The Cost of Downtime

Availability as the hidden driver of value in industrial supply chains.

Table of Contents

1. Investment Thesis

2. Catalysts & Narrative

3. Risks

4. Conclusion

Thesis Summary:

DNOW: The “Made in America” supply-chain utility hiding in plain sight. DNOW is evolving from “oilfield distributor” into a scaled, digitally-enabled industrial supply-chain utility, levered to U.S. re-industrialization, energy security capex, and AI-driven infrastructure buildouts, while the MRC Global combination turns its network density and category breadth into a harder-to-replicate moat.

1. Investment Thesis

Intro: A Primer on The Cost of Downtime

In industrial systems, downtime is not simply an inconvenience, it is a financial event with direct and indirect consequences. Downtime refers to any period in which a machine, facility, or system is unavailable for production. It can be planned (maintenance, turnarounds) or unplanned (equipment failure, logistics breakdowns, human error). The distinction matters operationally, but economically the outcome is the same: lost output at precisely the wrong moment.

Critically, the cost of downtime is not limited to the value of foregone production. It compounds across multiple dimensions:

Idle labor and overtime to recover schedules.

Missed deliveries and contractual penalties.

Safety and regulatory exposure.

Reputational damage with customers.

Cascading disruptions across dependent systems.

In other words, downtime costs are non-linear. Once a system fails, every additional minute becomes more expensive than the last.

Recent research underscores how severe this has become. According to Siemens’ True Cost of Downtime study, unplanned downtime now costs Fortune Global 500 companies roughly 11% of annual revenue, nearly $1.5 trillion globally, up sharply from pre-2020 levels. At the facility level, large industrial plants now lose over $100 million per year on average to downtime. The cost of a single lost hour ranges from tens of thousands of dollars to well over $2 million, depending on industry and criticality. The key takeaway is not the exact figures, but the direction: downtime is becoming more expensive, not less, as industrial systems grow more capital-intensive, more regulated, and less tolerant of failure.

This reality changes procurement behavior. When the cost of failure dwarfs the cost of parts, purchasing decisions shift away from unit price and toward availability, specification accuracy, logistics reliability, and response time. The economic value migrates to whoever can ensure that the right component is in the right place at the exact moment failure becomes intolerable.

Manufacturers increasingly respond by investing in predictive maintenance, inventory buffering, supplier consolidation, and digital monitoring because it is cheaper than being wrong. Siemens’ research shows these strategies can materially reduce unplanned downtime, but they also raise the strategic importance of partners embedded directly in maintenance workflows.

For readers interested in the full data and methodology, Siemens’ True Cost of Downtime report provides a comprehensive breakdown across industries and geographies. Linked HERE

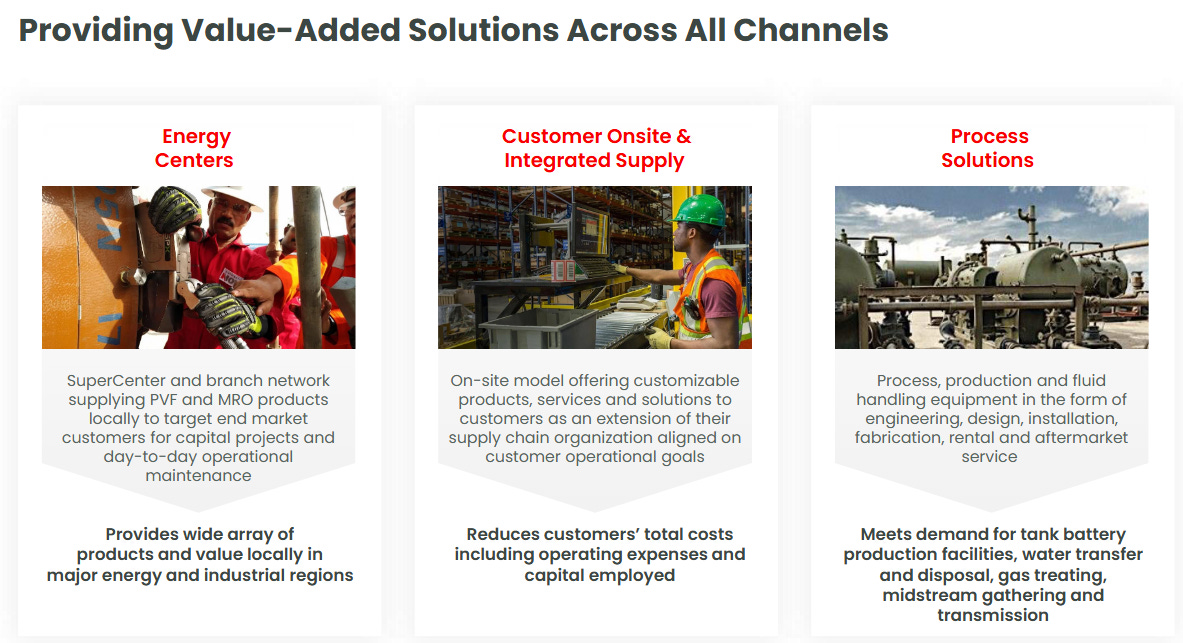

Where Downtime Economics Meet the Physical Supply Chain: DNOW

The correct way to underwrite DNOW is as a monetizer of downtime risk, not as a cyclical oilfield distributor. Across energy, utilities, manufacturing, and infrastructure, the economic penalty of downtime dwarfs the marginal cost of parts. When physical systems fail: pipelines, processing plants, power infrastructure, industrial facilities; the cost is measured in lost output, safety exposure, regulatory risk, and cascading operational disruption. DNOW’s business sits directly at this fault line. What DNOW actually sells is time certainty:

The right part,

in the right specification,

at the right location,

exactly when failure is most expensive.

This is a fundamentally different economic proposition than selling commoditized inputs. In this model, availability, logistics reliability, and workflow integration become the value drivers rather than unit pricing.

In 2025, this model became reinforced by an unusually favorable structural backdrop:

U.S. industrial and manufacturing construction remains historically elevated.

Policy-driven re-industrialization and tariff regimes are increasing supply-chain friction.

Energy and midstream reinvestment is driven by reliability, not growth optimism.

AI and data-center expansion is pulling forward power and infrastructure buildouts.

DNOW benefits from all of these without requiring a bullish view on any single commodity, election outcome, or GDP forecast.

The MRC Global combination materially strengthens the thesis. It expands DNOW’s network density, PVF category depth, purchasing leverage, and customer relevance, pushing the company closer to a supply-chain utility rather than a transactional distributor.

The core premise is simple but underappreciated:

As physical systems become more capital-intensive and less tolerant of failure, the value of being in-stock, on-time, and operationally embedded compounds.

That is the economic engine DNOW is building.

2. Catalysts & Narrative

DNOW’s story works because multiple independent narratives converge on the same operating mechanism: downtime avoidance. These narratives are:

A. Re-industrialization and the permanence of maintenance demand

The current U.S. manufacturing build cycle is not just about new construction. Every plant, terminal, and processing facility commissioned today creates a long tail of maintenance demand that often exceeds the initial build cost over the asset’s life.

DNOW participates in both phases:

Build / commissioning: supplying PVF, flow control, safety equipment, and tooling.

Operate / maintain: recurring MRO, replacement parts, and inventory programs.

The second phase is where the economics compound. Once DNOW is managing inventory, standards, and procurement workflows, it becomes operationally embedded. Switching suppliers becomes a risk decision, not a price decision. This dynamic makes DNOW less dependent on incremental construction starts and more tied to the installed base of physical capital, which is growing.

B. Tariffs, supply-chain friction, and the value of aggregation

The 2025 tariff environment matters less for its politics and more for its operational consequences.

Tariffs and trade friction increase:

Lead-time uncertainty.

Supplier fragmentation.

Inventory risk.

Operators respond by:

Localizing sourcing where possible.

Holding buffer inventory.

Consolidating suppliers to reduce complexity.

These behaviors disproportionately benefit scaled distributors that can aggregate supply, manage inventory across sites, and act as an outsourced procurement function. DNOW’s model becomes more valuable as supply chains grow more complex. This is a critical point: supply-chain friction increases distributor relevance when the distributor solves it.

C. Energy reliability over energy growth

DNOW does not need a new shale boom to work. Energy infrastructure, upstream, midstream, utilities, LNG, power, requires continuous reinvestment simply to remain operational and compliant. Maintenance is not discretionary, and downtime is not tolerated. Even as capital allocation in energy shifts toward electrification and decarbonization, the physical reality remains:

Pipelines still need valves.

Compressors still fail.

Power systems still require redundancy.

Regulatory standards continue to tighten.

DNOW’s exposure is to maintenance intensity. That distinction matters when cycles turn.

D. AI, data centers, and second-order infrastructure demand

AI and data centers do not buy parts from DNOW directly, but they reshape the physical economy underneath them. Data-center expansion pulls forward:

generation capacity

grid upgrades

gas infrastructure

cooling and redundancy systems

All of these are flow-control and MRO-intensive over time. DNOW’s participation is indirect but durable, and it reinforces the broader theme: as society leans harder on physical systems, downtime becomes more expensive.

E. The MRC Global integration as a structural catalyst

The MRC Global acquisition is the most important company-specific catalyst because it changes DNOW’s competitive geometry.

The combination delivers:

materially higher network density

expanded PVF category leadership

improved purchasing leverage

broader customer relevance across energy, utilities, and industrials

This matters for three reasons:

Service reliability improves with scale and inventory depth

Customer consolidation accelerates toward fewer, larger suppliers

Digital procurement leverage increases as workflows standardize

The strategic value is the reinforcement of DNOW’s moat where it actually matters: availability and fulfillment certainty.

3. Risks

Integration execution risk:

The MRC integration must preserve service levels. Any disruption to availability directly undermines DNOW’s value proposition.Energy activity downturns:

DNOW is maintenance-oriented but not immune to sharp volume contractions in energy-related end markets.Policy volatility:

Tariffs and industrial policy can raise costs as well as stimulate domestic investment. DNOW must maintain pricing discipline and execution to benefit net-net.Digital disintermediation risk:

Digital procurement reduces friction, but it also lowers switching costs if DNOW fails to be the preferred platform. The bull case assumes DNOW deepens lock-in, not commoditization.Working-capital mismanagement:

Inventory discipline during integration and demand shifts is critical. Poor execution here would pressure cash generation.

4. Conclusion

DNOW is best understood as industrial uptime infrastructure, not as a commodity distributor or a simple energy proxy.

Its economics are driven by:

The cost of downtime.

The value of availability.

The difficulty of replacing an embedded supply-chain partner.

In a world of heavier physical capital, tighter supply chains, and lower tolerance for failure, those attributes become more valuable. The MRC Global combination materially strengthens DNOW’s position by widening its moat in the areas that matter most: inventory density, category breadth, and procurement integration. This is not a call on oil prices, GDP growth, or political outcomes. It is a call on a durable economic reality:

When downtime is expensive, the distributor who prevents it becomes indispensable.

That is the business DNOW is building.

Disclaimer:

This publication is for educational and informational purposes only. It reflects research opinions and illustrative examples, not investment advice or recommendations. Nothing herein constitutes an offer, solicitation, or advice to buy or sell any security. By reading, you agree to the full disclosures → Ridire Research Substack Disclaimer

Great analysis! I've also been selling cash-secured puts on it to generate income while waiting for a lower entry price. Thanks!

Couldn't this thesis apply to most industrial component suppliers? What makes dnow so unique?