The Industrial REIT With Embedded Convexity

LXP’s land bank could quietly convert into years of new NOI and NAV growth the market isn’t modeling.

Affiliation Disclosure & Disclaimer:

The managing principal of Ridire Research is affiliated with a private investment fund that holds long positions in the securities discussed herein (LXP Industrial Trust, LXP), which could influence the views expressed. This publication is for educational and informational purposes only. Any performance referenced is illustrative and tracked on a per-article basis, not as part of a model portfolio or investment program. Nothing herein constitutes investment advice, a recommendation, or a solicitation. → Ridire Research Substack Disclaimer

Table of Contents

Why This Story Is Different

Start With What Already Works

The Real Story Is the Development Spread

Phoenix Is the Bridge From Optionality to Reported Earnings

Why This Deserves More Credit Than a Typical Land Narrative

The Balance Sheet Makes the Optionality Actionable

What Has to Happen for the Stock to Work

What Would Break It

Bottom Line

Why This Story Is Different

LXP is not a direct AI stock. But it may be an indirect AI and MAGA/protectionist winner: its Phoenix land bank sits in the path of semiconductor reshoring, advanced manufacturing migration, and a broader policy push to localize strategic supply chains.

Most REITs are not transformation stories rather they are cash-flow vehicles. Investors buy current income, modest rent growth, balance-sheet discipline, and some NAV accretion over time. LXP is more interesting because it may no longer fit neatly inside that box.

The company today looks like a credible, stabilized industrial landlord. But inside that stabilized portfolio sits something more valuable than “extra land.” It sits on a development pipeline that could convert dormant carrying value into future NOI, NAV creation, and a better growth profile than a standard industrial REIT screen implies.

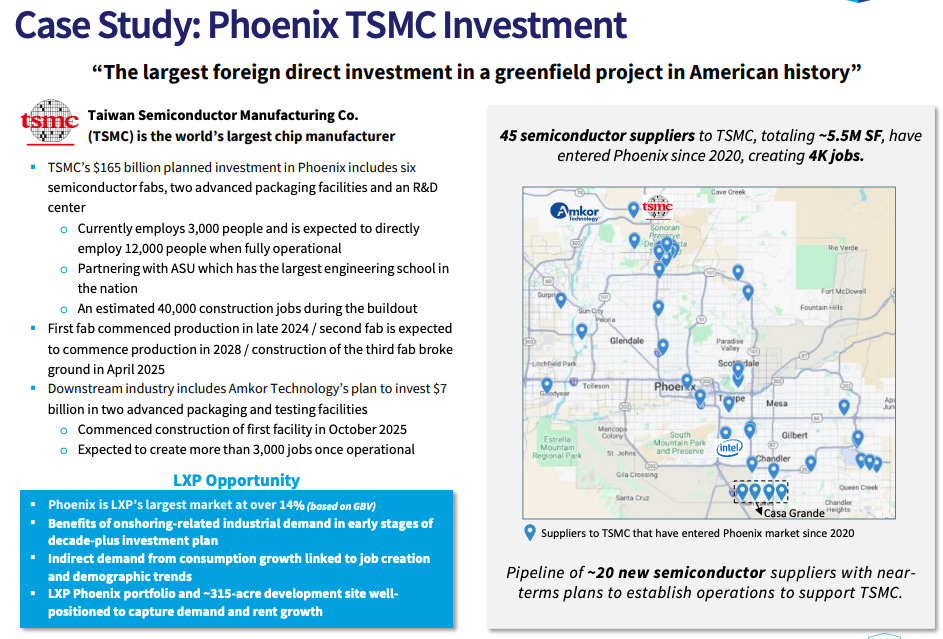

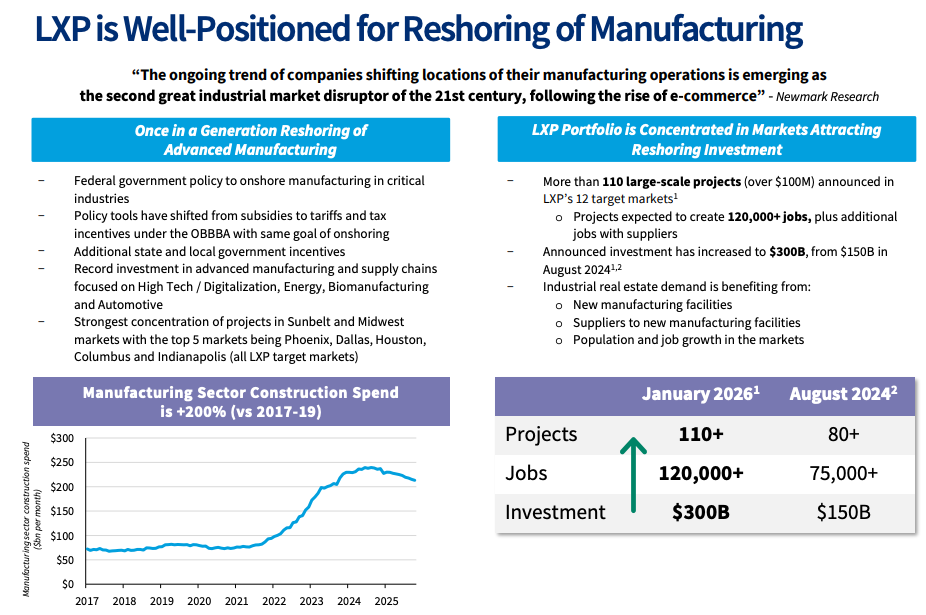

There is also a timely macro layer here that makes the story more relevant than a normal land-bank pitch. LXP is not an AI stock in the conventional sense, but it is arguably an indirect beneficiary of the same capex cycle. Management has pointed to advanced manufacturing tailwinds tied to TSMC and semiconductor supply-chain migration into Phoenix.

That makes LXP a second-order AI infrastructure and domestic industrial-policy beneficiary because it owns land in a market that may increasingly absorb the warehousing, logistics, and supplier footprint created by semiconductor reshoring and protectionist supply-chain realignment. This is not really a “land story.” It is a land-to-NOI conversion story with a potentially favorable macro backdrop.

Start With What Already Works

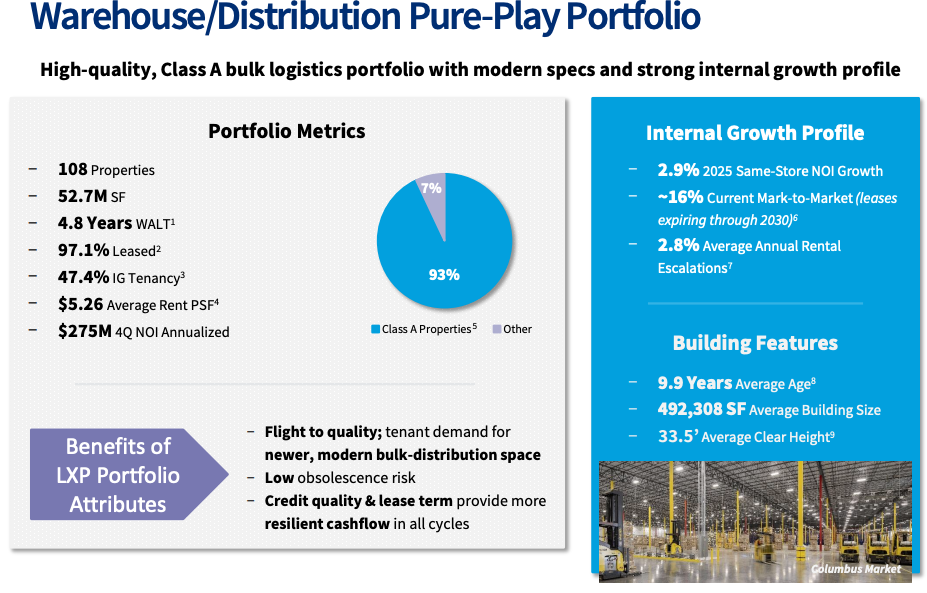

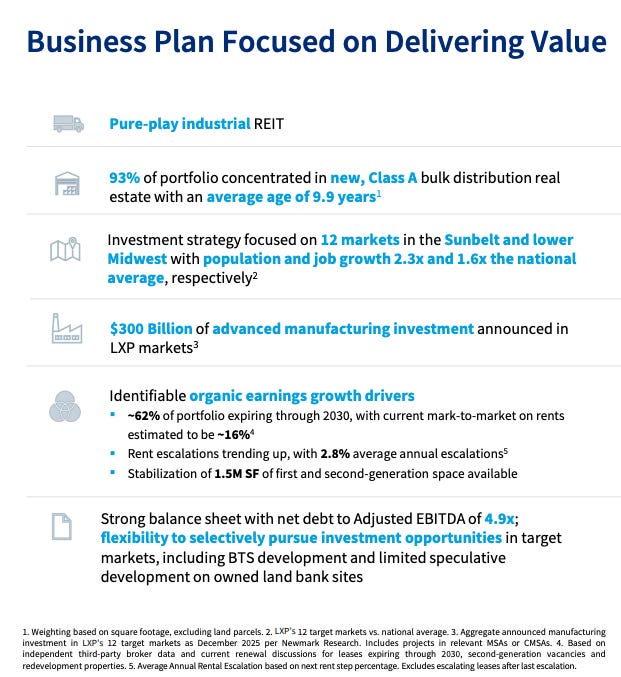

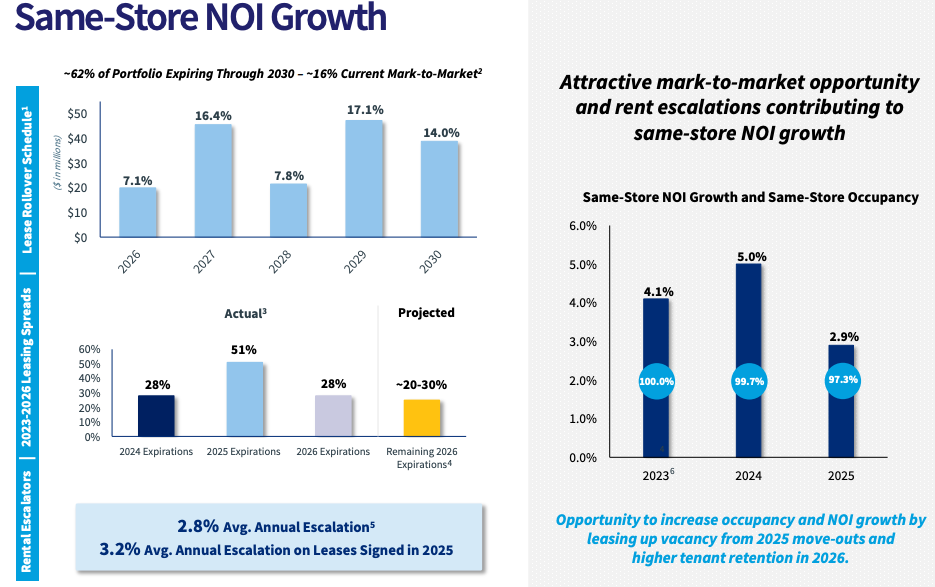

As of year-end 2025, the company owned 108 properties totaling 52.7 million square feet. Roughly 92.6% of square footage was Class A. The portfolio was 97.1% leased with a weighted-average lease term of 4.8 years. It also controlled 514 acres of developable land. The stock does not require a heroic view on development to be investable. The base business is already a modern industrial platform with solid occupancy and a reasonably clean portfolio.

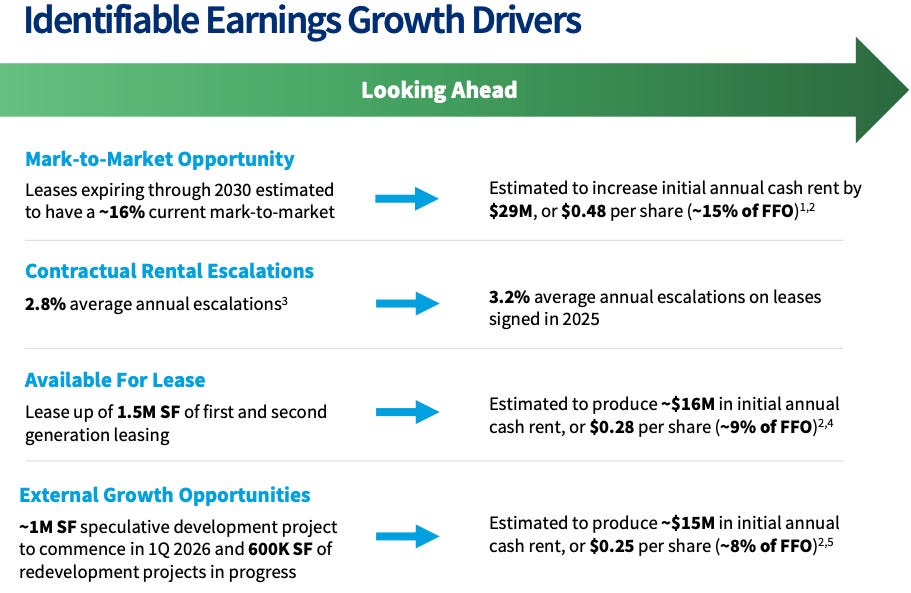

The internal earnings bridge also looks better than a simple REIT screen may suggest. Management’s fourth-quarter presentation notes that leases expiring through 2030 carry an estimated current mark-to-market of roughly 16%, enough to increase initial annual cash rent by about $29 million, or roughly $0.48 per share, equal to about 15% of FFO. The same presentation says LXP has 1.5 million square feet available for lease, which could add another roughly $16 million of initial annual cash rent, or about $0.28 per share. Layer in average annual rental escalations of 2.8%, with 2025 signed leases carrying average annual escalations of 3.2%, and the existing portfolio already has credible internal growth. Even before the development pipeline contributes meaningfully, LXP has a clear path to higher rents, better occupancy, and incremental earnings.

The Real Story Is the Development Spread

The market usually values REITs by capitalizing current or near-term NOI. That works well for stabilized portfolios. It works poorly when part of the asset base is held in land that generates little current income but can be developed into higher-value industrial product. In those cases, book value can be a misleading anchor. The relevant economic question is not what the land is worth sitting still. It is what the company can earn by building on it.

LXP’s filings show land held for development at roughly $82.97 million on the consolidated balance sheet, with another $11.47 million in non-consolidated land projects. The consolidated land table shows 315 acres in Phoenix carried at about $75.4 million. But the heart of the thesis is whether LXP can convert that land into stabilized industrial product at returns above what the market will ultimately pay for those assets.

If LXP can consistently develop industrial assets at 7%-plus stabilized cash yields and the market values comparable stabilized product at materially tighter cap rates, the value creation is mechanical. The land bank becomes a pipeline of future NAV accretion rather than a passive balance-sheet line item.

Phoenix Is the Bridge From Optionality to Reported Earnings

Phoenix is the clearest expression of that mechanism.

In its 2025 annual letter, management says the company’s 514-acre land bank includes 315 acres in Phoenix. It has already broken ground on a 1.2 million square foot speculative development project there with projected completion in the first half of 2027, an estimated budget of $120 million, and a stabilized cash yield expected in a range of 7.0% to 7.5%. More importantly, management says the remaining 240 acres at the site can support up to four million square feet of industrial development.

This is a multi-year inventory of future NOI.

Phoenix matters for another reason: it is where the macro overlay meets the financial model. Management notes that construction costs are about $20 per square foot below peak levels and points to advanced manufacturing tailwinds tied to TSMC and semiconductor supply-chain migration into Phoenix. That makes the project more than a generic Sun Belt warehouse build. It potentially places LXP inside a broader reshoring and industrial-policy current that has both AI and protectionist characteristics. AI does not only require chips and data centers. It also requires domestic manufacturing ecosystems, supplier networks, and logistics infrastructure. Phoenix is becoming one of those ecosystems.

The key point is not that every macro tailwind must fire perfectly. It is that LXP appears to control land in a market where large-box industrial demand may remain strategically supported, and where the economics of building today look better than they did at peak cost.

As long as land remains land, upside stays abstract. Once the first building is delivered, leased, and stabilized, the market has to stop treating the site as dormant optionality and start treating it as an earnings pipeline. Optionality only rerates when it becomes legible in reported results.

Why This Deserves More Credit Than a Typical Land Narrative

Many companies can point to undeveloped acreage. Far fewer can show an operating history of converting land into value. That is why LXP’s execution record matters so much here.

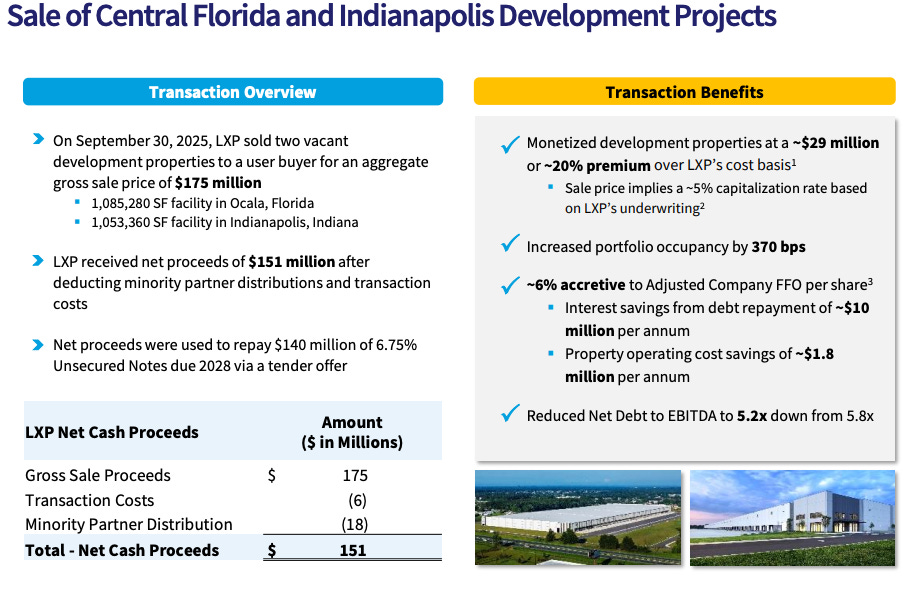

Management says it has constructed 15 facilities since 2019 at a 7.1% weighted-average stabilized yield on first-generation leases and generated $91 million of sales proceeds in excess of cost basis. It also says that in 2025 it sold the Indianapolis and Ocala development properties for $175 million to a user buyer at an implied 5% capitalization rate and a 20% premium to initial cost basis:

That is a highly important proof point. It suggests the upside is not merely “Phoenix land is probably worth more than book.” The stronger claim is that LXP has already shown it can build at one yield and monetize at another. That spread is what turns development from a story into a capital-allocation engine. In other words, the bull case is essentially repeated spread capture.

The Balance Sheet Makes the Optionality Actionable

Optionality in REITs is useless if the balance sheet cannot support it. LXP looks more interesting now because that constraint appears to be easing.

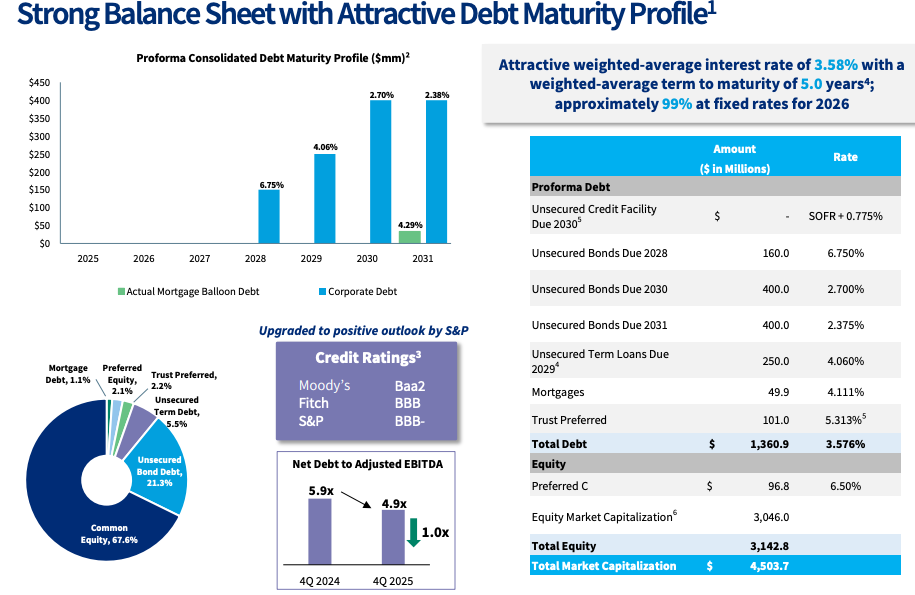

At year-end 2025, the company reported net debt to Adjusted EBITDA of 4.9x after selling assets, repaying debt, and reducing exposure to non-target markets. In the annual letter, management explicitly says that with its key 2025 objectives achieved, 2026 capital allocation priorities will focus on development opportunities, primarily within the existing land bank, while still leaving room for opportunistic buybacks.

That statement is more important than it sounds. It marks a shift from portfolio repair and simplification toward deliberate capital deployment. The thesis strengthens materially once investors believe LXP has both the land and the financial flexibility to start converting it. The distinction here matters:

A land bank on a stressed balance sheet is deferred optionality.

A land bank on a repaired balance sheet is potential growth inventory.

What Has to Happen for the Stock to Work

The mechanism is straightforward:

First, the existing portfolio continues to compound through rent mark-to-market, escalators, and lease-up. That supports earnings growth even without any heroic development assumptions.

Second, the cleaner balance sheet allows capital to move toward development inside the land bank, especially Phoenix.

Third, development starts become delivered buildings, delivered buildings become leased buildings, and leased buildings become stabilized NOI. At that point, the market no longer has to value those acres as dormant land.

Fourth, as the contribution becomes visible, LXP can begin to look less like a plain industrial landlord and more like an industrial REIT with an internal development engine. That is the point where the valuation framework can shift.

That chain is the entire thesis:A sequence of conversion from land to buildings to NOI to NAV.

What Would Break It

The biggest risk is that the spread never gets realized:

If industrial demand softens, speculative leasing stalls, construction costs re-accelerate, or capital becomes less available, the land bank can remain underutilized for longer than bulls expect. In that outcome, the acreage still exists, but the timing of value realization stretches materially.

There is also clear concentration in the upside case. Phoenix is the crown jewel. If Phoenix performs, the thesis becomes more obvious. If Phoenix disappoints, the stock may still work as a decent industrial REIT, but the argument for material upside weakens.

Finally, rerating is not automatic. A REIT can create real value and still trade as if it were only a current-income vehicle for longer than investors expect. The market often requires repeated proof before it changes the box it puts a company in.

Bottom Line

LXP is a stabilized industrial REIT whose current earnings base may understate the value of a real internal development pipeline.

The existing portfolio already supports ownership through rent growth, lease-up, and a healthier balance sheet.

The Phoenix land bank is what adds asymmetry. And that asymmetry is not happening in a vacuum: Phoenix is also exposed to semiconductor reshoring, advanced manufacturing buildout, and a more protectionist domestic supply-chain regime, which makes LXP an indirect beneficiary of both the AI capex cycle and the political push to localize strategic production.

If management keeps converting low-carry-value land into 7%-plus stabilized industrial product, and if the market continues to value finished assets at materially tighter cap rates, then LXP has a credible path to create more NAV and more future NOI than a standard REIT multiple implies today.

In short LXP is a landlord with a visible path to turn land into earnings in a market increasingly shaped by AI infrastructure demand and industrial reshoring.