Silicon, Software & Settlement: A Payments Trifecta

Own the hardware, middleware, and cross-border tailwind driving the next trillion digital transactions.

Model Portfolio Allocation

Fiserv (FI) – 2.0% weight

Pax Global (327 HK) – 1.0%

dLocal (DLO) – 0.5%

Company Overview – “End-to-End Transaction Stack”

Platform at Scale (Fiserv). The world’s largest merchant processor pairs acquiring, issuer processing and core banking assets under one roof. Merchant margins run 39% and Financial Solutions 52% thanks to high recurring processing revenue and heavy operating leverage. Management highlights 39 consecutive years of double-digit EPS growth and calls the model “high recurring, strong incremental margin, and healthy free cash flow.”

Device Layer (Pax Global). Shenzhen-based Pax ships Android smart POS terminals to >100 countries and monetises post-sale software via its MAXSTORE marketplace. FY-24 gross margin hit 47% on disciplined BOM control and a weaker RMB. Over 11 million live terminals are connected to MAXSTORE, generating >HK$100 m SaaS revenue and meaningfully raising switching costs for acquirers.

Cross-Border EM Rails (dLocal). One-API pay-in / pay-out network operating in 40+ emerging markets. Q1-25 TPV grew +53% YoY to $8.1 bn; revenue rose +18% and net income leapt 163% YoY to $46.7 m with a 27% adjusted EBITDA margin.

Collectively the three names capture the processor, the point-of-sale device and the cross-border settlement leg of a single global payment.

Executive Summary

Core thesis: Volumes and software mix will compound faster than the basket’s blended ~15× forward P/E implies.

What the market misses:

FI’s operating leverage still expands despite scale.

327 HK’s SaaS attach is masking a hardware trough and sits on HK$6bn net cash.

DLO has digested governance noise yet trades at half the multiple of other high-growth networks.

Value unlocks: FI’s FIUSD stablecoin rails, Pax’s MAXSTORE attach, and DLO’s license expansion all offer near-term catalysts.

Compelling Positives

1 | Fiserv ($FI) – scale-plus-software flywheel

Operating leverage still climbing.

“Adjusted operating margin rose 170 bps to 39.4% while organic revenue grew 16%” proof that even at $19 bn run-rate revenue, incremental margins are expanding.Unified omnichannel wins.

“We added large enterprise clients … on the strength of our unified offering, modern gateway and growing value-added solutions” (CEO) indicates that the First Data + Clover stack is resonating with top-tier merchants.Clover still in hyper-growth. Management highlights four value-add products adopted per Commerce-Hub client after one year, raising ARPU and stickiness.

2 | Pax Global ($327 HK) – margin power hiding in “hardware”

MAXSTORE turning devices into SaaS annuities. “>11 million devices connected to MAXSTORE; SaaS revenue topped HK$100m”. This converts a one-off terminal sale into recurring, higher-multiple revenue.

CEO signals ecosystem focus. Jack Lu: “We will strengthen the MAXSTORE ecosystem to maximise Android solutions”. Growing app attach elevates switching costs and future pricing power.

3 | dLocal ($DLO US)– EM rails back on track

Volume and profit re-accelerate. Q1-25 TPV $8.1 bn (+53 % YoY); net income $46.7 m (+163 % YoY); adj. EBITDA margin 27% best quarter since IPO.

Licence moat widening. “In 2024 we added nine licences, incl. UK FCA API” increasing regulatory barriers for new entrants.

Cross-border mix tilt. Cross-border TPV +76 % YoY, now 53% of total, higher-growth corridor with lower competitive saturation than local-only processors.

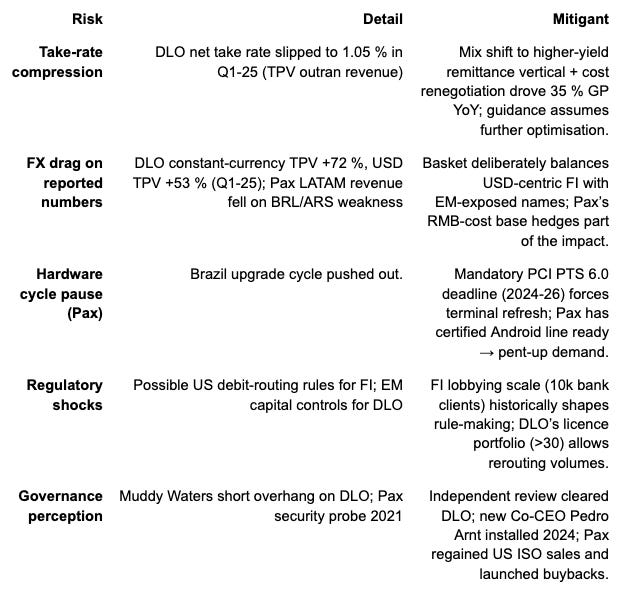

Key Risks & Mitigants

Competitive Advantages

Fiserv

Deep integration moat. Only processor operating at scale in both merchant and issuer tech; over 10k financial-institution clients and 6m merchants. High switching costs (core banking conversions take 2–3 yrs) reinforce 99% client retention.

Pax Global

Cost + ecosystem edge. Shenzhen R&D and in-house firmware cut BOM; Android first-mover gave Pax >50 % of shipments on smart devices. 11 m+ connected terminals provide a distribution network for 14k apps, difficult for Verifone/Ingenico to replicate quickly.

dLocal

Regulatory and network moat. One API covers 40+ EMs and 900+ local payment methods. Nine new licences in 2024 include UK FCA API and UAE Central Bank PSP, raising the compliance barrier while improving unit economics through direct settlement rails.

Competitive Landscape

Processors. FI’s 39% segment margin and 16× fwd P/E compare with Global Payments at 3% and 13×; FIS merchant spin at 11×; Adyen at 38× on 55% margin. Investors pay for pure growth or pure value; FI offers both mid-teens growth and cash yield.

Hardware. Pax at 8× TTM earnings vs. Verifone (taken private at ~15×) and Worldline’s Terminals unit (spun at 12× EV/EBITDA). Pax couples low multiple with SaaS optionality others lack.

Cross-border. DLO’s 27% EBITDA margin dwarfs EBANX (private, est. sub-10 %) and PayU LatAm (Naspers), while its licence footprint now matches PayU India. Adyen and Stripe compete only in ~15 of DLO’s 40 markets, mostly tier-one EMs.

Bottom Line

This Payments Infrastructure Basket captures the full journey of a transaction:

Fiserv records and settles it with high-retention software.

Pax Global supplies the smart device that initiates it.

dLocal moves the funds seamlessly across borders.

Each layer carries its own moat, currency mix, and growth engine. Blended, we own mid-teens EPS compounding with upside from:

FI’s stablecoin rails and Clover SaaS share gains,

Pax’s PCI-driven refresh cycle plus MAXSTORE attach,

dLocal’s licence-led expansion into Africa, GCC, and SE Asia.

Current valuation still prices the group closer to legacy processors than high-conviction infrastructure. Execution on the above catalysts can unlock multiple expansion and deliver an attractive risk-adjusted return without concentration in any single geography or revenue model.

Disclaimer:

Ridire Research is an independent research publication operated by Ridire Research LLC and affiliated with a private fund, an Exempt Reporting Adviser under the U.S. Investment Advisers Act of 1940. Ridire Research is not registered as an investment adviser and does not provide personalized investment, legal, accounting, or tax advice.Informational & Educational Purpose Only

All materials—including text, charts, model portfolios, and explicit labels such as “Buy,” “Sell,” “Hold,” “Long,” or “Short”—are published solely for general informational and educational purposes. They reflect the author’s views at the time of writing, derived from publicly available data, proprietary frameworks, and market analysis, and are not tailored to any reader’s specific objectives, financial situation, or risk tolerance. Subscription to this Substack does not create an adviser–client relationship with the affiliated private fund or its principals.

No Offer or Solicitation

Nothing herein constitutes (i) an offer to sell or the solicitation of an offer to buy any security or other instrument, (ii) a recommendation to participate in any investment strategy, or (iii) a solicitation for investment advisory services. Any references to trades, allocations, or vehicles should be viewed as hypothetical model illustrations only. Offers, if ever made, will be made solely by confidential offering documents and only to qualified investors in jurisdictions where permitted.

Potential Conflicts of Interest

The affiliated private fund, its affiliates, employees, and related accounts may hold, increase, decrease, initiate, or exit positions, long or short, in securities or digital assets discussed, without notice or obligation to update disclosures. Such positions may be inconsistent with views expressed in this publication. The affiliated private fund, related entities, and personnel may initiate, modify, or exit positions in any mentioned security before or after publication without further notice. We maintain internal policies, including trading blackout windows and conflict reviews, to mitigate potential conflicts of interest.

Accuracy & Forward-Looking Statements

Although we strive for accuracy and analytical rigor, information may become outdated and may contain errors or omissions. Forward-looking statements, projections, or target prices are inherently uncertain and may differ materially from actual results. No warranty, express or implied, is given as to completeness, accuracy, or reliability.

Risk Acknowledgment

Investing involves substantial risk, including the potential for complete loss of capital. Past performance, whether actual, indicated by back-tests, or modeled, is not indicative of future results. Securities, derivatives, and digital assets mentioned may be illiquid, highly volatile, or subject to regulatory change.

Reader Responsibility

Readers should conduct their own due diligence, consider their personal circumstances, and consult a licensed financial professional before acting on any information contained herein. By reading this publication you agree that Ridire Research LLC, the affiliated private fund, and their affiliates accept no liability for any direct or consequential loss arising from reliance on the information presented. This research is not directed at persons in jurisdictions where such distribution would be contrary to local law.