The 3Bs of Sovereignty

Bullets, Bars & Bitcoin in an Age of Fracture

Sovereignty means owning what no one can freeze, print, or invade. In a world tilting toward surveillance, inflation, and conflict, few assets truly safeguard autonomy: Bullets, Bars, and Bitcoin. Each offers a distinct layer of independence: physical, financial, and digital. Defense stocks benefit from geopolitical instability and national rearmament. Gold has endured millennia of monetary collapse. Bitcoin offers an exit from fiat debasement and centralized control. Together, they anchor a hard-asset portfolio designed not just to perform, but to persist.

Strategic Allocation: A Sovereign Portfolio

Our positioning reflects long-term structural shifts in capital, trust, and power:

Bullets (Defense): A custom basket of equities spanning aerospace primes, dual-use tech, and military infrastructure.

Bars (Gold): GLD for liquidity and institutional flows; GDXJ for leveraged upside via junior miners.

Bitcoin: IBIT for scalable spot exposure; CLSK for high-efficiency, energy-levered Bitcoin mining.

Bullets: The Defense Basket

If sovereignty has a backbone, it's built on control of force. Defense equities offer exposure to an industry that thrives not despite geopolitical instability, but because of it. The global rearmament cycle is now undeniable, with NATO countries boosting budgets, Asia-Pacific tensions rising, and sovereigns refocusing on industrial capacity and defense autonomy.

Our basket reflects high-quality exposure across aerospace primes, dual-use technologies, and mission-critical suppliers. This is not a momentum trade, it’s a structural allocation to defense as a long-duration theme.

This portfolio emphasizes supply chain control, modularity, and sovereign procurement sensitivity. The goal is not to chase wartime spikes, but to own enduring franchises with high-margin, defensible niches in an increasingly kinetic world.

Bars: GLD (Gold ETF)

Gold isn’t a bet on collapse, it’s a hedge against consensus error. Central banks are buying gold at the fastest pace since WWII. The freezing of sovereign FX reserves (e.g., Russia, 2022) has reasserted gold’s role as a neutral reserve asset.

GLD provides:

Liquidity: Among the world’s most liquid ETFs, enabling institutional-scale allocation.

Sovereign Tracking: Reflects global reserve diversification flows away from USD and Treasuries.

Crisis Resilience: Performs well during stagflation, liquidity stress, and when real yields peak.

Bars: GDXJ (Junior Miners)

Junior gold miners represent a unique investment opportunity due to their pronounced operational leverage to gold price movements. Unlike major miners, juniors operate with thinner margins, which amplifies both risks and rewards as gold prices fluctuate. When gold prices rise, the net present values (NPVs) of their projects increase disproportionately, and their valuation multiples begin to converge with those of the majors, offering multiple layers of leverage. Historically, gold mining companies have demonstrated resilience during economic downturns. During the Great Depression, the SP Gold Index advanced roughly eightfold from 1929 to 1937.

Why Now?

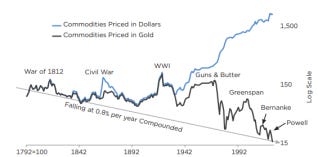

Macro Environment Favoring Gold: Contrary to mainstream economic predictions, high interest rates have driven gold prices higher instead of lower. This is primarily due to a shift in global capital flows and concerns over U.S. monetary policy. High interest rates led to higher gold prices (not lower, as bank analysts predicted); and commodities fell in terms of gold to a new 212-year low, which should lead to higher real margins for gold mining over time.

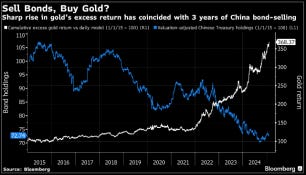

Global Capital Reallocation: The freezing of Russian dollar reserves in 2022 marked a turning point in international trust in U.S. dollar assets. This has led to increased international demand for gold over U.S. Treasury bonds. The voracious demand for gold is coming not from domestic sources but from international buyers who have begun to prefer the marginal gold ounce to the marginal treasury bond.

Liquidity Reversal: The U.S. Federal Reserve's tightening monetary policies, alongside the Treasury's unsustainable short-term financing strategy, are poised to create a liquidity crunch. The main sources of liquidity are going into reverse: long rates will rise due to federal financing needs, the money supply will shrink because there is no more ability for the Treasury to undo Powell’s balance sheet runoff. Custom liquidity index shows we are still stuck in the post pandemic regime:

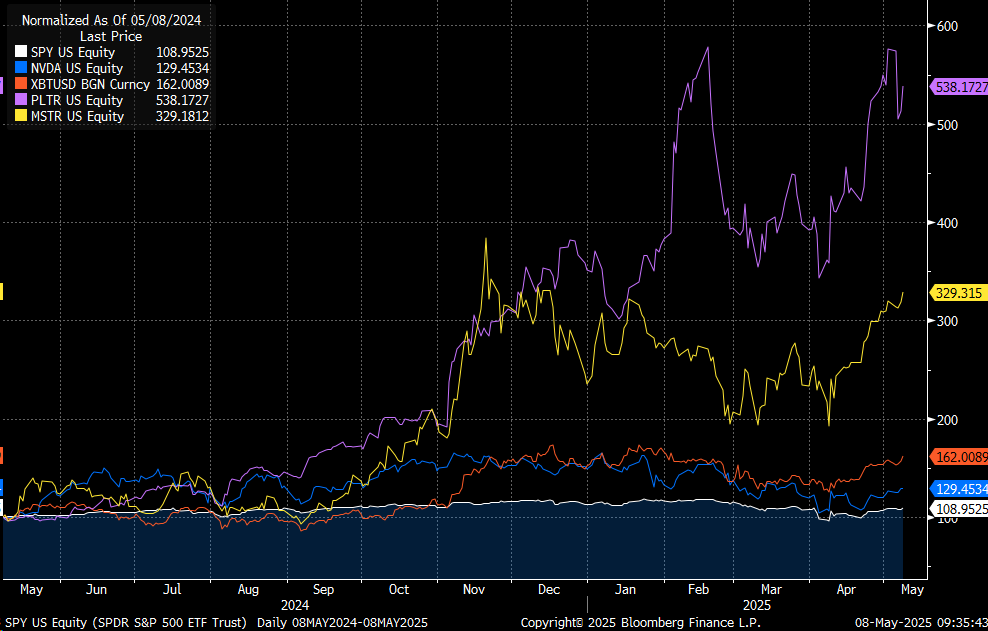

Bubble Exhaustion: The extreme overvaluation in equities and speculative assets like cryptocurrencies is unsustainable. When these bubbles burst, capital will seek safer havens, including gold and, by extension, junior gold miners will benefit. The S&P 500 increased 25% in 2024... investors could have more than doubled their 2024 return if they had instead loaded up on bitcoin, which jumped 164% during the year, if that was not enough then MSTR +500%, then fartcoin +trillion%.

Compelling Reasons to Own GDXJ:

Operational Leverage: Junior miners' thin margins mean that any increase in gold prices significantly boosts profitability. When the gold price increases, the net present values of their projects rise the fastest, applying multiple leverage on top of operational leverage.

Undervaluation Relative to Gold Prices: Despite rising gold prices, junior miners have lagged due to capital being diverted into bubble trades. This creates an attractive entry point for investors.

Resilience in Economic Downturns: Historically, gold miners have performed best during economic busts. As the current bubbles in tech and cryptocurrencies deflate, junior miners are poised to benefit from the flight to safety.

Risks to Monitor:

Access to Capital: Junior miners often struggle to secure financing, especially when investor focus is elsewhere. Access to capital is often tenuous and expensive; when money comes rushing suddenly into the sector, there are no ETFs funneling money into their stocks, making them lag sharp moves.

Market Sentiment Toward Risk Assets: The current euphoria surrounding speculative assets like Bitcoin and niche cryptocurrencies can delay capital flows into junior miners.

Geopolitical Volatility: The evolving geopolitical landscape, including U.S. fiscal policies and international trust in the dollar, introduces uncertainty.

Bitcoin: IBIT (iShares Bitcoin Trust)

Bitcoin has always been about optionality: a hedge on monetary failure, capital controls, and censorship. In 2024, it crossed the institutional threshold. BlackRock’s IBIT now offers scalable, regulated spot BTC exposure.

Why IBIT?

Flow Magnet: BlackRock is onboarding long-term capital via RIAs and institutional platforms.

Operational Ease: IBIT eliminates wallet friction, custody risk, and tracking inefficiencies.

Symbolic Legitimization: The SEC’s ETF approval marked a broader acceptance, Bitcoin is infrastructure.

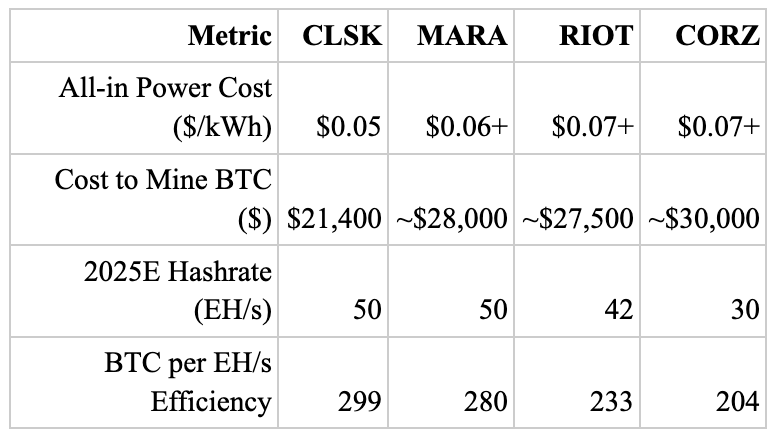

Bitcoin: CleanSpark (CLSK)

CleanSpark is the lowest-cost Bitcoin miner in the industry, with an all-in power cost of just $0.046/kWh and a cost to mine Bitcoin at $21,400 per BTC, substantially below peers such as Marathon (MARA) at ~$28K and Riot (RIOT) at ~$27.5K. With a rapidly expanding hashrate (33.5 EH/s today, targeting 50 EH/s by 2025), a large BTC treasury (~10,000 BTC), and long-duration energy contracts across multiple deregulated markets, CLSK is more than a mining play, it is a strategic asset for institutional buyers and hyperscalers.

Key Catalysts:

Lowest Industry Cost Structure: CLSK’s unit economics remain profitable even at sub-$25K BTC.

Strategic Energy Contracts: Locked-in wholesale power rates position CLSK as a top candidate for M&A by hyperscalers or AI compute buyers.

BTC Treasury & Expansion: $1B+ in Bitcoin and 726MW of operational capacity, growing toward 1GW by 2025.

M&A Potential: Amazon, Google, Nvidia, and others need energy arbitrage and low-cost sites, CLSK already owns them.

AI Transition Readiness: Bitcoin miners are evolving into energy infrastructure providers. CLSK's modular power-dense sites are easily repurposed for GPU clusters and data center buildouts.

Comparative Advantage:

A Prime Acquisition Target for Hyperscalers & AI Infrastructure, Why CLSK Could Be Acquired:

1. Strategic U.S. Energy Contracts: CLSK has 726MW of operational capacity, with a 1GW+ target in 2025.

o Hyperscalers like Amazon (AWS), Google (GCP), and Microsoft Azure need low-cost, renewable power for AI data centers.

o CLSK’s locked-in power rates are significantly below market averages, making it an attractive acquisition target for firms looking to hedge against rising electricity costs.

o AI training requires massive GPU clusters, which are constrained by high energy costs and grid instability, two issues CLSK has already solved.

2. Bitcoin Miners are Becoming Energy Infrastructure Providers:

o Large-scale AI data centers need excess grid capacity and energy arbitrage, which Bitcoin miners specialize in.

o CLSK’s low-cost power + modular site designs make it easy to transition into AI compute.

3. Institutional M&A Wave Incoming:

o Previous M&A: Block (SQ) acquired TBD for Bitcoin infrastructure; Core Scientific (CORZ) emerged from bankruptcy with hyperscaler backing.

o Potential Bidders for CLSK:

▪ AI infrastructure providers: Nvidia, Microsoft, Amazon Web Services (AWS)

▪ Energy-focused firms: Exelon, NextEra Energy

▪ Institutional crypto players: BlackRock, Fidelity Digital Assets

Bitcoin Cycle Tailwinds:

ETF Inflows: Spot ETF approvals drive institutional capital into BTC, supporting mining economics.

Halving Supply Shock (2024): Reduced block rewards benefit cost-leaders like CLSK.

Regulatory Legitimacy: As U.S. policy normalizes around BTC, CLSK’s U.S.-based operations gain further strategic value.

Risks and Mitigations:

BTC Price Decline: CLSK remains profitable down to $25K.

Energy Market Volatility: Offset by multi-year locked-in contracts.

Rising Mining Difficulty: Mitigated via secured next-gen ASICs.

Portfolio Recap: The Sovereign Allocation

To reflect our updated conviction in sovereignty-aligned assets, we are adding the following positions to the model portfolio with their respective weightings:

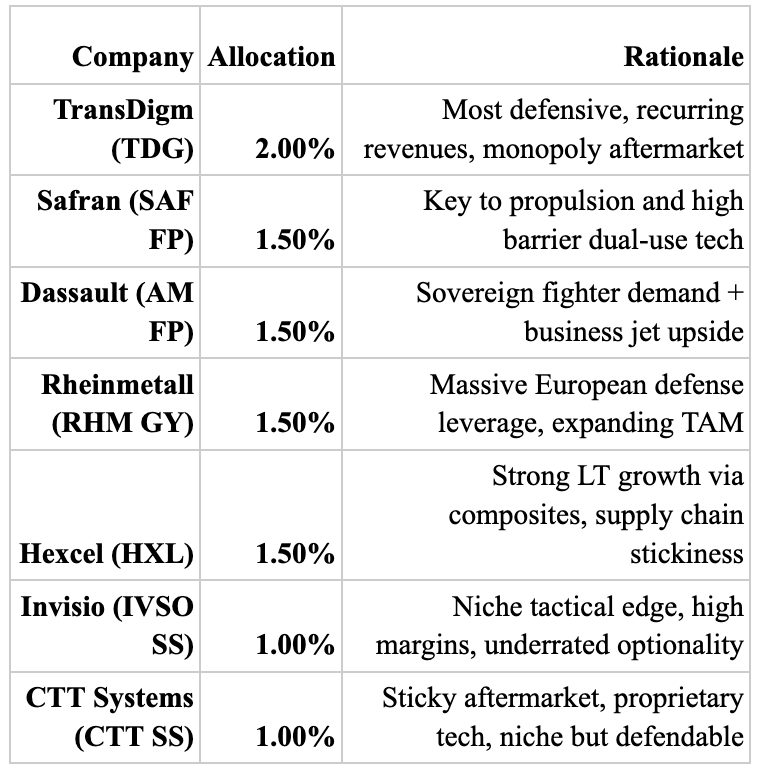

Bullets (Defense Basket): 10.0% Total Allocation

TransDigm (TDG): 2.0%

Safran (SAF): 1.5%

Dassault (AM): 1.5%

Rheinmetall (RHM): 1.5%

Hexcel (HXL): 1.5%

Invisio (IVSO): 1.0%

CTT Systems (CTT): 1.0%

Bars (Gold): 7.0% Total Allocation

GLD: 5.0%

GDXJ: 2.0%

Bitcoin: 3.0% Total Allocation

IBIT: 2.0%

CLSK: 1.0%

This 20% thematic sleeve sits alongside our core model portfolio and is structured to capture asymmetric upside in regimes defined by monetary debasement, geopolitical fracture, and rising demand for digital and industrial sovereignty.

These positions are part of our illustrative model portfolio and is presented for informational purposes only. It does not constitute personalized investment advice.

Disclaimer:

Ridire Research is an independent research publication operated by Ridire Research LLC and affiliated with a private fund, an Exempt Reporting Adviser under the U.S. Investment Advisers Act of 1940. Ridire Research is not registered as an investment adviser and does not provide personalized investment, legal, accounting, or tax advice.

Informational & Educational Purpose Only

All materials—including text, charts, model portfolios, and explicit labels such as “Buy,” “Sell,” “Hold,” “Long,” or “Short”—are published solely for general informational and educational purposes. They reflect the author’s views at the time of writing, derived from publicly available data, proprietary frameworks, and market analysis, and are not tailored to any reader’s specific objectives, financial situation, or risk tolerance. Subscription to this Substack does not create an adviser–client relationship with the affiliated private fund or its principals.

No Offer or Solicitation

Nothing herein constitutes (i) an offer to sell or the solicitation of an offer to buy any security or other instrument, (ii) a recommendation to participate in any investment strategy, or (iii) a solicitation for investment advisory services. Any references to trades, allocations, or vehicles should be viewed as hypothetical model illustrations only. Offers, if ever made, will be made solely by confidential offering documents and only to qualified investors in jurisdictions where permitted.

Potential Conflicts of Interest

The affiliated private fund, its affiliates, employees, and related accounts may hold, increase, decrease, initiate, or exit positions, long or short, in securities or digital assets discussed, without notice or obligation to update disclosures. Such positions may be inconsistent with views expressed in this publication. The affiliated private fund, related entities, and personnel may initiate, modify, or exit positions in any mentioned security before or after publication without further notice. We maintain internal policies, including trading blackout windows and conflict reviews, to mitigate potential conflicts of interest.

Accuracy & Forward-Looking Statements

Although we strive for accuracy and analytical rigor, information may become outdated and may contain errors or omissions. Forward-looking statements, projections, or target prices are inherently uncertain and may differ materially from actual results. No warranty, express or implied, is given as to completeness, accuracy, or reliability.

Risk Acknowledgment

Investing involves substantial risk, including the potential for complete loss of capital. Past performance, whether actual, indicated by back-tests, or modeled, is not indicative of future results. Securities, derivatives, and digital assets mentioned may be illiquid, highly volatile, or subject to regulatory change.

Reader Responsibility

Readers should conduct their own due diligence, consider their personal circumstances, and consult a licensed financial professional before acting on any information contained herein. By reading this publication you agree that Ridire Research LLC, the affiliated private fund, and their affiliates accept no liability for any direct or consequential loss arising from reliance on the information presented. This research is not directed at persons in jurisdictions where such distribution would be contrary to local law.