The Dollar’s Next Anchor

The Petrodollar Reimagined for the Computational Era

Before I lose half of you at the headline, let me be clear: this is highly speculative. This is a framework review rather than a call. What follows is the first attempt to map out the ideas circulating around what I’m going to call the “Hash-Energo Dollar.” I’m not advocating it, just outlining the logic and the players behind it. Personally, I’m exposed to both “systems”, the hash/energy-anchored assets and the gold/BRICS complex, and I don’t particularly care which one wins. My base case: it’s slightly better than a coin-flip that some version of this structure quietly takes shape within five to ten years. I’ve heard variations of it whispered for a while now, and it keeps resurfacing. It still sounds ridiculous at first, especially if you can’t get past the “crypto is a scam” reflex, but the plumbing is starting to look real. That being said, let’s dive in.

Table of Contents

The Hash-Energo Dollar Hypothesis

Why This Exists & Campbell’s Asymmetry: The Decoupling Backdrop

Mechanics That Already Work, Mechanics That Could Work

The Pigeon Framework vs. Softwar

Incentive Alignment and the Stablecoin Flywheel

Financial Weaponization: Two Systems, Two Logics

From Geopolitics to Balance Sheets

Trump and Musk: Policy, Optics, and Execution

Implementation Phases

What the Outcome Looks Like

Tracking the Trades: The Two Horses

The Hash-Energo Dollar Hypothesis

Thesis in brief:

Move the dollar’s second anchor from abstract confidence to measurable energy productivity and Bitcoin hashpower.

Pull global crypto liquidity into Treasuries, keep custody and miners on U.S. rails, and let the reserve architecture emerge from the grid.

The objective is straightforward: reinforce dollar primacy while decoupling from China and blunting the optics of a BRICS gold lane.

Why This Exists

Treasuries still sit at the core of the system, but reserve prestige erodes at the margin. Gold lifts our adversaries. China’s banking system is running a structural loss machine: $5-10T in property-related losses against roughly $3T in bank equity, plus something on the order of $1.1T per year to hide the damage. That is called a capacity constraint. The United States needs a second pillar that rests on physics and metered output, rather than narrative alone.

Campbell’s Decoupling 2017-2045 gives the macro backdrop. He outlines how China’s extend-and-pretend property regime bleeds liquidity and traps the PBOC in an impossible trilemma: defend the currency, recapitalize banks, or preserve social stability. Time, demographics, and energy dependence all push in one direction, structural asymmetry that widens each year.

His key insight: after 2027, U.S. rare-earth and energy independence close the loop, leaving Beijing exposed to dollar system chokepoints it cannot replicate.

The Hash-Energo Dollar is what I believe fills that vacuum: the mechanism through which U.S. energy and computation become reserve credibility, while China’s capital base dissolves into hidden losses.

Campbell’s decoupling framework is the backdrop. China faces a trilemma it cannot solve cleanly: defend the currency, recap banks, or preserve social stability. Choose two at best, often one. The leverage window narrows into 2027 to 2030 as U.S. rare-earth independence rises, demographics worsen in China, Taiwan politics move, and leadership succession risk increases. The asymmetry grows with time, so this is the window to shift the plumbing.

Mechanics That Already Work

Bitcoin miners already earn $1b to $2b per year from ERCOT to provide flexible load. They are paid to throttle when the grid needs headroom. In practice, these sites behave like controllable demand that absorbs volatility and helps renewables scale.

Immersion cooling can improve efficiency 20 - 40%.

U.S. miners control on the order of 40% of global hash rate, roughly two hundred exahash per second.

Mechanics that could work:

Tie issuance to verified energy output and proof of work. Start small, 1 - 2 billion of capacity, scale to 10 to-20 as contracts, measurement, and custody mature. Energy-backed instruments could probably print 5 - 10% yields while delivering grid services. Liquidity lives around the clock. Bitcoin trades roughly $200b per day. DeFi flows can reach $500b to $1T by 2030. That outpaces gold’s cash turnover and gives the dollar a continuous settlement rail that moves at market speed.

The Pigeon Framework vs. Softwar

This is where the Pigeon Framework departs from Softwar. Softwar imagined Bitcoin as a digital battlespace, essentially hash as deterrence. Pigeon treats hash as collateral. Instead of militarizing the network, it monetizes it and miners become flexible infrastructure. Under Pigeon logic, the U.S. doesn’t need to dominate global hash to win; it only needs to host enough of it to link computation, grid balance, and dollar liquidity under its legal system.

Softwar’s frame casts Bitcoin as a non-kinetic power system, a new military domain to be contested like cyber or space. The Pigeon view is less theatrical and more useful. Bitcoin is a reserve release valve running on U.S. rails. It extends the dollar’s reach precisely when pure Treasuries lose some reserve shine and gold starts funding rivals. The neutrality of the asset is not the point. Jurisdiction over custody, ETFs, banking access, and miner share is the point. Washington is not fighting Bitcoin, this is clear.

In short, Softwar gives the metaphor while Pigeon gives the plumbing, and Campbell provides the strategic rationale. Together they describe a state that no longer needs to announce standards; it shapes them through infrastructure. Hashpower, custody, and energy policy become instruments of macro strategy, the invisible hand of the state moving through open-source rails.

Incentive Alignment and the Stablecoin Flywheel

Miners monetize downtime, earn curtailment revenue, and upgrade to immersion without praying for bull markets.

Grids get a programmable cushion that makes an 80% renewable target by 2030 more realistic and more stable.

Investors get liquid, yield-bearing exposure to U.S. energy infrastructure.

Treasury gains a scalable collateral channel that does not require a treaty or a new Bretton Woods.

The stablecoin flywheel is the quiet engine:

Credible stablecoins will hold 100% T-Bills.

Tether already sits among the largest Treasury holders. Each on-chain dollar becomes a structural bid for U.S. debt.

Our $30T+ T-Bill pool is the natural sink for global crypto savings. You are not browbeating foreign central banks to buy paper.

Here the feedback loop becomes geopolitical:

Every stablecoin minted with full T-Bill backing is a private-sector extension of U.S. debt monetization.

The same mechanism that critics call “crypto” effectively crowds in global dollar demand.

The United States gets a permanent, algorithmic buyer base that is permissionless in front-end form but sovereign in custody. It is the quiet mirror image of China’s ghost banking loop, except this one earns real yield, in real dollars.

Financial Weaponization: Two Systems, Two Logics

The U.S. model weaponizes liquidity through openness: stablecoins collateralized by Treasuries, miners stabilizing renewables, and energy converted into yield. It turns productive capacity into collateral and keeps global capital tied to U.S. rails.

The BRICS model weaponizes exclusion: gold, commodities, and bilateral settlement meant to bypass the dollar. It’s defensive and finite, stores value but doesn’t scale or compound.

The gap is simple: one system monetizes electrons, the other hoards metal. One exports liquidity, the other traps it. The Hash-Energo Dollar sits in between, anchoring credibility in measurable output.

From Geopolitics to Balance Sheets

BRICS are building a gold lane that is static and finite. The United States is building an energy lane that scales with innovation. One hoards metal. The other monetizes electrons and computation with better custody, law, liquidity, and hardware.

Campbell’s asymmetry maps neatly into this plumbing:

China needs the dollar system, advanced chips, allied markets, and U.S. software.

The United States needs Chinese rare-earth processing for a limited window that closes as domestic projects come online.

The financial hostage logic is simple. China holds roughly 2.5 trillion in U.S. financial assets that can be frozen, inflated away, or bought back with a balance-sheet expansion. U.S. firms in China hold physical assets that are far harder to weaponize at scale.

Immediate decoupling hurts them catastrophically and us temporarily. You do not have to pull the trigger for the deterrent to work. Markets price the option.

Trump and Musk: Policy, Optics, and Execution

Trump’s posture is pro-energy and pro-crypto with a mixed-strategy approach to China. Build domestic hash first, normalize ETFs, keep policy optionality on seizures and strategic reserves, and declare the standard only after the infrastructure exists.

Musk’s view of flexible power offloading is the engineering layer. Miners already behave like virtual batteries next to Powerpacks. They get paid to curtail, they stabilize frequency, they capture waste heat.

The optics are coherent: energy independence, American custody, continuous markets, and a real plan to scale renewables without brownouts.

The historical rhyme is obvious. Nixon moved the dollar from gold to oil to regain maneuvering room. The modern move shifts from oil to energy plus computation to regain credibility without gifting the narrative to gold. Build the infrastructure first. Announce the standard later.

Expect the administration’s messaging to stay ambiguous. Publicly, it’s “energy security” and “innovation.” Privately, it’s a quiet re-anchoring of monetary credibility. The politics play as jobs and grid stability; the macro outcome is a harder dollar without a single policy speech. Musk’s engineering credibility gives it narrative cover: renewables, batteries, flexible load, while Trump’s chaos strategy keeps opponents guessing which part is policy vs bluff.

Implementation Phases

Phase one builds hash capacity near stranded or intermittent generation and hardens ERCOT-style contracts in multiple ISOs.

Phase two tightens the custody perimeter with ETFs, qualified custodians, surveillance-sharing, and clean hygiene around seized reserves.

Phase three tokenizes T-Bills, validates energy output, references hash metrics in issuance, and opens a narrow pilot window of one to two billion that can scale to ten to twenty. The Strategic Bitcoin Reserve at 127,000 BTC is a signaling tool. Used sparingly, it hardens optics without telegraphing a peg.

What the Outcome Looks Like

A dollar with a second anchor. Energy output and proof of work provide reserve credibility. Stablecoin standards create a constant bid for Treasuries. U.S. custody binds global flows to U.S. law. Miners make renewables easier to finance and operate.

China’s extend-and-pretend meets a hard floor. The BRICS gold optic loses altitude because the growth asset is not metal rather it is productive capacity you can meter.

The standard does not need a grand unveiling. It will show up first as capacity auctions, curtailment receipts, ETF flows, tokenized bills that settle in seconds, and grid dashboards that look strangely like monetary dashboards. When the plumbing is built, the announcement writes itself.

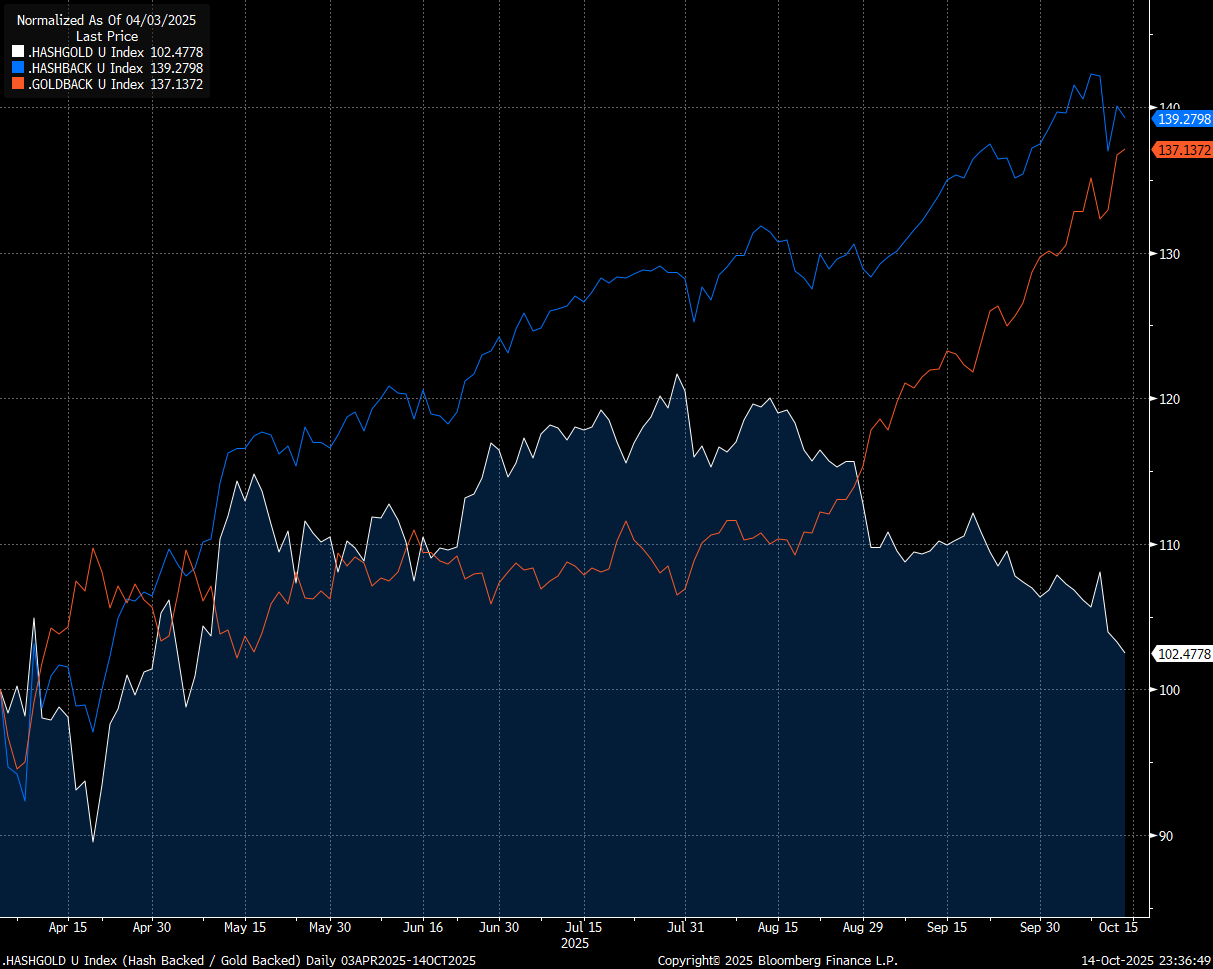

Tracking the Trade: The Two Horses

To track the thesis in real time, I’ve built two equal-weight baskets: two “horses” racing the monetary transition.

HASHBACK: Hash/Energy System → QQQ + IBIT + MNRS

A proxy for the emerging U.S. architecture: tech compute, Bitcoin reserve absorption, and domestic mining infrastructure integrated with the grid.

GOLDBACK: BRICS/Gold System → KWEB + GLD + GDX

A proxy for the alternative bloc: China’s digital and capital-market exposure via KWEB, paired with physical gold and gold miners to represent the static, metal-backed reserve model centered on BRICS and commodity collateral.

Performance since Liberation Day+1 (04/03/2025):

The spread between the two serves as a live decoupling gauge. When HASHBACK outperforms, it implies markets are leaning into the energy-anchored regime, stronger Treasury demand via stablecoins, healthy compute CAPEX, tighter U.S. credit spreads, and confidence in renewable buildout economics. It would theoretically align with a firmer dollar and fading gold beta.

When GOLDBACK leads, it signals rotation toward the BRICS and gold safety complex, capital flight from risk assets, policy or custody stress, rising term premium, or geopolitical pressure that favors tangible stores of value. It would theoretically coincide with softer U.S. liquidity conditions, EM outflows, and widening credit spreads.

Over time, the spread’s direction offers more than a trade, it’s a readout of which monetary operating system the market believes in: the energy-backed, compute-native dollar or the gold-and-commodity collateral bloc.

I’m exposed to both systems. I’m not making a directional bet on which global monetary system wins, I’m positioned to benefit (or at least observe cleanly) either outcome. My goal isn’t to predict, it’s to track which regime the market is migrating toward.

Disclaimer:

Ridire Research is an independent research publication operated by Ridire Research LLC and affiliated with a private fund, an Exempt Reporting Adviser under the U.S. Investment Advisers Act of 1940. Ridire Research is not registered as an investment adviser and does not provide personalized investment, legal, accounting, or tax advice.Informational & Educational Purpose Only

All materials, including text, charts, model portfolios, and explicit labels such as “Buy,” “Sell,” “Hold,” “Long,” or “Short”, are published solely for general informational and educational purposes. They reflect the author’s views at the time of writing, derived from publicly available data, proprietary frameworks, and market analysis, and are not tailored to any reader’s specific objectives, financial situation, or risk tolerance. Subscription to this Substack does not create an adviser–client relationship with the affiliated private fund or its principals.

No Offer or Solicitation

Nothing herein constitutes (i) an offer to sell or the solicitation of an offer to buy any security or other instrument, (ii) a recommendation to participate in any investment strategy, or (iii) a solicitation for investment advisory services. Any references to trades, allocations, or vehicles should be viewed as hypothetical model illustrations only. Offers, if ever made, will be made solely by confidential offering documents and only to qualified investors in jurisdictions where permitted.

Potential Conflicts of Interest

The affiliated private fund, its affiliates, employees, and related accounts may hold, increase, decrease, initiate, or exit positions, long or short, in securities or digital assets discussed, without notice or obligation to update disclosures. Such positions may be inconsistent with views expressed in this publication. The affiliated private fund, related entities, and personnel may initiate, modify, or exit positions in any mentioned security before or after publication without further notice. We maintain internal policies, including trading blackout windows and conflict reviews, to mitigate potential conflicts of interest.

Accuracy & Forward-Looking Statements

Although we strive for accuracy and analytical rigor, information may become outdated and may contain errors or omissions. Forward-looking statements, projections, or target prices are inherently uncertain and may differ materially from actual results. No warranty, express or implied, is given as to completeness, accuracy, or reliability.

Risk Acknowledgment

Investing involves substantial risk, including the potential for complete loss of capital. Past performance, whether actual, indicated by back-tests, or modeled, is not indicative of future results. Securities, derivatives, and digital assets mentioned may be illiquid, highly volatile, or subject to regulatory change.

Reader Responsibility

Readers should conduct their own due diligence, consider their personal circumstances, and consult a licensed financial professional before acting on any information contained herein. By reading this publication you agree that Ridire Research LLC, the affiliated private fund, and their affiliates accept no liability for any direct or consequential loss arising from reliance on the information presented. This research is not directed at persons in jurisdictions where such distribution would be contrary to local law.