The Aviation Aftermarket Flywheel

Why an aging fleet and a regulatory clock could quietly transform AerSale.

Affiliation Disclosure & Disclaimer:

The managing principal of Ridire Research is affiliated with a private investment fund that holds long positions in the securities discussed herein (AerSale Corp, ASLE), which could influence the views expressed. This publication is for educational and informational purposes only. Any performance referenced is illustrative and tracked on a per-article basis, not as part of a model portfolio or investment program. Nothing herein constitutes investment advice, a recommendation, or a solicitation. → Ridire Research Substack Disclaimer

Table of Contents

Executive Summary

Company Overview

The Setup

Causal Mechanism

Timeline

Key Risks

Conclusion

Executive Summary

AerSale (ASLE) is in the middle of a business-quality transition: from a volatile “asset trader” (whole aircraft/engine sales) toward a more recurring, higher-margin aviation aftermarket platform where TechOps (MRO + proprietary engineered solutions) becomes the primary earnings driver. The inflection is already visible in reported results: in Q3’25, the company delivered no aircraft or engine sales yet still expanded profitability, with management explicitly citing TechOps margin expansion from 13.6% (Q3’24) to 25.3% (Q3’25) as the segment mix and work scope shifted toward higher-margin opportunities.

The near-to-medium term forcing function is AerSafe, a proprietary, FAA-STC-backed engineered solution tied to an FAA compliance deadline in Q4 2026. As aircraft rotate through maintenance windows, AerSafe deliveries are positioned to remain elevated into 2026.

Simultaneously, AerSale is coming off a multi-year facilities buildout: management states construction is complete on expansion projects and guided (on the Q3’25 call) to ~$25M of revenue and ~$4–5M of EBITDA contribution in 2026 from the three expansion projects as they ramp into production.

What must be proven for the thesis to compound:

TechOps margins remain structurally higher even when whole-asset sales are muted .

Engineered solutions scale without pulling forward all demand into a single “deadline quarter”.

The company converts its substantial inventory base into cash flow as the model becomes more capital-light.

Company Overview

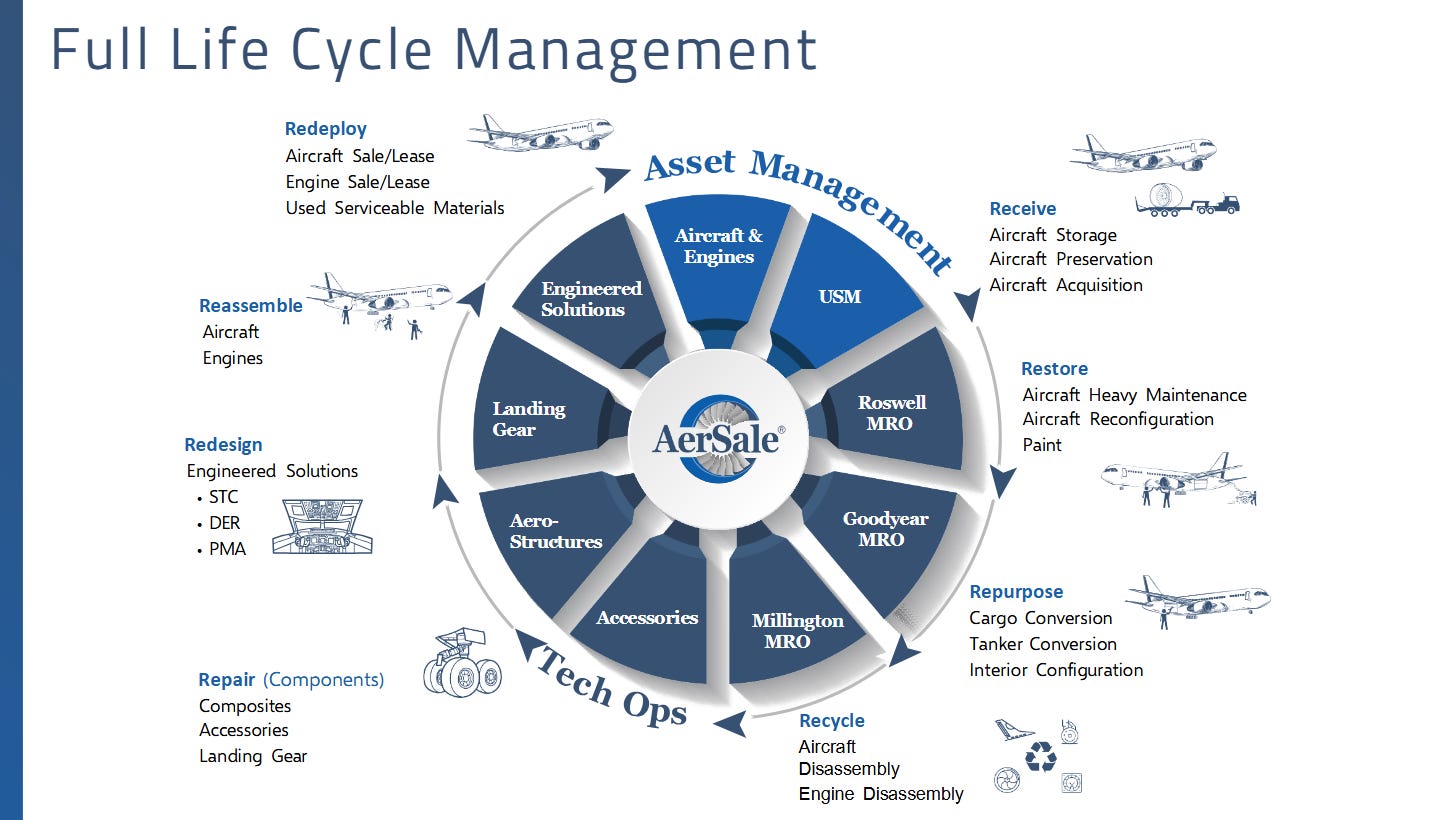

AerSale is an integrated aviation aftermarket provider organized into two reportable segments:

Asset Management Solutions: acquires flight equipment and monetizes it through leasing, trading, or disassembly into used serviceable material (USM).

TechOps: provides MRO (aircraft/component maintenance, landing gear, thrust reversers, aerostructures, modifications/cargo conversions, storage) and sells internally developed engineered solutions permitted by FAA Supplemental Type Certificates (STCs) (proprietary, non-OEM solutions to airworthiness directives/technical challenges).

In Q3’25, AerSale reported total revenue of $71.2M, split between $39.2M Asset Management Solutions and $32.0M TechOps. The quarter also highlighted the company’s deliberate pivot away from pure trading volatility: no aircraft or engines were sold in Q3’25, versus five engines in the prior-year quarter.

The Setup

“Quality of revenue” is improving even as headline revenue remains volatile.

While reported revenue can fluctuate with the timing of aircraft and engine transactions, the company’s recurring businesses, USM parts, leasing, MRO services, and proprietary engineered solutions, are becoming a larger share of activity, supporting a more stable earnings profile over time.

TechOps is the margin inflection point, already happening.

Management attributed the step-change in TechOps profitability to refocusing MRO facilities on higher-margin work and to engineered solutions volume/mix. Operationally, Roswell has been repositioned toward teardown/decommissioning work (higher-margin scope), while other shops (aerostructures/landing gear) and AerSafe helped offset softer services at certain facilities.

Capacity expansion is shifting from “build” to “harvest.”

Management stated construction is complete on expansion projects and the company is transitioning into operations. Separately, AerSale opened a new ~90,000 sq ft aerostructures MRO facility in Hialeah Gardens, FL, described as ~3× larger than the prior location, with upgraded equipment supporting larger widebody structures (B777 nacelles/thrust reversers, GE90/Trent platforms).

Capital allocation has already cleared the private equity overhang.

In March 2025, AerSale repurchased ~6.4 million shares at $7.00 per share (~$45M) from its former sponsor, Leonard Green & Partners, and immediately retired them. The transaction effectively completed the sponsor’s exit and removed a recurring technical headwind that often weighs on asset-heavy businesses with private equity ownership. While not an operational catalyst, the removal of a large financial sponsor reduces potential share supply and clarifies the company’s transition into a fully public shareholder base.

Causal Mechanism

The thesis is a stacked mechanism where multiple moving parts reinforce each other:

Mechanism A: Regulatory-driven engineered solutions + maintenance cycles → accelerating high-margin TechOps mix.

AerSale stated it saw a strong increase in AerSafe deliveries YoY and expects volume to remain elevated through 2026 as the company approaches an FAA airworthiness directive compliance deadline (satisfied by AerSafe installation). At quarter-end, management disclosed that 2025 AerSafe deliveries + backlog totaled >$22M. Management also stated AerSafe should support results through the regulatory compliance deadline in Q4 2026.

Because engineered solutions are proprietary products sold under FAA STCs, the incremental margin profile is structurally better than labor-heavy commodity MRO (and requires meaningfully less incremental capex once certification and tooling are in place).

Mechanism B: “Build is done” facilities expansion → capacity + capability unlock in 2026.

In Q&A, management quantified the expansion projects: ~$25M of revenue and ~$4–5M of EBITDA in 2026, stepping toward a higher run-rate at full capacity.

This contribution is powerful because it is incremental to the pre-expansion base and intended to be more recurring than whole-asset sales, reducing consolidated earnings volatility.

Mechanism C: Leasing + USM monetization → smoother revenue and better operating leverage.

The company is explicitly shifting its deployment strategy toward assets on lease to create more stable quarter-to-quarter performance (leasing additional converted freighters/engines).

The financial statements show this operationally: AerSale disclosed reclassification of inventory to equipment held for lease (a signal that inventory is being pushed into recurring lease-earning assets rather than one-time sales).

Mechanism D: Capex taper (post-buildout) + working-capital discipline → potential inflection in free cash flow.

Cash-flow disclosures are directionally consistent with capex moderating as major buildouts complete. Management has also framed working-capital optimization as part of building a “more resilient business model,” but the proof will be in reported operating cash flow as inventory turns into USM sales, lease revenue, and TechOps throughput.

Timeline

Near-term: FY2025 results (March 5, 2026).

AerSale announced it will report Q4 and full-year 2025 results on March 5, 2026 (after market close), with a conference call the same day. This is the first opportunity for investors to pressure-test whether Q3’s margin profile persists and whether 2026 ramp commentary holds.

2026: “Harvest year” for expansions + AerSafe pre-deadline acceleration.

Key 2026 checkpoints:

H1 2026: early evidence of expansion project ramp, utilization, and whether TechOps margins remain elevated. (Management’s quantified expectation for 2026 contribution is a direct benchmark.)

H2 2026: engineered solutions should remain strong as operators work through compliance timelines; management has explicitly anchored AerSafe support through Q4 2026.

Post-deadline (2027 setup): durability question.

After the compliance deadline, the debate becomes: is AerSafe predominantly pull-forward (a “one-time compliance wave”) or does it settle into a multi-year annuity-like stream (replacement/maintenance + broader adoption)? The company’s longer-term narrative also depends on whether AerAware converts from “engineering asset” to “commercial product” via a launch order.

Key Risks

Used-serviceable material supply loosens faster than demand.

If OEM delivery rates and retirements normalize faster than expected, USM pricing and demand intensity can soften, pressuring the Asset Management segment and lowering returns on acquired feedstock. This matters because AerSale’s balance sheet is heavily inventory-weighted.

AerSafe “demand cliff” after the Q4’26 compliance deadline.

Management is clear that AerSafe is tied to an FAA compliance window through Q4’26. If demand collapses post-deadline and AerSale does not scale additional engineered solutions, TechOps margins could revert toward historical (lower) levels and the “recurring, high-margin TechOps” narrative weakens.

Whole-asset sales remain structurally lumpy (earnings optics risk).

AerSale repeatedly emphasizes that whole-asset sales drive quarter-to-quarter volatility; Q3’25 is a reminder that reported revenue can swing materially depending on whether aircraft/engine sales occur. Even if the long-term shift toward leasing/TechOps works, near-term results can look noisy.

Working capital / inventory monetization risk.

The company disclosed $371.1M of inventory and cash used in operations year-to-date of $34.3M, reflecting inventory investment. If inventory turns slow (or pricing deteriorates), leverage rises and cash conversion can disappoint.

Conclusion

AerSale’s thesis is best framed as a margin + mix + cash-conversion transition. The company has already demonstrated that profitability can improve even in a quarter with zero whole-asset sales, driven by higher TechOps margins and a pivot toward leasing/USM monetization. The next 12–18 months are about validating durability: AerSafe demand into the Q4’26 compliance deadline, the 2026 ramp of expansion projects (with disclosed revenue/EBITDA expectations), and tangible improvement in operating cash flow as inventory is monetized.

A secondary dimension of the story is AerSale’s position as a sub-scale but integrated platform in a consolidating aviation aftermarket industry. The company combines aircraft and engine feedstock sourcing, USM parts distribution, MRO capabilities, and proprietary engineered solutions, capabilities that are increasingly being assembled into larger platforms by strategic buyers. While not required for the thesis, the company’s integrated capabilities and regulatory certifications create potential strategic value if consolidation in the aerospace aftermarket continues and could potentially be an acquisition target.

Great Stuff! Great Read! Question for you as FTAI and other independent players scale their “module exchange” programs to capture a larger share of the $25 billion CFM56 aftermarket, how do the Original Equipment Manufacturers (OEMs) like GE and Safran typically respond? Is there a risk of the OEMs tightening the supply of life-limited parts (LLPs) to protect their own high-margin service revenue?