value. The market largely overlooked the company’s underwriting infrastructure, which leverages one of the deepest consumer credit datasets in the industry: over 15 years of labeled outcomes and more than 100 billion data points. Incremental AI capability was being added through small, targeted acquisitions, improving credit performance and operating efficiency.

These advantages were already visible in reported results. Credit losses declined materially year over year, whole-loan sale pricing improved, and margins expanded, even as peers faced deteriorating credit trends. The company’s strong capital position further supported the durability of the business model.

The idea ultimately benefited from the market beginning to reassess LendingClub as a “second-derivative” AI credit platform, one where artificial intelligence was not a speculative future initiative, but a system already embedded in underwriting and economics. As that recognition improved, valuation followed.

In hindsight, the strength of this idea came from focusing on what was already working in the data, rather than what management hoped to build, and identifying where market perception lagged operational reality.

2. The Moat That Closes With Every Mortgage +75.7%

This was not a simple call on falling rates or a housing rebound. The core thesis was that Rocket Companies was being mispriced as a cyclical mortgage originator, when in reality it is in the process of becoming a vertically integrated, end-to-end housing platform.

The acquisitions of Redfin and Mr. Cooper, alongside the simplification of Rocket’s Up-C structure, materially changed the company’s earnings durability and strategic optionality. Redfin added top-of-funnel traffic and a national brokerage footprint, while Mr. Cooper brought scale servicing, recurring cash flow, and customer lifetime value. Together, they create a flywheel for retention, cross-sell, and structurally lower customer acquisition costs, something the market was slow to appreciate.

Operationally, Rocket continued to execute. AI-driven automation improved productivity and lowered costs, market share was gained even in a weak housing environment, and the balance sheet remained fortress-like. Importantly, the thesis also acknowledged macro uncertainty: servicing income and a flexible cost base helped offset higher-for-longer rate risk.

To further balance rate exposure, the idea was paired with copper producers (ERO CN and CS CN), a deliberate hedge against re-accelerating inflation or rising rates. This created a more robust expression across both rate-sensitive and inflation-sensitive regimes, rather than a one-way macro bet.

In hindsight, the strength of the idea came from treating Rocket as an emerging housing ecosystem, not a levered duration trade, and from structuring the idea to survive multiple macro outcomes.

3. Tariff to Table (LS) +74.6%

This idea examined the U.S.–U.K. Economic Prosperity Deal (EPD) as a rare, discrete policy catalyst capable of reshaping cross-Atlantic flows in both agricultural commodities and digital services. Rather than treating the agreement as a headline geopolitical event, the research focused on how specific quota creation, tariff removal, and regulatory harmonization would create winners and losers across adjacent industries.

The framework centered on expressing the downstream effects of regulatory clarity, where new access, cost advantages, or competitive pressure were likely to emerge, while contrasting businesses positioned to benefit from the agreement with those facing incremental margin or valuation risk.

U.S. Agricultural Export Beneficiaries

The EPD introduced a preferential duty-free ethanol quota for U.S. producers and removed tariffs on U.S. beef exports into the U.K. This materially altered export economics for select U.S. agricultural firms. The idea highlighted companies with modern production assets, export readiness, and scale advantages, where incremental international demand could flow directly into margins. Management commentary at the time reinforced that regulatory-aligned international demand was becoming a more meaningful earnings driver.

U.K. Domestic Protein Pressure

On the other side of the trade, the agreement increased competitive pressure on U.K.-centric protein producers. The introduction of tariff-free U.S. beef created the risk of import-driven price competition in a market already facing cost inflation. Businesses with limited geographic diversification and exposure to domestic fresh-protein pricing were identified as structurally more vulnerable to margin compression as supply dynamics shifted.

Digitized Trade Enablement vs. Consumer SaaS

Beyond physical goods, the EPD placed explicit emphasis on digital trade provisions, including paperless customs processes and harmonized digital standards. The research differentiated between platforms that directly enable cross-border commerce, through tariff calculation, VAT handling, and compliance workflows, and consumer-facing software businesses with limited linkage to trade infrastructure. The former stood to benefit from increased cross-border activity and regulatory normalization, while the latter faced the risk of relative multiple compression as capital rotated toward policy-aligned platforms.

In hindsight, the strength of this idea came from treating the EPD not as a macro headline, but as a microeconomic shock that reallocated value across supply chains and software layers. By focusing on second-order effects, who gains access, who absorbs competition, and who enables the system, the framework captured dispersion that broad market narratives missed.

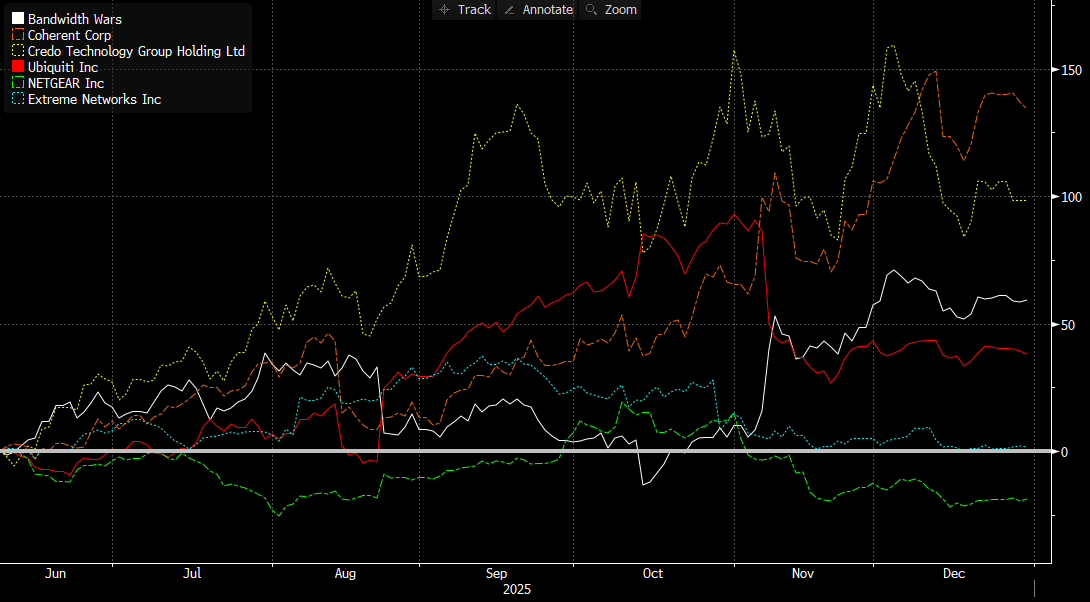

4. Bandwidth Wars (LS) +58.8%

This idea examined the growing bifurcation within the global connectivity ecosystem. While “networking” is often discussed as a single sector, the research argued that the market was increasingly splitting into two distinct camps: companies enabling the next wave of bandwidth expansion and convergence, and legacy vendors tied to slower-growth, increasingly commoditized segments.

Rather than making a directional call on technology or equity markets broadly, the work focused on relative fundamentals inside the connectivity stack, who is positioned to benefit from secular demand for bandwidth, and who faces structural headwinds as architectures evolve.

Enablers of the Bandwidth Expansion

The research highlighted companies supplying critical technology for modern connectivity buildouts, including virtualized broadband access, optical transport, and high-speed datacenter interconnect. These businesses sit directly in the path of several durable trends: DOCSIS 4.0 and fiber upgrades, hyperscale cloud and AI datacenter expansion, and the shift toward software-defined, higher-capacity networks.

Across this group, common characteristics emerged: exposure to customer capex that is strategic rather than discretionary, improving product mix, and demand driven by physics (speed, power, latency) rather than refresh cycles. Product roadmaps centered on next-generation technologies such as virtualized access platforms, 800G+ optical links, and high-speed electrical interconnects designed for AI clusters. In many cases, fundamentals reflected this positioning through stronger growth, margin expansion, and improving balance sheet profiles.

Legacy Connectivity and Structural Pressure

In contrast, the research identified connectivity vendors whose core exposure remains tied to mature or saturated markets such as consumer Wi-Fi hardware, SMB networking, or traditional enterprise campus networks. While some of these businesses are well run and profitable, their end markets face slower growth, heightened competition, and increasing commoditization.

These companies tend to rely on incremental product updates, cyclical refresh demand, or cost discipline rather than participation in the fastest-growing areas of network spending. As customer budgets increasingly prioritize broadband infrastructure, cloud interconnect, and AI-driven capacity expansion, legacy segments risk being deprioritized.

Why Dispersion Matters

The central insight of this idea was that connectivity demand is simply reallocating. Bandwidth requirements continue to rise from the last mile to the core, but value accrues unevenly depending on where a company sits in the architecture. Firms enabling convergence, virtualization, and scale stand to benefit disproportionately, while those anchored to box-based or fragmented niches face relative erosion.

By focusing on this internal dispersion rather than the sector as a whole, the idea captured performance differences driven by technology relevance, customer mix, and capital allocation priorities, rather than broad market direction.

In hindsight, the success of this idea came from recognizing that the future of connectivity belongs to those enabling greater bandwidth, efficiency, and integration, and that legacy hardware models, while often optically cheap or operationally stable, remain structurally disadvantaged as the connectivity cycle evolves.

5. The Skeleton Crew +48.7%

This idea focused on a simple but non-consensus observation: the next wave of automation would not be led by abstract AI models alone, but by physical robots, increasingly humanoid in design, enabled by mature sensors, compute, and motion control systems. The value was expected to accrue not to any single robot form factor, but to the upstream suppliers providing the indispensable “bones and guts” of every robotic system.

Rather than speculating on which humanoid platform might win, the research emphasized infrastructure inevitability. Every general-purpose robot, regardless of brand or design, requires dense edge compute, high-reliability power management, precise sensing, motion control, and rigorous semiconductor testing. These needs exist independently of marketing narratives or end-user hype.

Why the Timing Mattered

The work argued that several forces had converged to push robotics out of the lab and into commercial deployment: persistent labor shortages, rising wages in logistics and manufacturing, improvements in real-time AI inference, and declining hardware costs. Together, these factors created a tipping point where general-purpose robots became economically viable rather than experimental.

Upstream Enablers Over End Products

The core insight was that the most durable value would likely accrue to companies supplying:

Edge AI compute and robotics software stacks

Analog, power, and sensing components embedded in every joint and actuator

Semiconductor test, packaging, and inspection tools required to manufacture advanced robotics chips

Optical and display technologies that support perception, interaction, and monitoring

These layers benefit regardless of which OEM ultimately dominates humanoid deployment.

Early Identification of the Robotics–Test Nexus

Notably, this research highlighted Teradyne’s dual exposure to robotics well before it became widely discussed. The analysis connected Teradyne’s ownership of Universal Robots and MiR, among the most widely deployed collaborative automation platforms, with its dominant position in semiconductor test. As robot intelligence increases, so does chip complexity, and every advanced processor, sensor, and memory component must be validated. This “picks-and-shovels” exposure to both physical automation and the silicon underneath it was identified early, ahead of broader commentary elsewhere (wink wink).

A Stack, Not a Bet

The strength of the idea lay in treating robotics as a stack. Compute providers, analog leaders, packaging specialists, optical equipment makers, and test vendors all occupy chokepoints with high switching costs and long design cycles. Many of these businesses already generate revenue from adjacent markets (cloud, automotive, industrial), giving them resilience while robotics adoption scales.

In hindsight, the effectiveness of this idea came from separating inevitability from uncertainty. The exact shape of humanoid robots remains fluid. The need for compute, power, sensing, testing, and integration does not. By focusing on the latter, the research captured exposure to the automation inflection without relying on speculative end-state winners.

Worst 5 Ideas of the Year

These ideas failed for different reasons: regime mismatch, narrative persistence, or being right too early (also called being wrong until further notice). Each one highlighted a weakness worth addressing.

1. LS Cash Flow Cosmetics (LS) -18.5%

This idea examined a structural divergence in global beauty, contrasting digital-first, science-led operators with diversified geography against a legacy prestige player reliant on travel retail and wholesale distribution.

The core thesis remains intact, but the idea proved too early. While channel pressure in travel retail and capital allocation constraints were correctly identified, the market proved willing to look through near-term disruption, restructuring, and China uncertainty for longer than expected.

Digital-native and IP-driven brands continue to deepen moats through data, proprietary formulations, and embedded distribution, while legacy prestige models face slower channel recovery and rising competition. The disconnect lies in timing of recognition, not in the underlying analysis.

This was a reminder that structural edges can take longer to surface in consumer sectors, and that patience, not conviction, was the missing ingredient here.

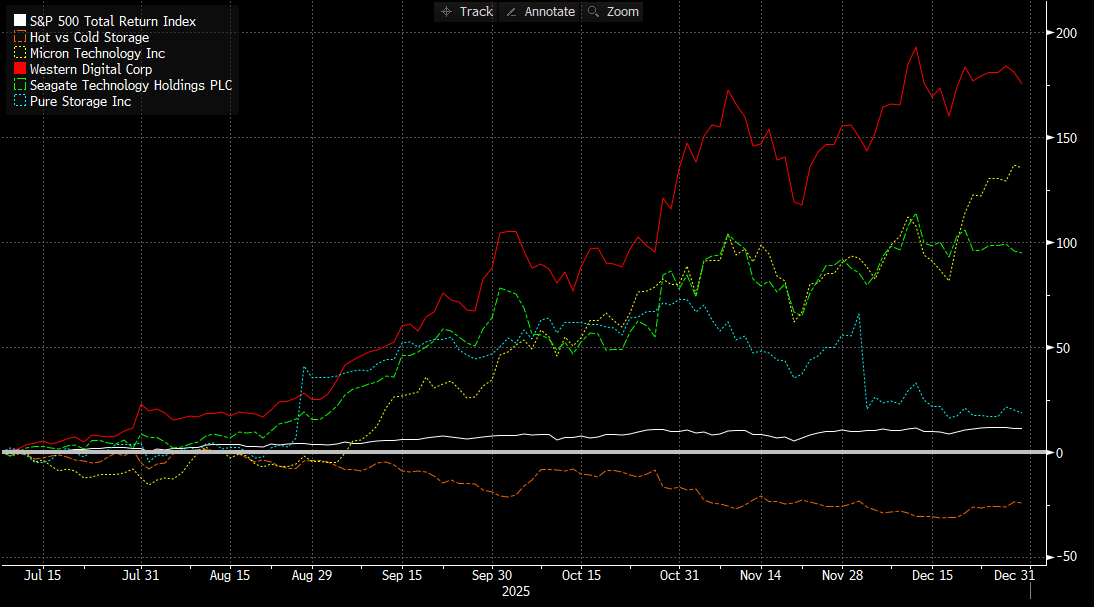

2. Hot vs Cold Storage (LS) -24.1%

This idea focused on a structural shift in data infrastructure: AI workloads increasingly favor low-latency, high-throughput storage over traditional hard-disk–based capacity. The analysis correctly identified flash, high-bandwidth memory, and modern networking as long-term beneficiaries, while legacy disk-centric models faced rising relevance risk.

The issue was timing and relative scale. Hyperscalers proved more willing than expected to extend HDD lifecycles for deep-archive and cold tiers, delaying the point at which latency economics fully dominated procurement decisions. At the same time, early AI-driven storage demand was simply too small, relative to the massive installed HDD base, to force immediate displacement. Capacity roadmaps and pricing discipline from disk vendors further slowed near-term disruption.

That said, the underlying physics have not changed. AI clusters remain constrained by data movement, not raw capacity, and capital spending continues to migrate toward flash, NVMe fabrics, and high-speed networking. This was a case where the destination appears right, but the path is unfolding more slowly and unevenly than anticipated.

3. Rare by Design (LS) -28.1%

Rare by Design

In an environment where biotech volatility is driven more by macro flows and sentiment than fundamentals, we propose a deliberately constructed long/short: long a focused basket of rare-disease leaders (RAREDIS Index), short the SPDR S&P Biotech ETF (XBI).

This idea was built around a clear structural view: cash-generative, orphan-focused biopharma businesses with pricing power and execution discipline should outperform a broad biotech index dominated by speculative, pre-revenue names. Fundamentally, that view held, many rare-disease companies continued to grow revenue, expand margins, and raise guidance.

The problem was the hedge. In practice, biotech performance over the period was driven less by fundamentals and more by macro flows, sentiment shifts, and risk-on/risk-off positioning. Broad biotech beta moved in ways that overwhelmed relative dispersion, blunting the intended offset and compressing spreads.

In short, the selection was largely right, but the pairing failed in a regime where capital flows mattered more than cash flows. This was a reminder that even well-founded relative frameworks can struggle when sector-wide sentiment dominates fundamentals.

4. A Payments Trifecta -47.3%

This idea centered on high-quality payments infrastructure businesses with strong moats, recurring revenue, and durable compounding characteristics across processing, point-of-sale hardware, and cross-border rails. Fundamentally, the businesses continued to execute.

The primary issue was valuation, not quality. These companies entered the period priced for near-perfection, leaving little margin for error as rates stayed higher for longer and investors rotated away from premium compounders. Even solid execution failed to offset multiple compression.

In hindsight, the key lesson was clear: great businesses can still be poor ideas if paid for at the wrong price. This was not a breakdown in fundamentals, but a reminder that quality does not immunize against valuation gravity.

5. TRUECALLER AB-B -72.2%

This idea was based on Truecaller’s unusually strong engagement (utility-level DAU/MAU), improving mix toward recurring revenue (subscriptions + business), and a belief that a negative earnings reaction was more optics than fundamentals.

What went wrong was not that engagement disappeared, it was that the stock proved far more sensitive to non-fundamental overhangs than expected:

Reporting optics and incentive-cost noise mattered more than anticipated. Even if economically non-cash, share-price-linked compensation and GAAP volatility created persistent confusion and kept investor confidence fragile.

Macro/FX sensitivity hit perception. With meaningful exposure to India/MENA/Africa and SEK reporting, currency and risk sentiment became a bigger headwind than the thesis underweighted.

“Quality” wasn’t enough without a clear near-term re-rating catalyst. The business continued to evolve, but the market didn’t reward the transition fast enough, and multiple compression did the rest.

Biggest Fades

This section captures a different kind of miss. These were not ideas that failed on analysis or fundamentals, but opportunities observed repeatedly without acting on them. In many cases, the thesis was clear and the setup unfolded as expected, but conviction lagged execution.

In hindsight, these tend to be more painful than ideas that didn’t work, because the cost is invisible: no loss, just foregone participation.

They are included here not as self-criticism, but as a reminder that restraint has a price, and that process risk includes when not to act as much as when to step in.

Presented without commentary. Consider what might have been…

The Recession Food Pair Trade (DLTR / SG):

Long/Short Behavioral Health (TALK/ACHC):

Long/Short GLP1 Related Procedures (ESTA + AIRS) / (INSP + TFX):

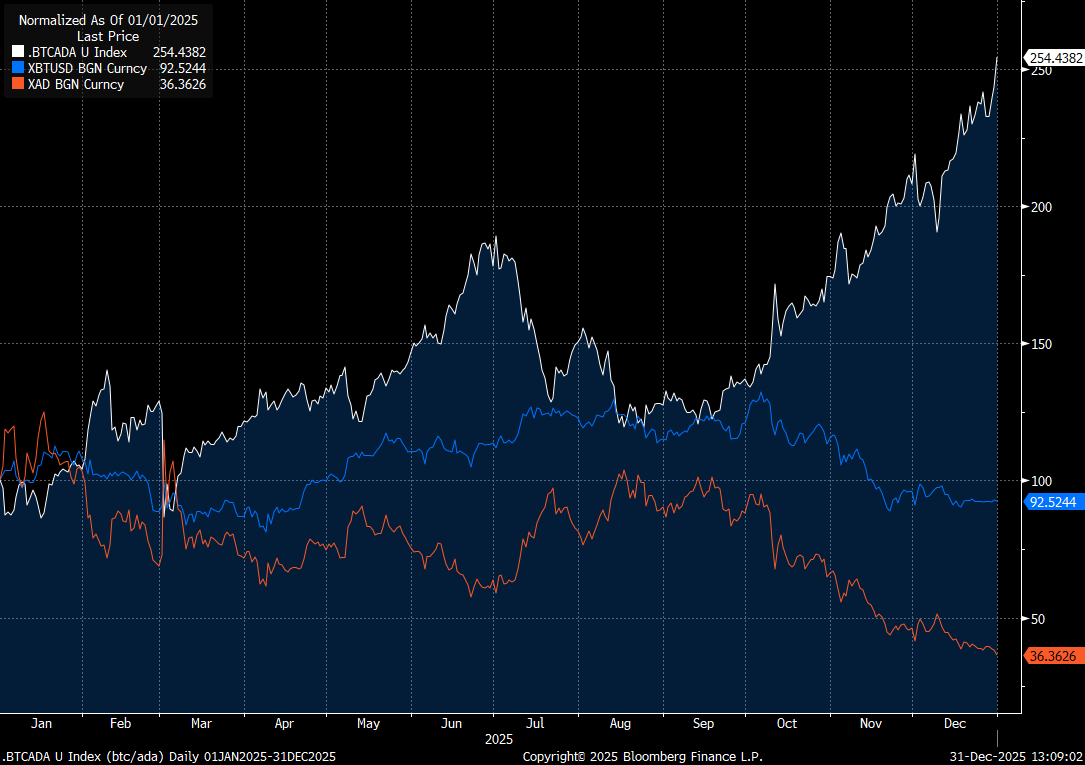

Long Bitcoin / Short Cardano:

Long/Short Freelance (UPWK / FVRR):

What This Year Reinforced

Structure and timing are as important as thesis quality.

Narrative persistence can overpower valuation for longer than expected.

Long/short frameworks tend to be most effective in policy-driven, volatile regimes.

Publishing losing ideas publicly is essential to maintaining a disciplined research process.

Thank you for reading, for thinking alongside me this year, and for sticking with the process. Wishing you all a healthy, focused, and rewarding 2026.

Disclaimer:

This publication is for educational and informational purposes only. Any performance referenced is illustrative and tracked on a per-article basis, not as part of a model portfolio or investment program. Nothing herein constitutes investment advice, a recommendation, or a solicitation. → Ridire Research Substack Disclaimer