The Payments Spin Nobody Believes In

A deeply discounted payments platform where modest execution could drive an outsized re-rating.

Affiliation Disclosure & Disclaimer:

The managing principal of Ridire Research is affiliated with a private investment fund that holds long positions in the securities discussed herein (GPN US) which could influence the views expressed. This publication is for educational and informational purposes only. Any performance referenced is illustrative and tracked on a per-article basis, not as part of a model portfolio or investment program. Nothing herein constitutes investment advice, a recommendation, or a solicitation. → Ridire Research Substack Disclaimer

Table of Contents

Executive Summary

Company Overview

The Setup

Causal Mechanism

Timeline

Key Risks

Conclusion

Executive Summary

Management sold Issuer Solutions, bought Worldpay and described the result as a focused merchant-commerce company. Investors heard a more familiar story: another large payments deal, another integration, more debt and another set of adjusted numbers.

Global Payments (GPN US) is interesting precisely because the transaction looks like the opposite of simplification.

Underneath the deal structure is a cleaner product map. Integrated payments, vertical software, point of sale, enterprise acquiring, ecommerce and international distribution now point at the same buyer: the merchant. The company no longer has to split capital and attention between merchant commerce and a separate issuer-processing business.

The important nuance is that this is not an integration-success story (yet). It is an integration-proof story. Global Payments does not need to become a high-growth software company. It needs to show that a much larger merchant platform can preserve growth, remove duplicate cost, keep service stable and turn reported earnings into cash.

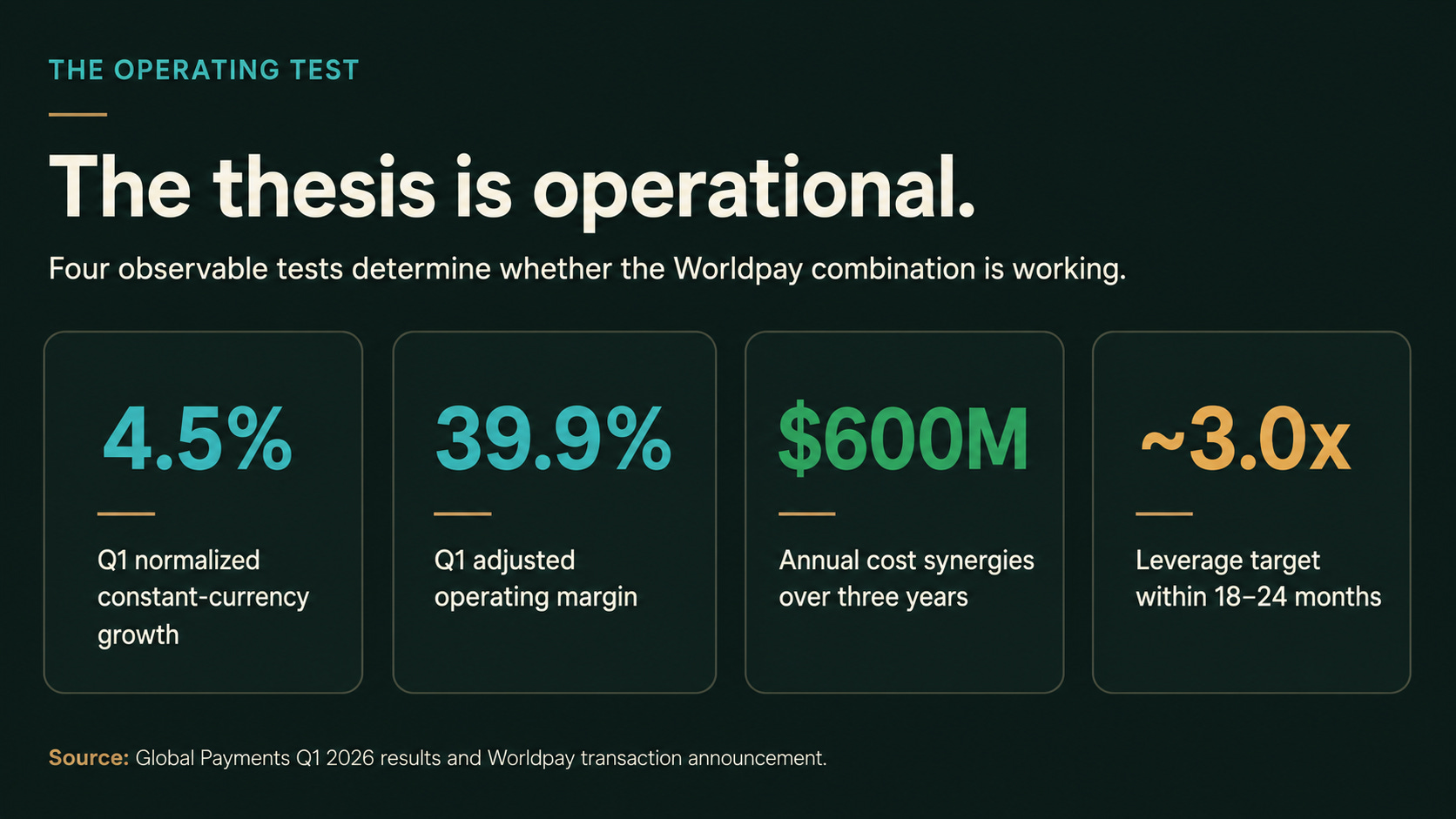

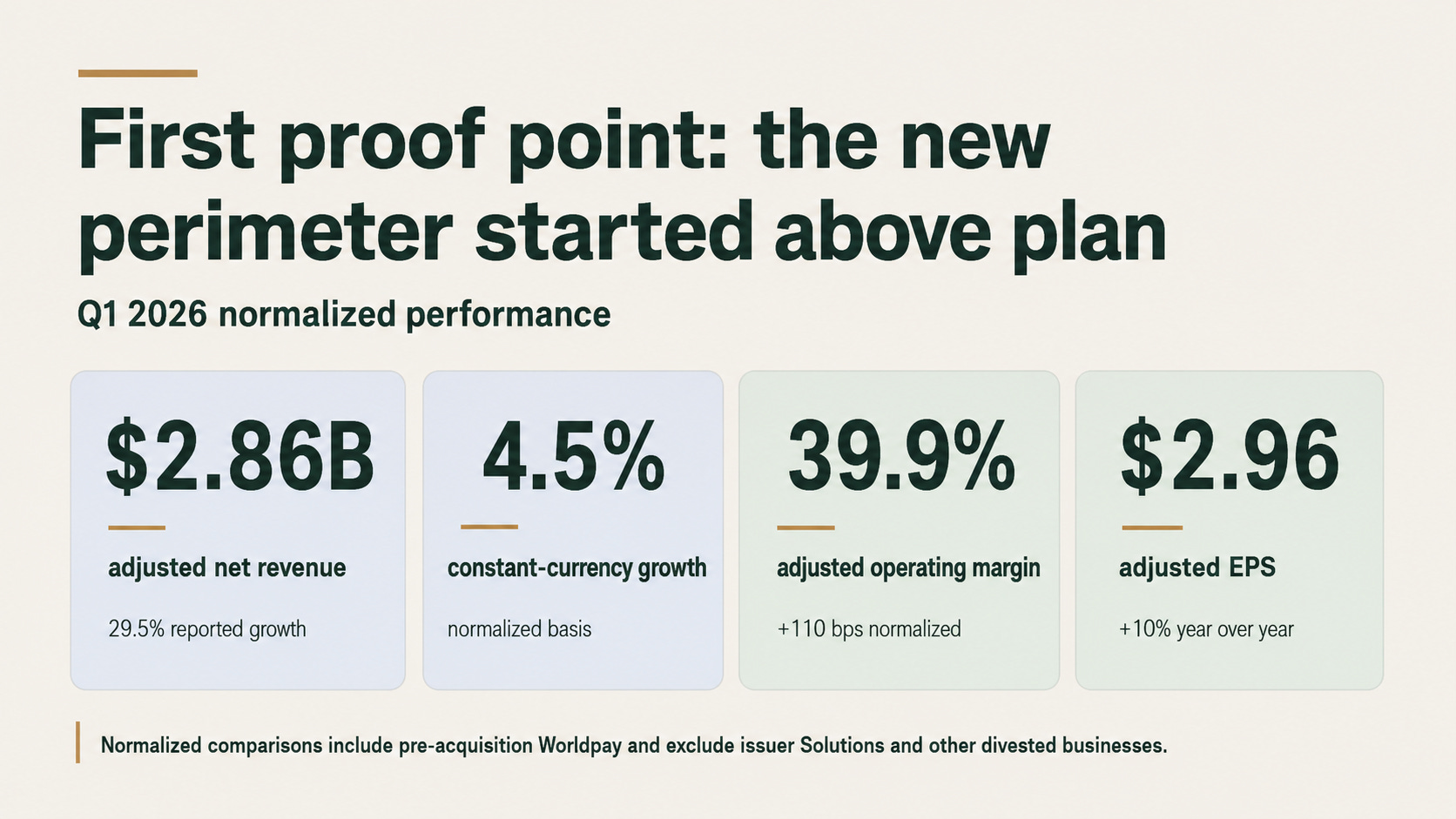

In Q1 2026, adjusted net revenue was $2.86 billion, normalized constant-currency growth was 4.5%, adjusted operating margin reached 39.9% and adjusted EPS was $2.96. Management said the quarter finished above internal expectations and kept the full-year framework intact. One quarter does not settle a multi-year integration, but the combined perimeter did not begin with an obvious operating break.

What makes the setup workable is that the next phase is visible.

The company has disclosed $600 million of annual cost synergies over three years, at least $200 million of revenue synergies over time and a leverage objective of roughly 3.0x within 18-24 months.

The merchant perimeter is more coherent than the transaction optics suggest.

Integrated and embedded payments were already the strongest organic growth engine before Worldpay.

Worldpay adds enterprise, ecommerce and international reach that Global Payments did not have at the same scale.

The next six quarters should show whether the larger platform is becoming easier or harder to operate.

The market sees a serial acquirer. The product map increasingly looks like a merchant platform. Both views can be true at once. The investment question is which one becomes more visible in the financials?

Figure 1 - The operating test. Q1 establishes the baseline; the synergy and leverage targets define the next phase.

Company Overview

Global Payments sits behind the checkout. It authorizes transactions, settles funds, manages fraud, connects merchants to software, powers point-of-sale systems and supports commerce across physical and digital channels.

That description sounds generic because payments infrastructure is supposed to disappear into the background. Merchants only notice it when authorization rates fall, settlement breaks, software stops talking to the processor or support becomes slow. The product is therefore part utility and part workflow. Processing provides scale; software and embedded distribution make the relationship harder to replace.

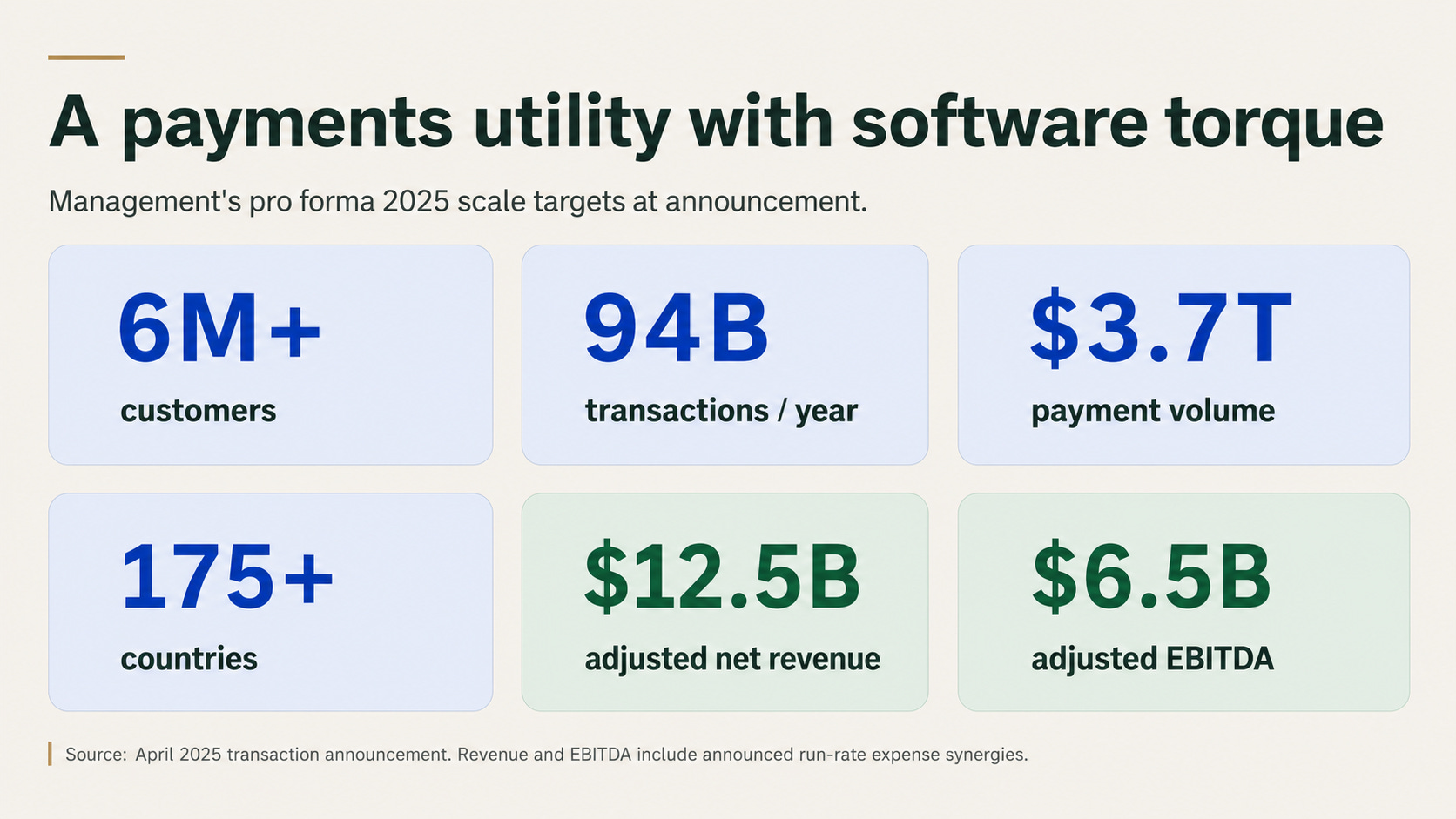

The Worldpay transaction materially enlarges that system. At announcement, management described a combined platform serving more than 6 million customers, processing roughly 94 billion transactions and $3.7 trillion of payment volume across more than 175 countries. There is real scale here, the harder question is whether it becomes useful scale.

Before Worldpay, Global Payments reported three merchant service lines:

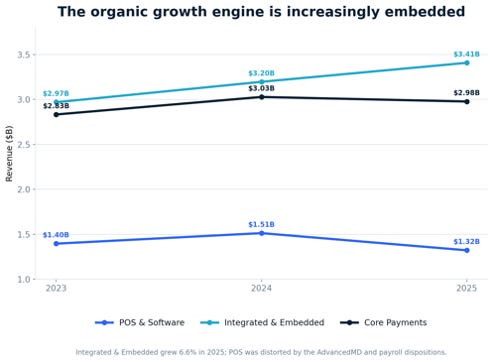

Integrated & Embedded generated about $3.41 billion of 2025 revenue and was the clearest organic growth engine.

Core Payments produced roughly $2.98 billion and was broadly flat.

POS & Software contributed about $1.32 billion, with comparisons affected by the AdvancedMD and payroll disposals.

This mix tells us the most interesting part of the business is the distribution layer around it. When payments are built into restaurant software, dealer-management systems, healthcare workflows or vertical SaaS, the processor reaches the merchant through a product the merchant already uses to run the business.

Worldpay adds a different kind of reach: larger enterprise merchants, ecommerce, cross-border capability and a broader international footprint. Global Payments contributes more vertical software and embedded distribution. The strategic case rests on those pieces becoming complementary rather than simply larger.

Figure 2 - Pro forma scale at the April 2025 transaction announcement. Revenue and EBITDA include announced run-rate expense synergies.

Figure 3 - Integrated & Embedded was the clearest reported growth engine before Worldpay.

The Setup

The setup is essentially a credibility gap:

Investors see a company that promised simplification and then announced another large acquisition.

The product map shows a company that sold the non-merchant business and concentrated the remaining portfolio around commerce.

Global Payments can be strategically more focused and operationally more complicated at the same time. That is what makes the next year important.

The April 2025 announcement landed badly because the burden of proof was already high:

Payments has spent years consolidating, separating and recombining assets.

Worldpay itself moved from Vantiv to FIS, then into a private-equity-controlled structure, and now into Global Payments.

Investors were being asked to believe that another owner could integrate the same large processing estate more effectively.

The transaction closed on January 9, 2026, which is when the operating clock actually started. Q1 was therefore a baseline. The 4.5% normalized constant-currency growth rate and 110 basis points of normalized margin expansion matters because they showed no immediate collapse in the combined perimeter.

The more important signal may be governance:

In September 2025, Global Payments added two independent directors in cooperation with Elliott Investment Management and created a dedicated Integration Committee to oversee Worldpay and synergy realization.

That does not guarantee execution, but it moves the integration closer to the board and makes slippage harder to hide behind broad strategic language.

We are not claiming this will be a seamless integration. The base case is that merchant growth and service remain intact while duplicate infrastructure and overhead come out. If that happens, the transaction begins to look like a difficult simplification rather than another layer of complexity.

Figure 4 - The first consolidated proof point. Normalized comparisons include pre-acquisition Worldpay and exclude Issuer Solutions and other divested businesses.

Causal Mechanism

The causal mechanism is a distribution-stack story:

Merchants rarely wake up wanting a new payment processor. They want a restaurant system that reduces order errors, a dealership platform that reconciles payments, an ecommerce stack that improves authorization or a checkout that works across store, mobile and web. Payments becomes more valuable when it is attached to the operating workflow.

Global Payments already had a meaningful position in that layer. Its Integrated & Embedded service line grew from roughly $2.97 billion in 2023 to $3.41 billion in 2025, while the other two reported lines were flatter or affected by divestitures. That is the clearest evidence that software-led distribution, rather than commodity processing alone, is the part of the model with the best organic shape.

Worldpay broadens the top of the funnel. It adds enterprise merchants, ecommerce volume, international acceptance and a large installed base through which Global Payments can sell fraud tools, omnichannel products, vertical software and value-added services. Global Payments brings more embedded and vertical-market distribution into the combined company. The revenue opportunity is therefore less about inventing a new product and more about moving existing products through a wider set of relationships.

Recent announcements are useful as product-map evidence. Global Payments unveiled an AI-enabled Genius handheld for restaurants, signed an exclusive agreement with CKE Restaurants, expanded its embedded-payments partnership with Lightspeed DMS and had Link2Gov selected as a preferred IRS partner. However, none of those releases disclosed a material revenue contribution. They should be read as evidence that the company still has relevant distribution and product activity during the integration, not as proof that the revenue-synergy target has arrived.

The second part of the mechanism is cost:

Management expects $600 million of annual cost synergies over three years. That target is more controllable than the $200 million-plus revenue opportunity because duplicate vendors, facilities, infrastructure and support functions can be mapped and removed. But cost savings are only useful if the merchant does not feel them first. The clean outcome is lower cost with stable service. The bad outcome is lower cost created by cutting into implementation, support or product development.

The third part is cash:

A transaction this large creates purchase-accounting noise, integration expense and working-capital movement. Adjusted earnings will therefore look cleaner than the cash-flow statement for a while. The right test is not to accept or reject adjusted results on principle. It is to watch whether operating cash flow, capital spending, integration outlays and debt reduction begin to line up over time.

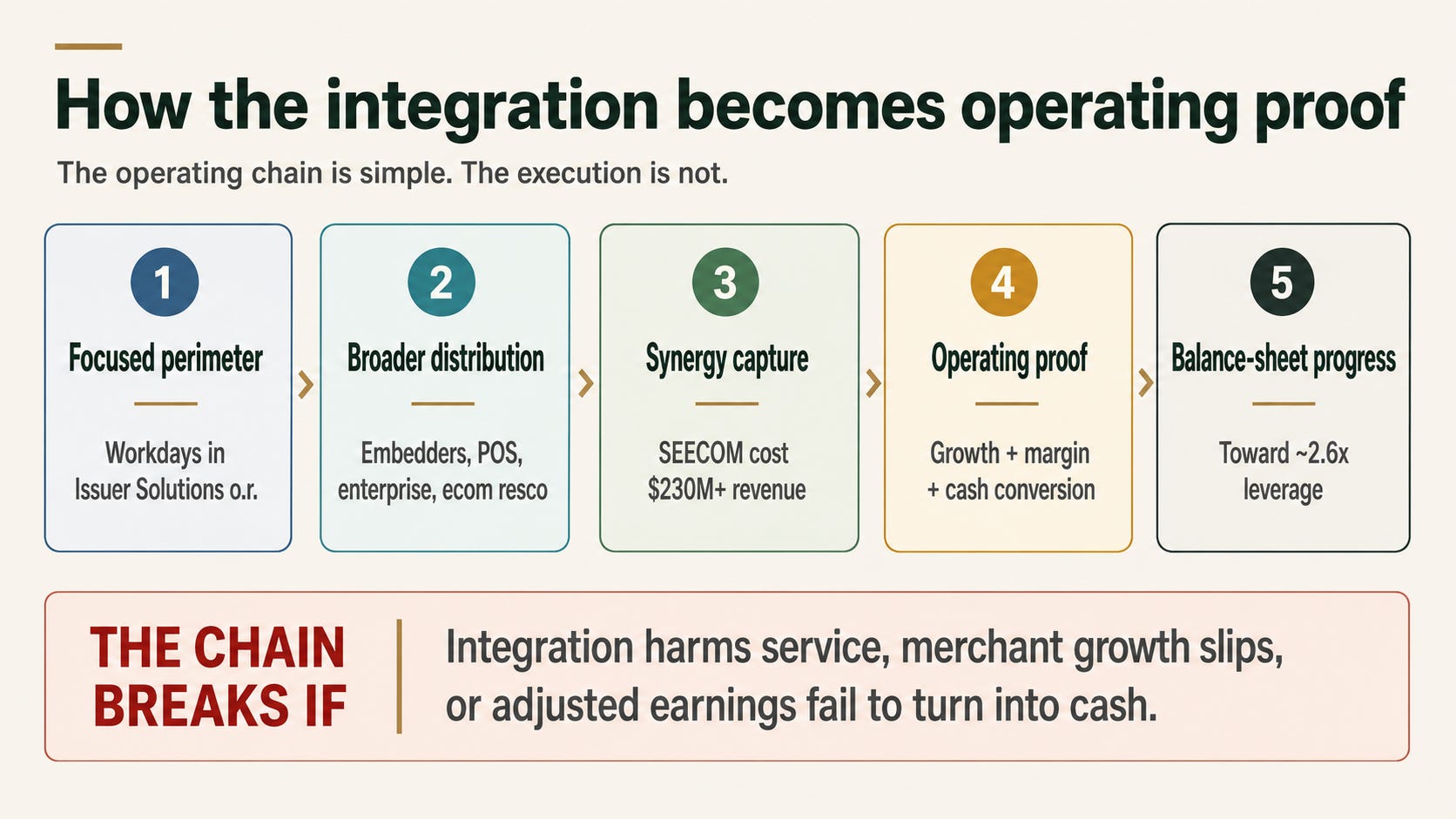

The chain is simple: a focused merchant perimeter creates a more coherent product roadmap; the combined distribution base creates more places to sell those products; cost removal funds investment and improves operating conversion; cash generation gives the company room to reduce leverage. The chain breaks if integration harms service, merchant growth slips or adjusted earnings fail to become cash.

Figure 5 - How the integration becomes operating proof. Management targets are reported; the sequence is Ridire Research interpretation.

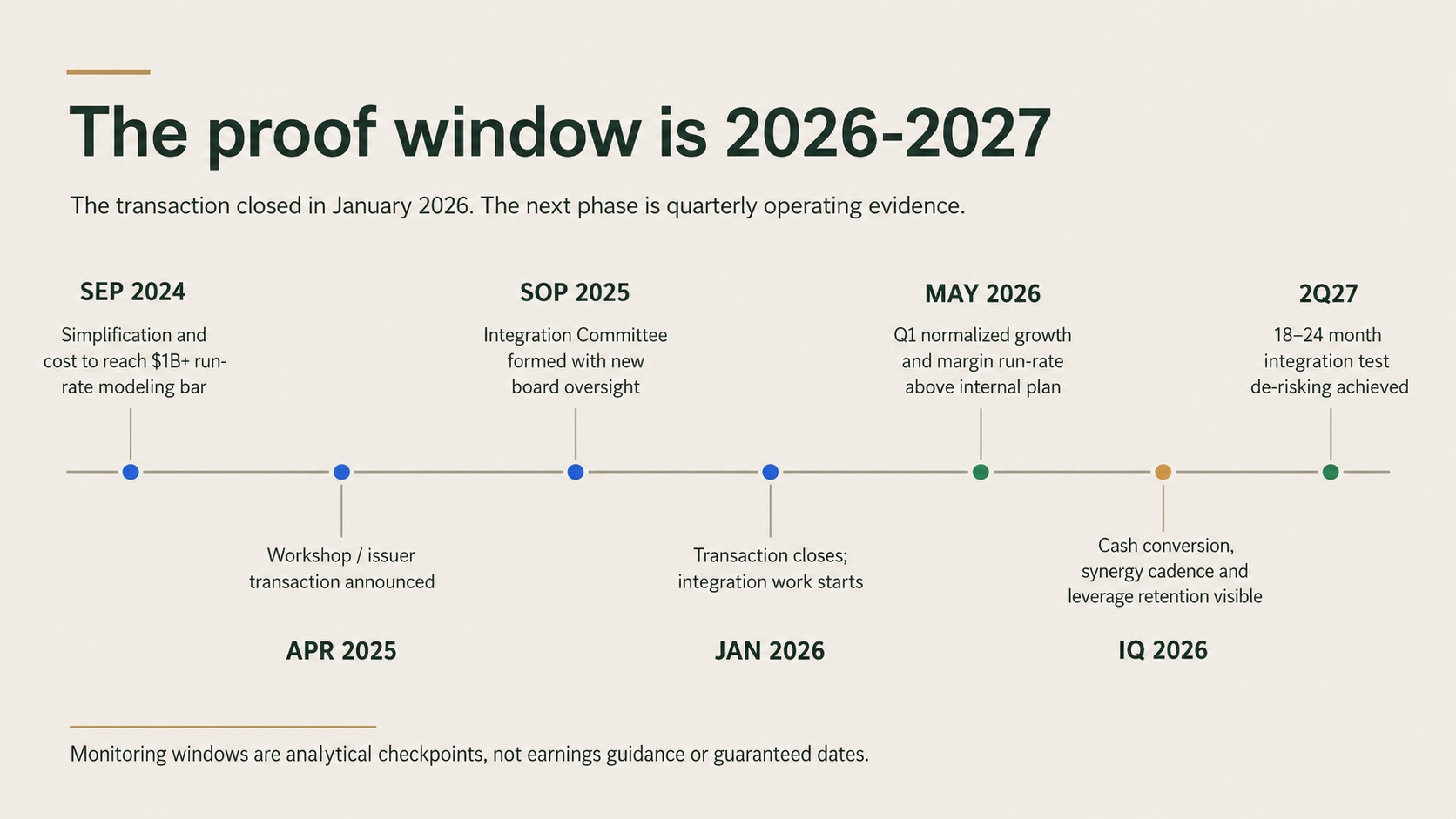

Timeline

The next year is about proof. The second half of 2026 should show whether the Q1 baseline was durable. Normalized growth should remain close to the mid-single-digit framework, margin progress should continue without deterioration in client commentary, and the company should begin making the cash effects of integration easier to understand.

By 2027, the conversation should move from closing the transaction to operating the platform. Investors should be able to see more than cost removal: cross-sell evidence, product adoption, stable retention, fewer duplicated systems and a clearer path toward the leverage objective.

An integration this large can always produce one clean quarter. The important signal is the sequence. Stable growth, margin progress, cash conversion and lower leverage moving together would be difficult to dismiss. A widening gap between those measures would be equally difficult to explain away.

Figure 6 - Timeline.

Key Risks

The right risk lens is straightforward: the deal may be strategically coherent and still be operationally too hard. The main risk is not that electronic payments stop growing. It is that the benefits remain trapped inside a system that is too complex to deliver them cleanly.

Service risk: platform migrations, support changes and cost removal can create outages, slower implementation or merchant attrition.

Growth risk: Worldpay adds scale, but scale does not fix weak product velocity or lost share. The combined company still has to win against Fiserv, Adyen, Stripe, Toast, Block and vertical software providers.

Synergy-quality risk: the company may hit a cost number by cutting too deeply into product, sales or service. Margin expansion would then flatter the short-term result while weakening the franchise.

Cash-conversion risk: purchase accounting and integration charges can keep the gap between adjusted earnings and cash open longer than expected.

Leverage risk: the debt load reduces room for error. A slower integration, weaker merchant volumes or higher funding costs would make the balance-sheet objective harder to reach.

Complexity risk: the company may end with a cleaner corporate perimeter but an internally fragmented collection of platforms, contracts and regional operating models.

Conclusion

Global Payments is not a clean story. That is precisely why it is interesting.

The market sees another processor buying another processor. The better interpretation is that Global Payments sold the part of the company serving issuers and concentrated the remaining portfolio around one problem: helping merchants accept payments and run commerce workflows.

The company does not need to prove everything at once. It needs to prove that the larger platform can preserve mid-single-digit growth, improve margins without damaging service, convert earnings into cash and make the product map more legible. Those are ordinary operating goals. The difficulty is achieving them inside an extraordinary integration.

Q1 says the new perimeter did not start broken. That is a low bar, but an important one. The next six quarters will show whether Worldpay becomes a wider distribution system for embedded payments and merchant software, or simply another processing estate that Global Payments has to manage.

The payments spin nobody believes in is not that the company found a new market. It is that a business known for complexity may finally have built a perimeter coherent enough to simplify.