The Grid Doesn’t Run on Venture Capital

Natural gas may remain strategically important longer than the market expects.

Affiliation Disclosure & Disclaimer:

The managing principal of Ridire Research is affiliated with a private investment fund that holds long positions in the securities discussed herein (CNX), which could influence the views expressed. This publication is for educational and informational purposes only. Any performance referenced is illustrative and tracked on a per-article basis, not as part of a model portfolio or investment program. Nothing herein constitutes investment advice, a recommendation, or a solicitation. → Ridire Research Substack Disclaimer

Table of Contents

Executive Summary

Company Overview

Casual Mechanism

Key Risks

Conclusion

Executive Summary

This is a shorter piece briefly highlighting a smaller natural gas asset we believe remains overlooked by the market: CNX Resources Corporation is a disciplined Appalachian natural gas asset with long-duration reserves, strong free cash flow generation, and second-order tailwinds from a structurally improving U.S. gas demand backdrop.

The market still tends to value Appalachian gas producers as cyclical commodity equities trapped in oversupplied domestic markets. That assumption is becoming less durable.

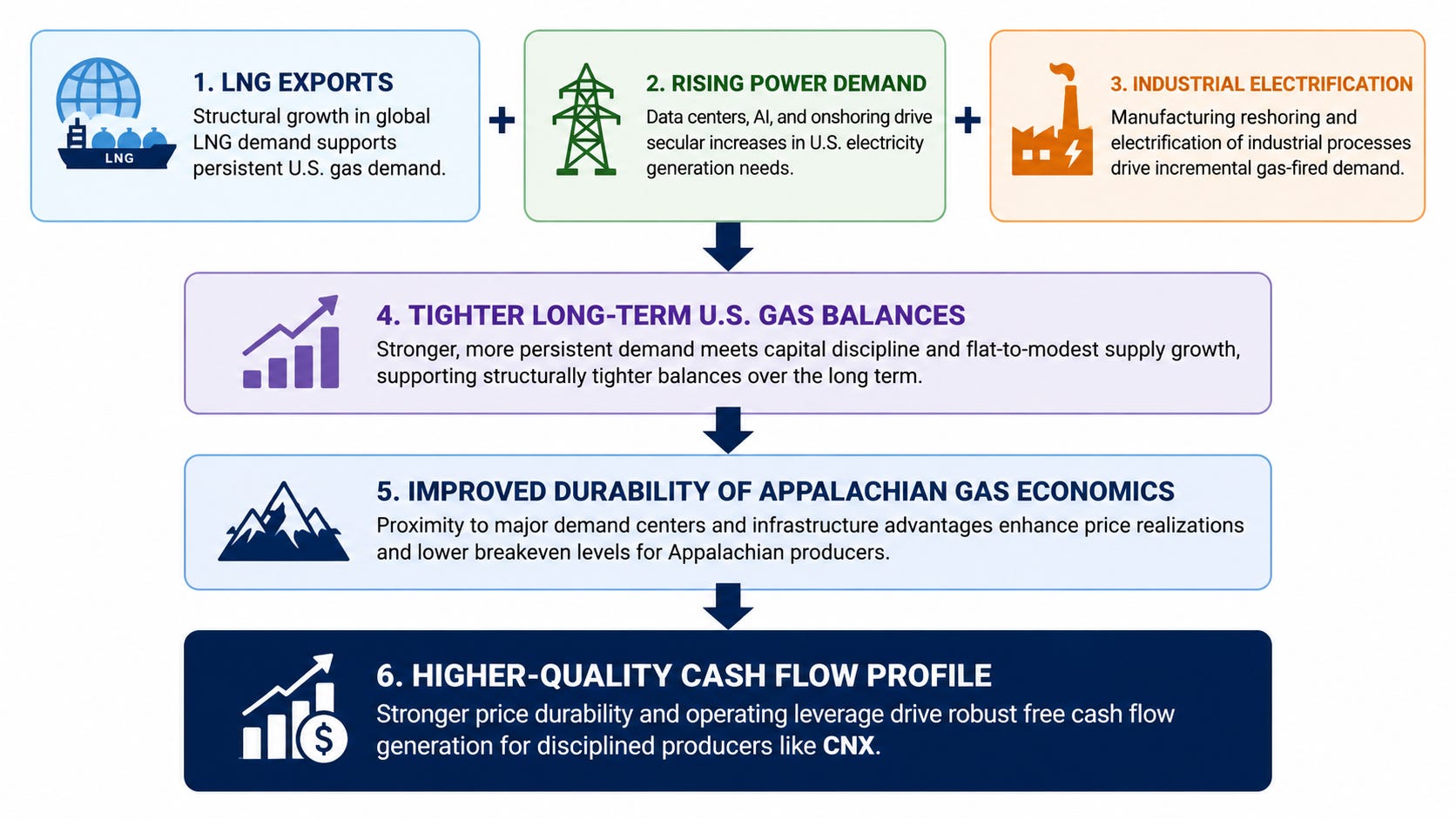

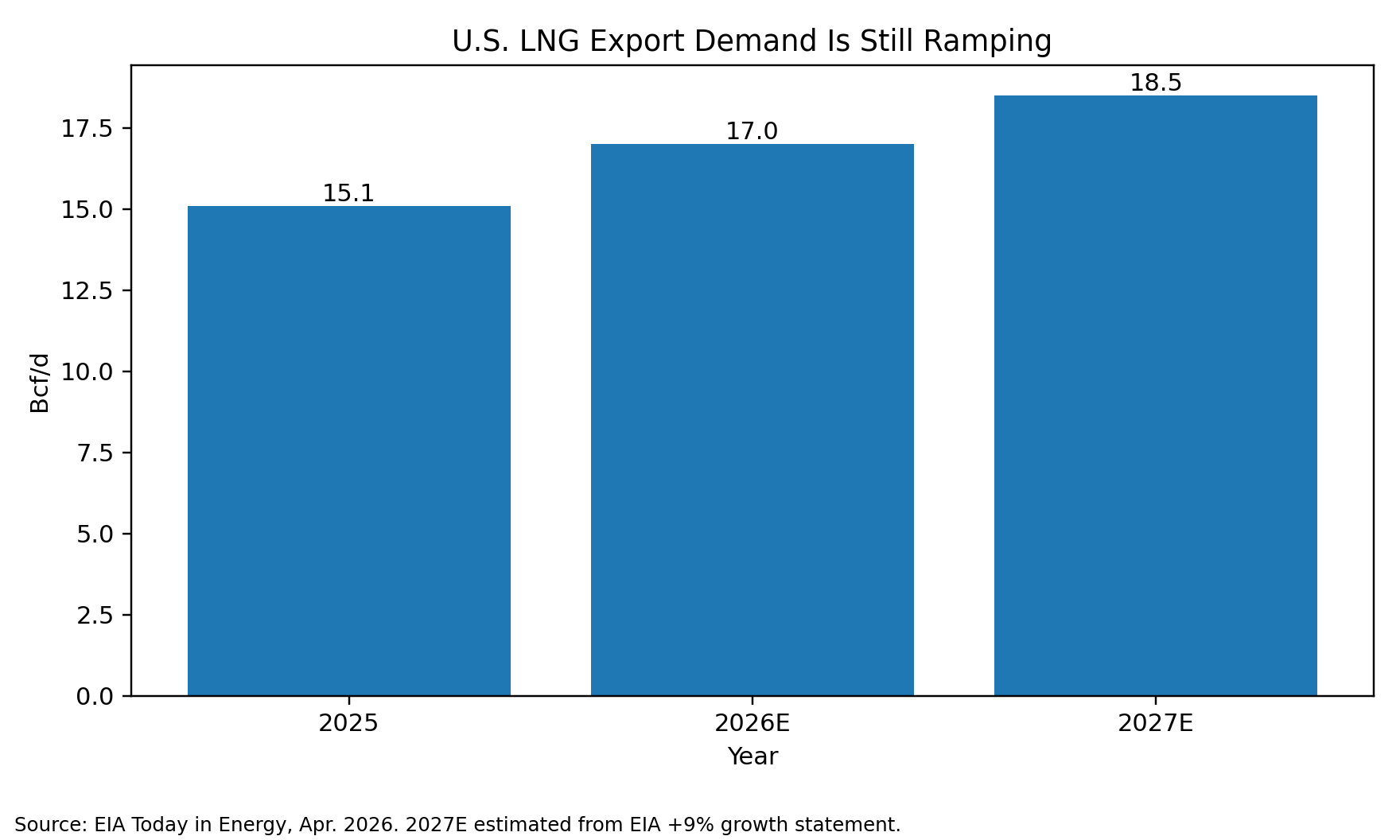

LNG exports are steadily globalizing U.S. gas markets, while AI-related power demand, industrial reshoring, and grid reliability needs are increasing the strategic importance of dispatchable natural gas generation.

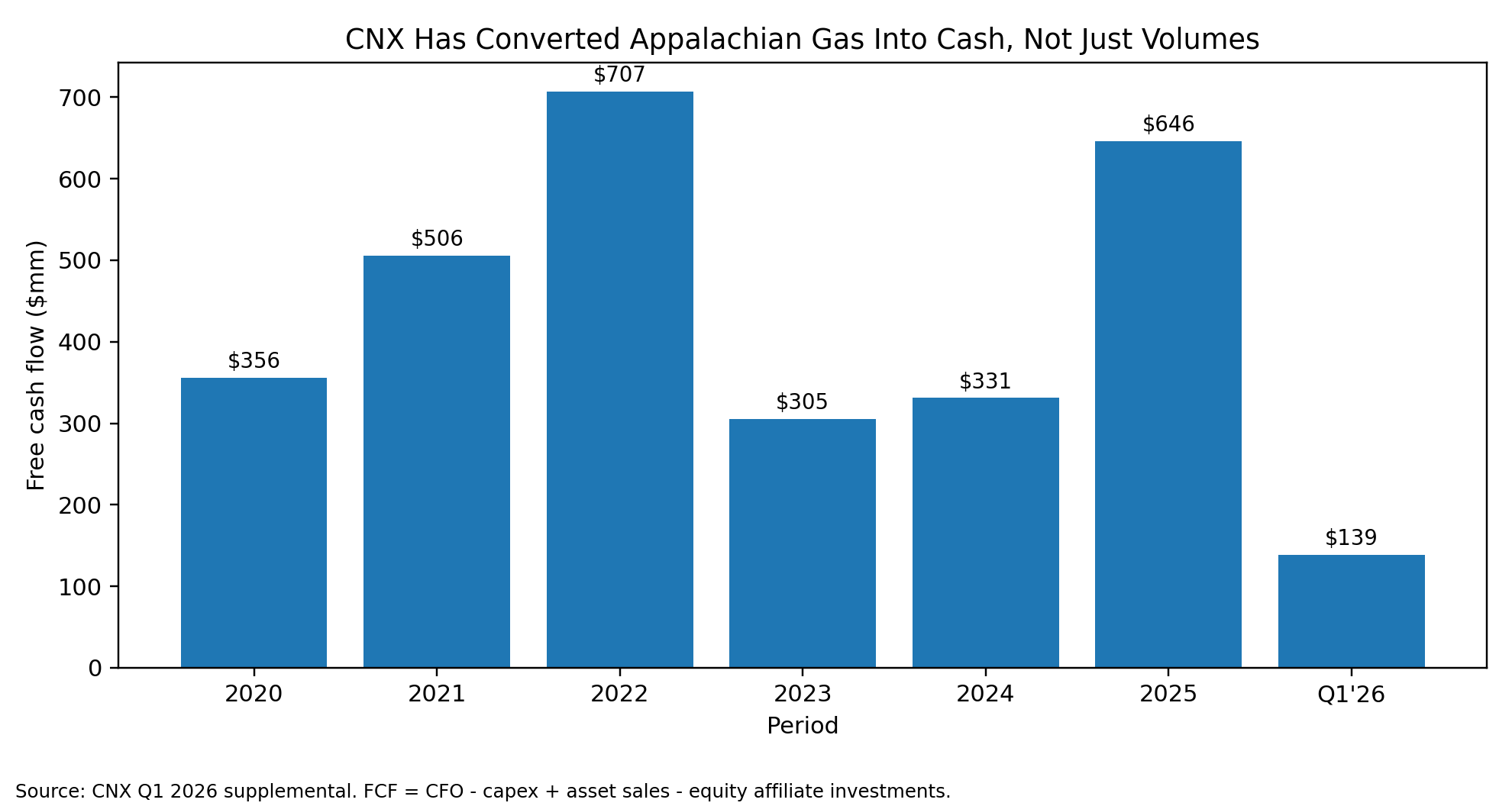

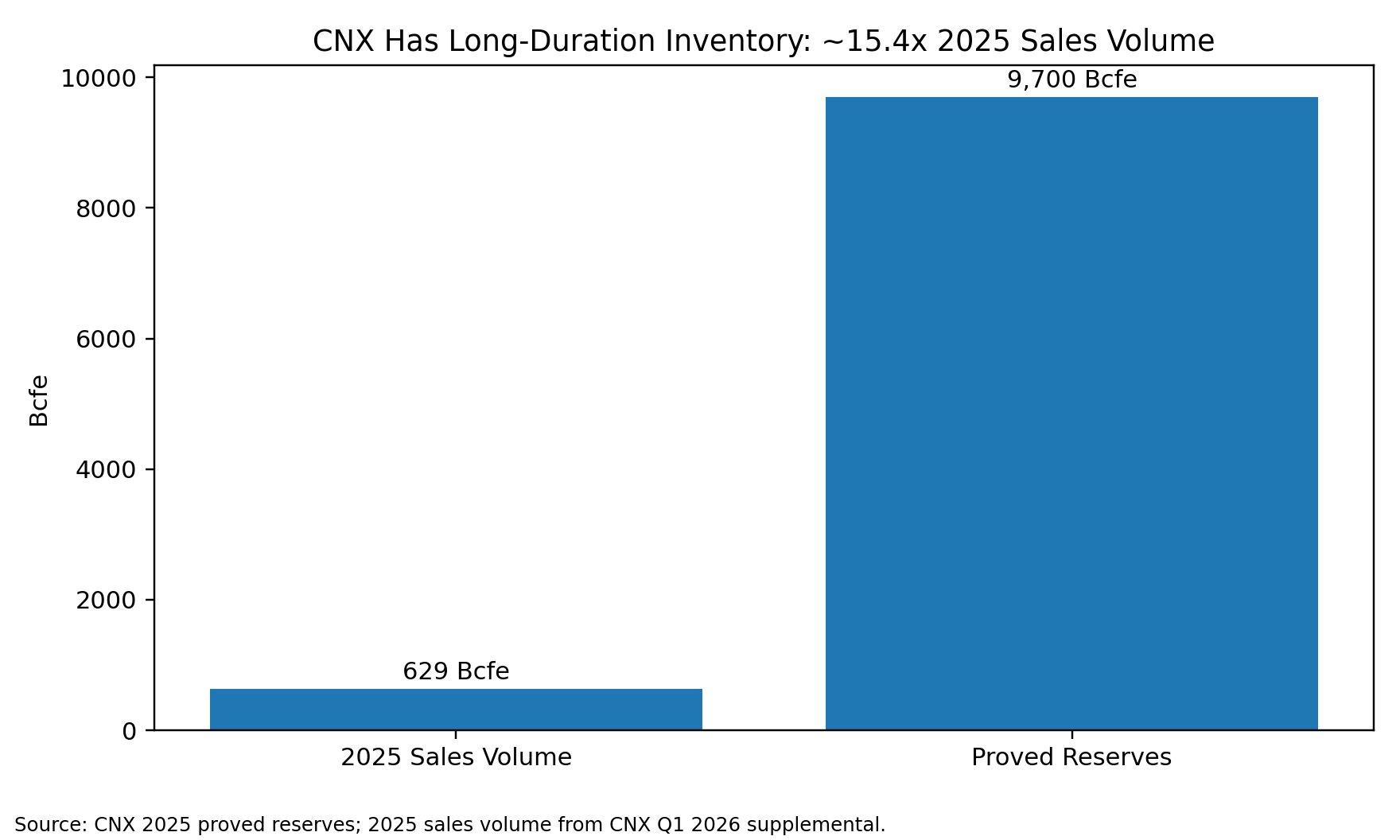

CNX benefits from that shift indirectly rather than explicitly. The company generated roughly $646mm of FCF in 2025 and reported 9.7 Tcfe of proved reserves, giving it meaningful reserve duration without requiring aggressive production growth.

The thesis is less about near-term gas torque and more about the possibility that long-duration U.S. gas reserves deserve a higher quality multiple if domestic and global gas demand remain structurally firmer than the market expects.

Company Overview

CNX Resources Corporation is an Appalachian natural gas producer focused on development, production, and midstream operations across the Marcellus and Utica regions. The company’s appeal is mainly capital discipline. CNX has consistently prioritized:

Free cash flow generation

Share repurchases

Long reserve life

Controlled capex intensity

That matters because Appalachian gas historically suffered from a “trapped commodity” narrative: abundant supply, weak regional pricing, and limited export pathways. The setup is slowly improving.

The company reported 9.7 Tcfe of proved reserves as of year-end 2025, providing significant inventory duration relative to current production levels.

Causal Mechanism

The thesis does not require CNX to become directly tied to AI infrastructure spending like many other natgas plays out there right now. Instead, the mechanism is:

U.S. LNG exports continue to rise as global buyers seek non-Russian (and non-blockaded?) energy supply in addition to long-term energy security for AI buildouts.

At the same time, natural gas remains one of the few scalable and dispatchable power sources capable of supporting incremental grid load growth. AI-related data-center demand is part of that backdrop, but only one component of it. The important distinction is that CNX is not really a “theme stock.” It is a fundamentally solid gas asset that may benefit from second-order thematic tailwinds:

LNG export growth

Grid reliability demand

Industrial reshoring

AI-related electricity consumption

Key Risks

The largest risk is simple: CNX is still a commodity-linked equity. Natural gas prices remain volatile and heavily influenced by:

Weather

Storage levels

Production growth

LNG outage risk

Pipeline constraints

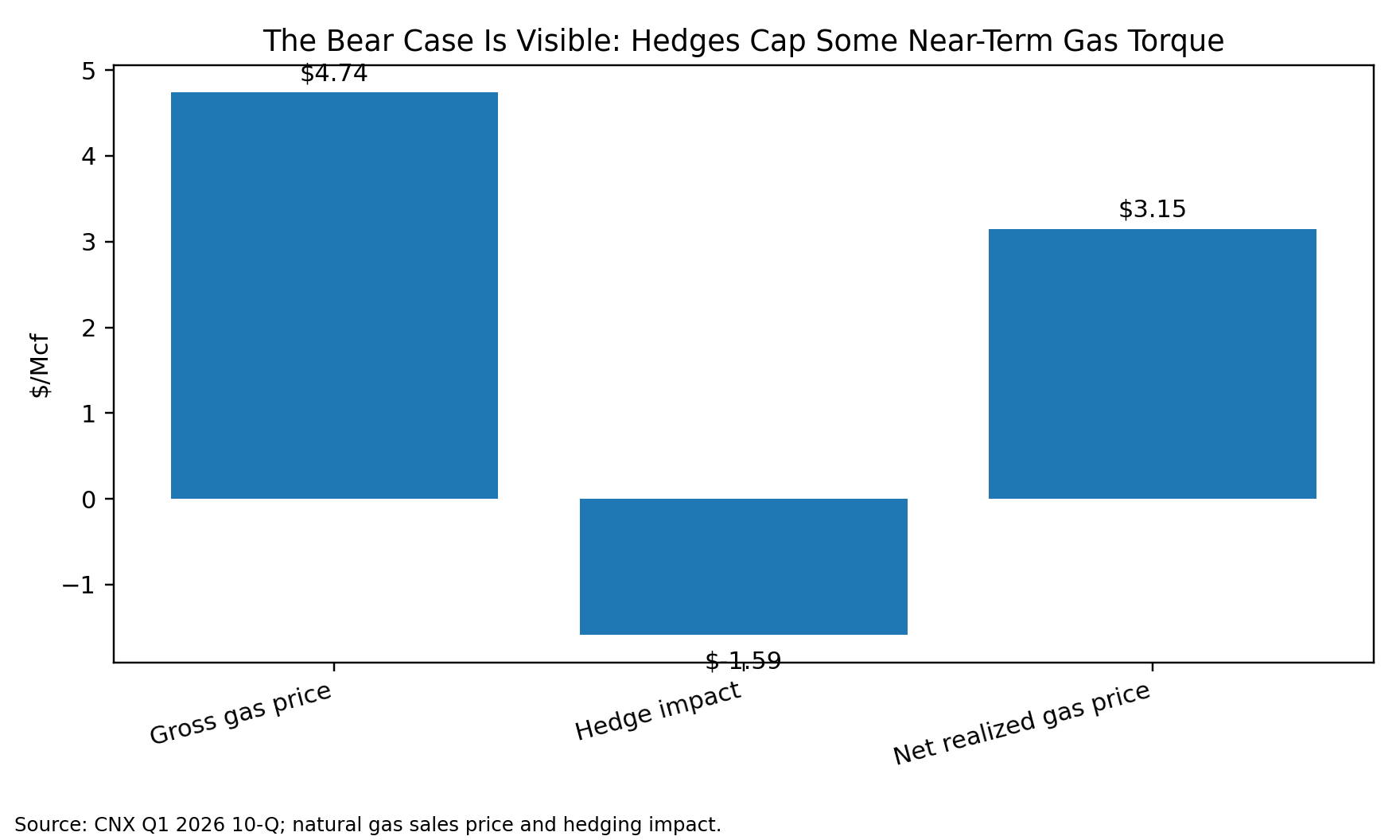

CNX also actively hedges production, which can reduce upside participation during stronger gas environments:

There is also persistent regulatory and infrastructure risk in Appalachia, particularly around pipeline permitting and regional basis dynamics. Finally, if LNG demand growth or power-load growth disappoints, the market may continue treating Appalachian gas reserves as structurally low-multiple assets.

Conclusion

CNX is best viewed as a disciplined, cash-generative Appalachian gas producer with long-duration reserves and improving macro context. The investment case does not directly rely on speculative AI enthusiasm or aggressive production growth. Instead, it rests on a more incremental but credible idea:

U.S. natural gas may remain strategically important for longer than the market expects, and long-life, free-cash-flow-oriented gas assets could be revalued accordingly.

CNX offers exposure to that possibility through reserve depth, capital discipline, and shareholder-oriented cash deployment rather than growth narratives.

Great article man, actually interesting which is rare to find

Subscribed, would love to have you along too🙂