The Quiet AI Trade

A note on long-run inflation and term premium

Affiliation Disclosure:

The managing principal of Ridire Research is affiliated with a private investment fund that holds long positions in the securities discussed herein, which could influence the views expressed.

Disclaimer:

This publication is for educational and informational purposes only. Any performance referenced is illustrative and tracked on a per-article basis, not as part of a model portfolio or investment program. Nothing herein constitutes investment advice, a recommendation, or a solicitation. → Ridire Research Substack Disclaimer

Table of Contents

Executive Summary

View

Why Look at This Now

What Long Rates Reflect

Productivity and Uncertainty

Why Short-Term Inflation Noise Matters Less

Why Duration Is the Correct Expression

Basket Expression

Optional Convexity

Why This Framework Exists

When This Would Change

Closing

Executive Summary

Markets appear to be pricing long-run inflation uncertainty and term premium too pessimistically at a time when productivity pressures, first visible in software and increasingly across services, are beginning to stabilize costs. Long-dated Treasuries are the cleanest way to express a repricing of that uncertainty, benefiting from term-premium compression even without deflation or near-term inflation relief.

View

The market may be overpricing long-run inflation and term premium in an environment where productivity is gradually improving. This note is not about near-term inflation prints or calling a macro inflection point. It’s about how long-dated assets are priced relative to plausible long-run outcomes, and whether that pricing still reflects the direction of underlying cost pressures.

Why look at this now

Inflation debates have become largely binary: either inflation is structurally higher forever, or it is about to collapse. Markets do not require that level of certainty to reprice. They move when the range of plausible outcomes narrows. What has changed recently is not inflation data, but where productivity pressure is becoming visible.

Markets have begun to recognize that AI is already pressuring software and digital services pricing. What initially looked like a margin expansion story is increasingly showing up as:

higher output per employee,

slower headcount growth,

rising competition within services categories,

and, in some cases, explicit pricing pressure.

That recognition matters because software and services have been among the most inflation-resilient parts of the economy over the past decade. Long-duration assets are especially sensitive to shifts in long-run uncertainty like this. Their pricing depends less on the next year and more on how investors assess cost stability over the next decade or two.

The question is straightforward: is the market still demanding too much compensation for long-run inflation and duration risk given these developments?

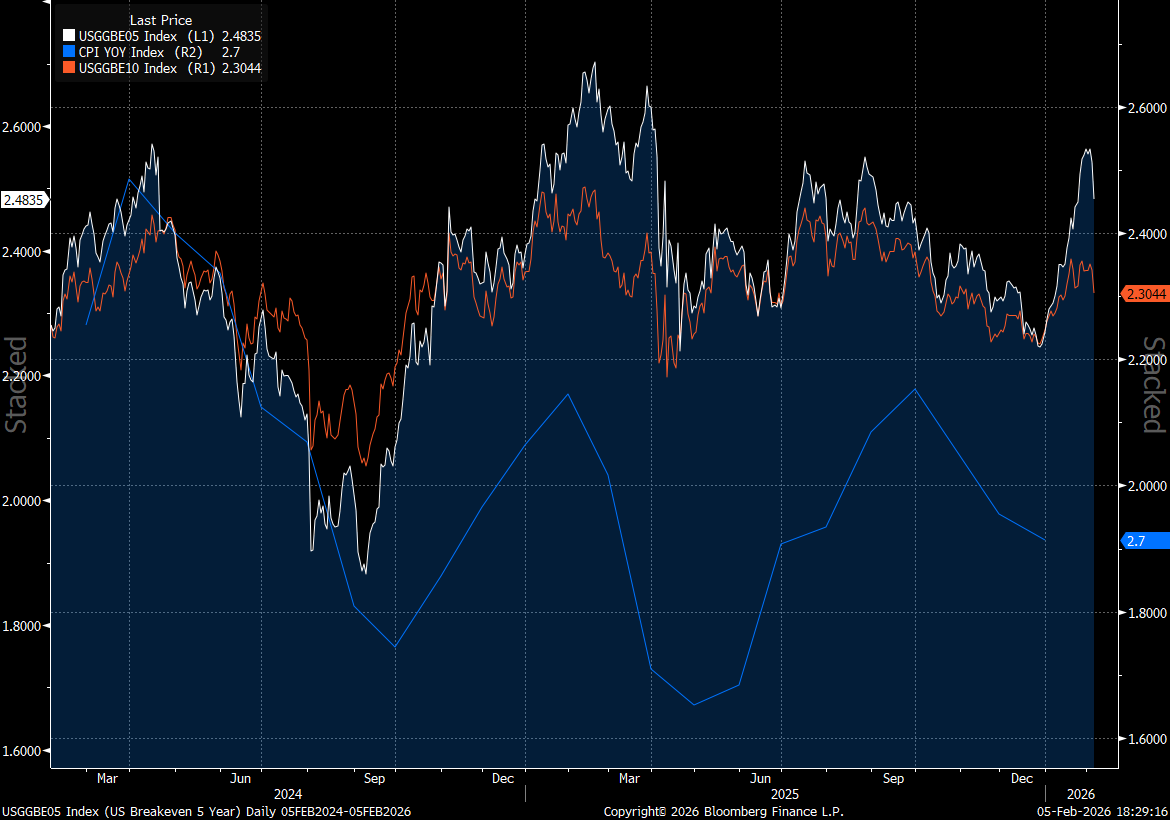

Chart 1: Long-run inflation expectations vs realized inflation (US 5y5y breakeven, 10y breakeven, and CPI YoY)

The chart below shows market-implied long-run inflation expectations alongside realized CPI. Despite large swings in headline inflation over the past two years, forward breakeven rates have remained contained, oscillating within a relatively narrow range. This matters because long-duration assets are priced off expectations about the next decade, not the last twelve months. The stability of long-run breakevens suggests that, while near-term inflation noise has been elevated, the market has not materially revised its view of long-run inflation. To the extent term premium has risen alongside nominal yields, it reflects uncertainty pricing rather than a clear shift in long-run inflation beliefs.

What long rates reflect

A long-dated Treasury yield embeds three components:

expected future short-term rates

expected long-run inflation

term premium, which compensates investors for uncertainty over time

Most macro commentary focuses on the first two. This allocation is focused on the third. Term premium tends to rise when inflation outcomes feel unstable and cost structures feel fragile. It tends to compress when investors gain confidence that the long-run environment is more predictable, even if growth is uneven.

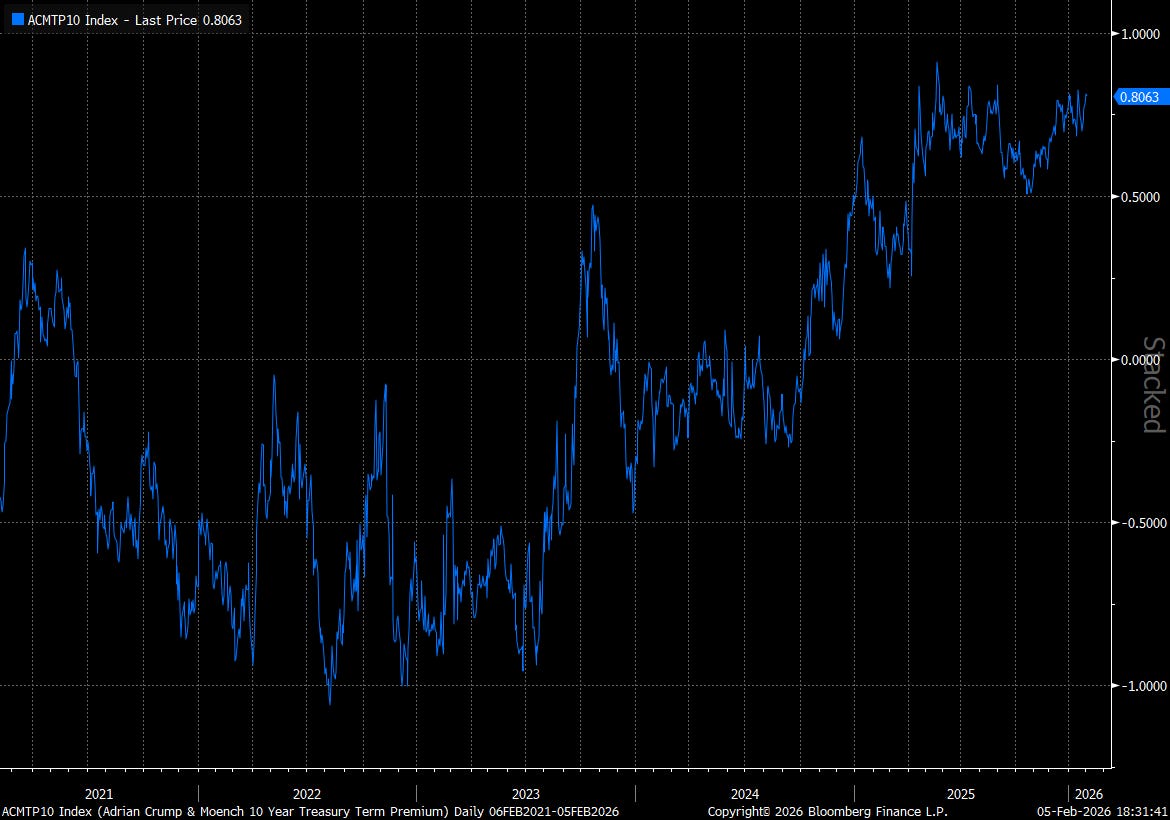

Chart 2: U.S. 10-Year Treasury Term Premium (Adrian-Crump-Moench model)

With long-run inflation expectations largely stable, elevated long-end yields increasingly reflect a higher term premium, compensation for uncertainty rather than a repricing of the inflation path.

Chart 3: U.S. 10-Year Real Yield (TIPS)

With real yields already elevated, changes in long-end pricing increasingly reflect shifts in term premium rather than expectations for stronger real growth.

The remaining question, then, is what could plausibly reduce this uncertainty over time?

Productivity and uncertainty

Productivity matters here not because it guarantees lower prices, but because it affects the stability of the system.

Incremental productivity improvements can:

reduce marginal cost pressure,

weaken pricing power over time,

limit the persistence of wage-price feedback,

narrow the range of long-run inflation outcomes.

Importantly, this process does not stop at software.

If digital services are the first place where productivity gains are visible, physical services are the logical next step as automation, robotics, and humanoid labor systems mature. Even partial substitution in labor-intensive services can materially change long-run cost dynamics without eliminating jobs outright.

None of this requires deflation. It does not require immediate or universal adoption. It requires only that the long-run cost structure of services becomes modestly easier than currently assumed. If that occurs, long-run inflation expectations and term premium can drift lower without any dramatic macro event. That is sufficient for long duration to reprice.

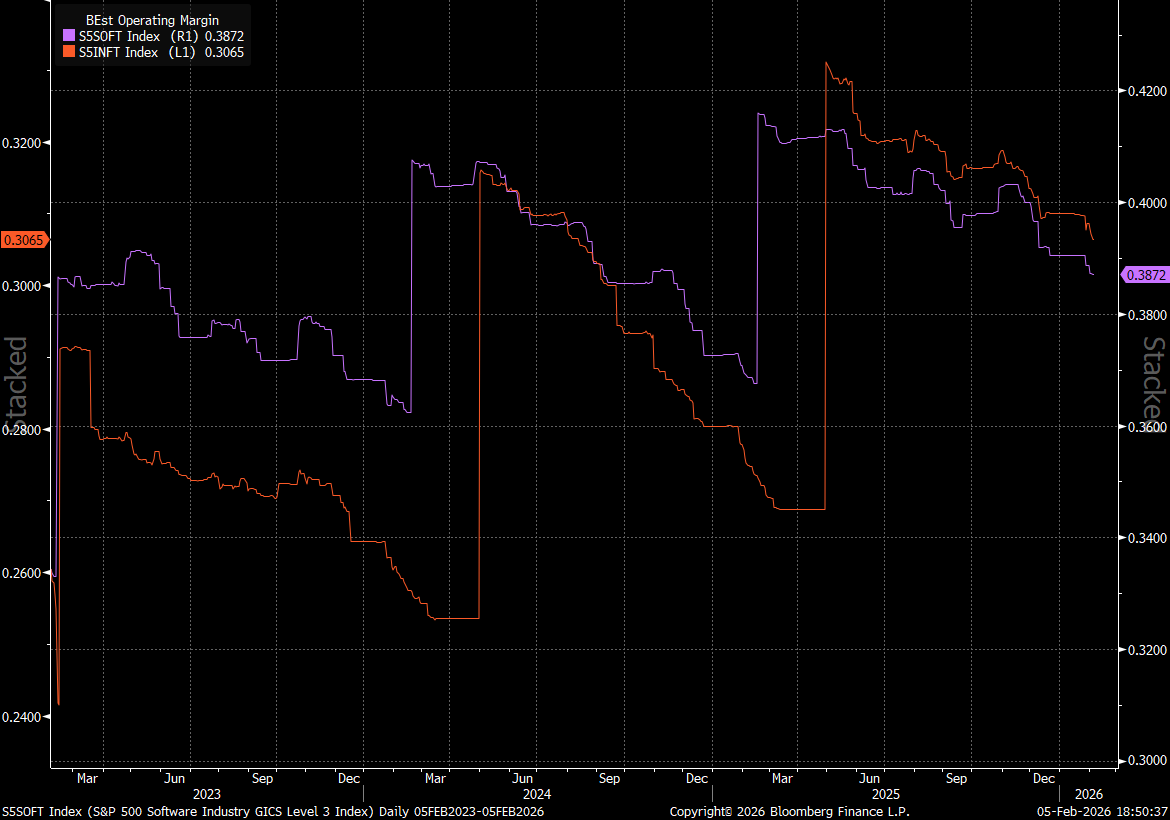

Chart 5: Software and IT Services Operating Margins (S&P 500 Software vs IT Services)

Operating margins in software and IT services have essentially stopped expanding despite continued demand. This is consistent with productivity gains translating into competitive and pricing pressure rather than sustained margin capture. Given software’s historical inflation resilience, early margin pressure here increases the likelihood that productivity effects eventually extend into broader services.

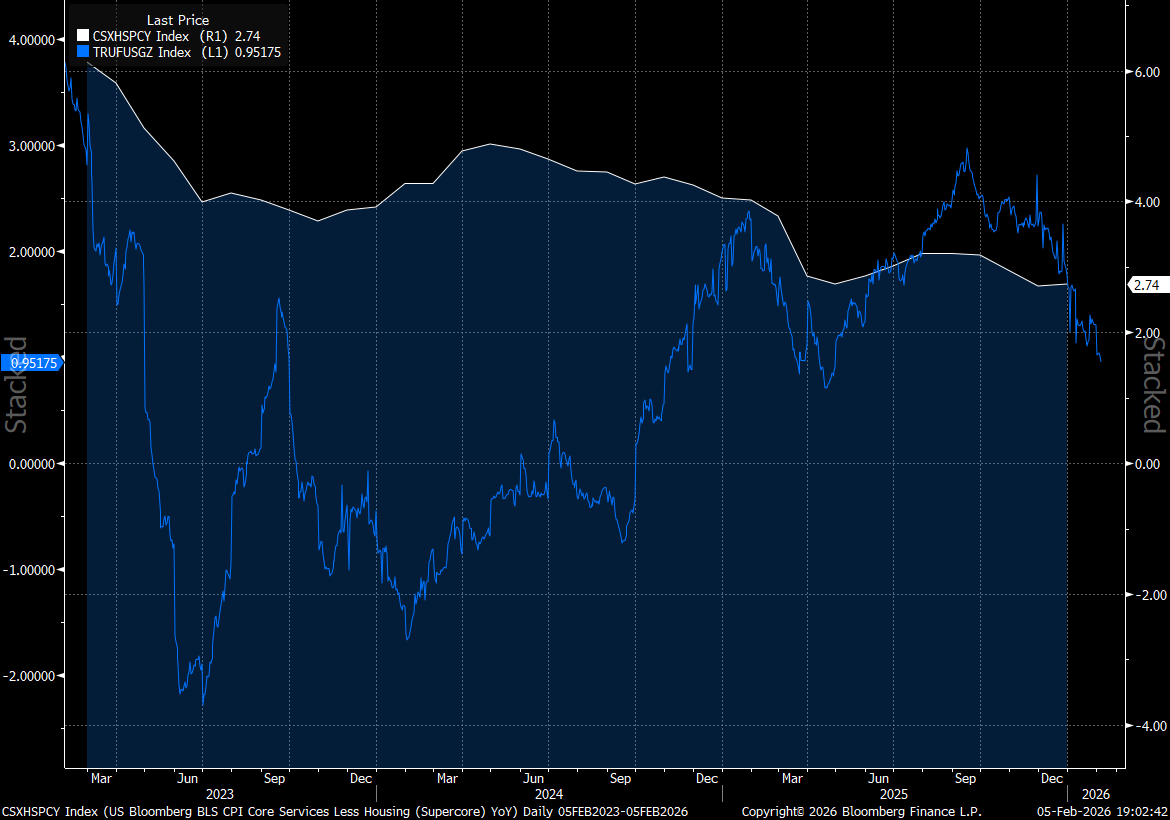

Chart 6: Services inflation: official vs real-time

The chart compares official measures of services inflation with a real-time price index. While the two series differ in construction and volatility, both suggest that services inflation has stopped accelerating. This matters because services inflation has been the most persistent component of CPI. Even modest stabilization here reduces the risk that elevated inflation persists indefinitely, supporting a narrower range of long-run inflation outcomes.

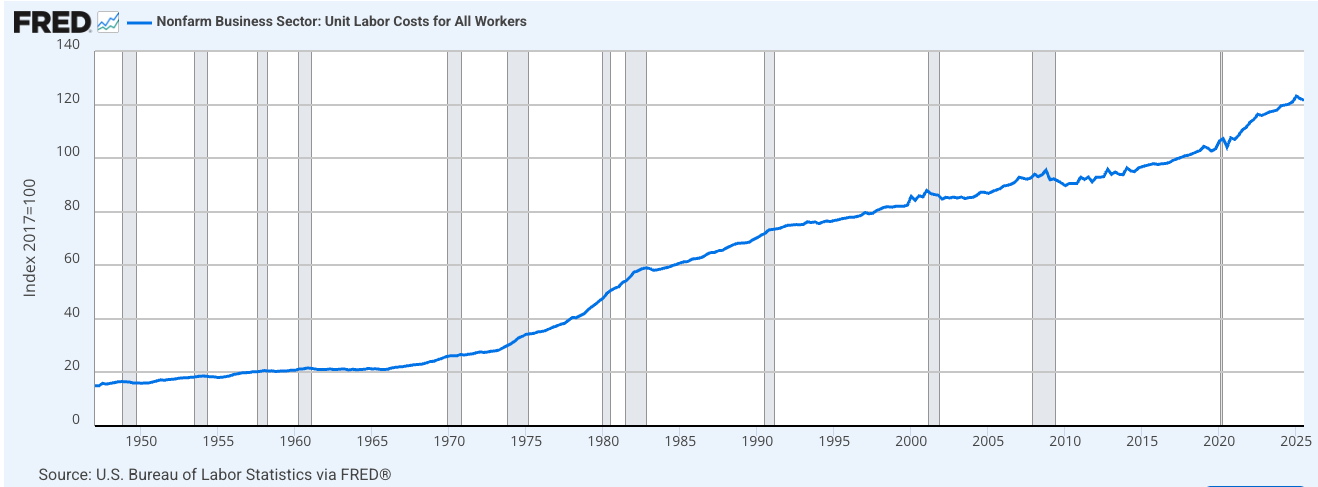

Chart 7: Unit labor costs

Despite elevated wage growth, unit labor costs have moderated as productivity improves, lowering the probability that services inflation remains structurally high.

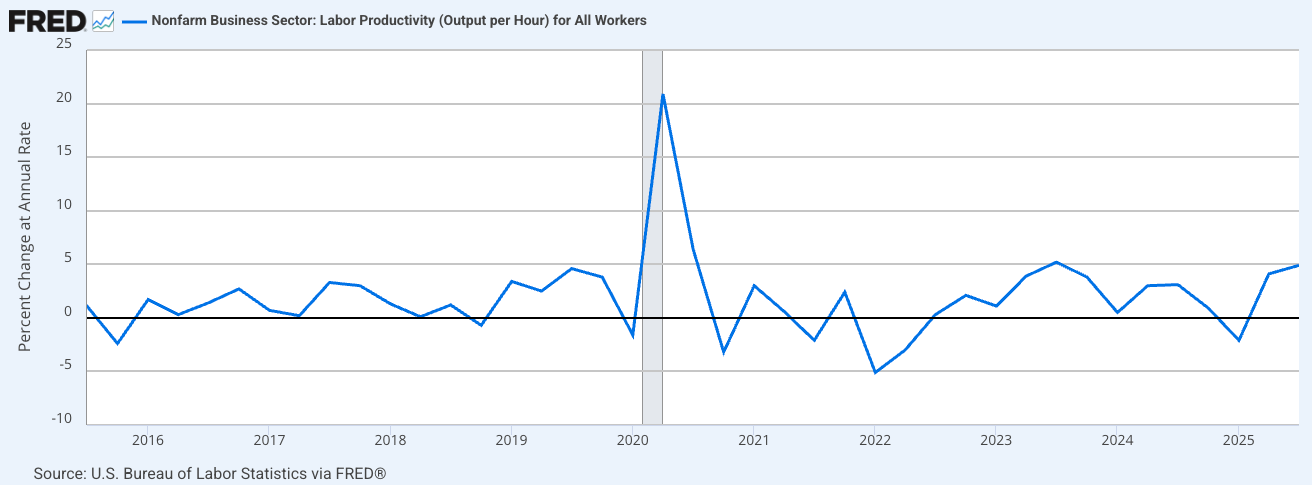

Chart 8: Labor productivity

Measured productivity growth narrows the range of plausible long-run inflation outcomes by lowering marginal costs and weakening wage–price persistence. One of the largest productivity shocks of the past decade coincided with the shift to remote work, a reminder that removing hours of low-value activity can matter more for output than most incremental technological upgrades. For long-dated assets, the level of inflation matters less than the stability of the cost structure that produces it, which is why productivity primarily acts through term-premium compression well before it appears in inflation data.

Why short-term inflation noise matters less

Near-term inflation is influenced by tariffs, supply chains, fiscal dynamics, and labor constraints, effects that are primarily reflected in short-dated rates. Long-duration assets are priced on longer horizons and respond to changes in confidence about long-run stability rather than transitory volatility. The thesis only fails if policy or structural forces permanently re-anchor long-run inflation expectations or sustain elevated term premium.

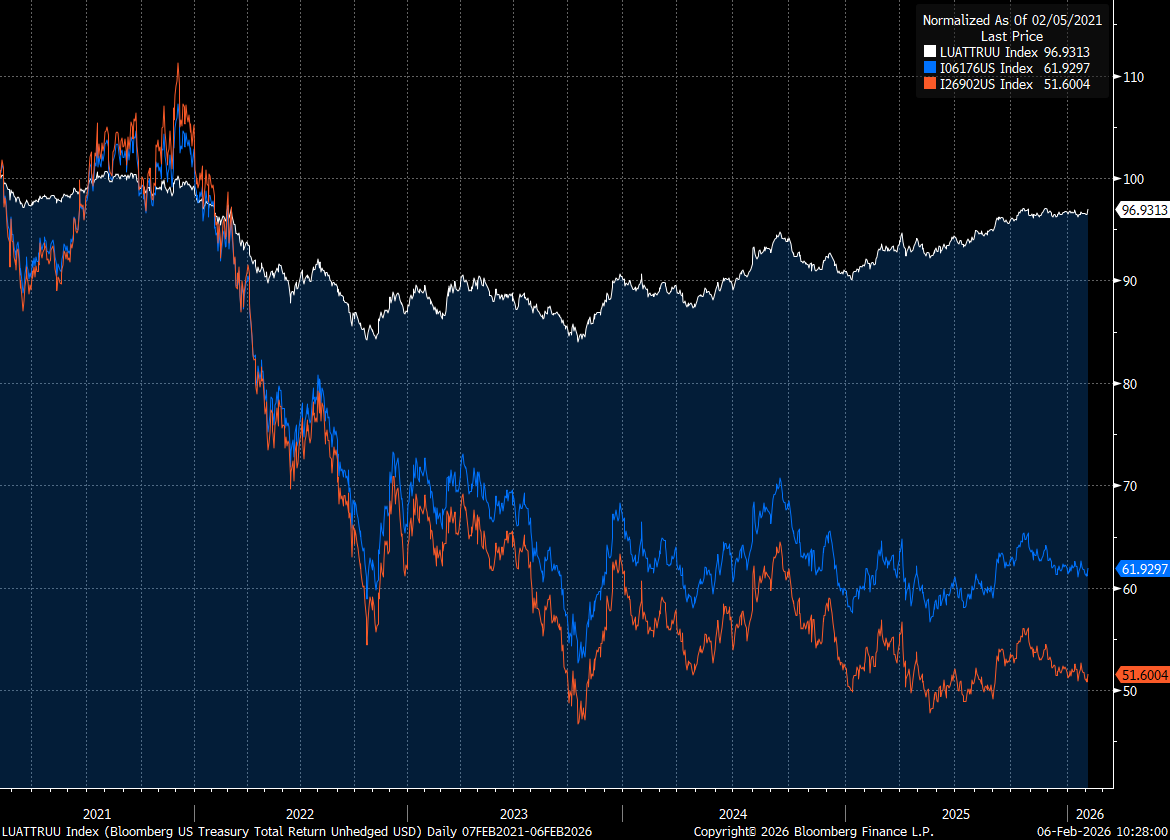

Chart 4: Treasury total return by maturity (Bloomberg US Treasury Total Return Indices)

Longer-duration Treasuries exhibit disproportionate total return sensitivity to changes in long-end pricing, making them the most direct way to express a view on term-premium compression.

Basket Expression

AI Productivity Duration Basket allocation:

TLT — 62.50%

EDV — 18.75%

ZROZ — 18.75%

TLT provides liquid exposure to long-duration Treasuries. EDV and ZROZ increase effective duration and sensitivity to changes in term premium. This allocation is intended to be held as a structural position rather than traded tactically.

Optional convexity

In addition to the structural duration sleeve, an optional options overlay could be used to introduce convexity. This overlay is focused primarily on long-dated calls on TLT, with a smaller exposure to long-dated EDV calls, and ZROZ options included only where liquidity allows and sized so a full loss would be immaterial. The purpose is to benefit from a faster-than-expected repricing of long-run inflation or term premium, while keeping downside strictly limited to the premium paid.

Why this framework exists

Long-dated rates currently embed a high degree of caution about the future. That caution may ultimately prove justified. It may also prove excessive if productivity gains continue to show up in services pricing and cost structures.

The asymmetry is the point: a modest reduction in long-run inflation uncertainty can have a meaningful impact on duration pricing, while the downside of a limited allocation remains manageable.

When this would change

This sleeve would be reduced or removed if:

long-run inflation expectations rise persistently,

term premium increases structurally due to sustained fiscal pressure,

productivity improvements fail to extend beyond narrow or isolated use cases.

Absent those developments, long duration remains a reasonable hedge against the possibility that long-run inflation risk is priced too aggressively.

Closing

This is a measured macro bet based on a simple observation: The future may be somewhat more stable, and less cost-intensive, than the market currently assumes. That alone can be enough for duration to work.

One final point, this framework is explicitly about long-run inflation uncertainty and term premium, not about near-term price levels or cyclical reflation. For that reason, several common “inflation hedges” are deliberately excluded.

Inflation-linked bonds and commodities primarily benefit from rising realized inflation, which is not the view being expressed.

Financials tend to benefit from elevated term premium and steeper curves, making them a poor fit for a compression thesis.

Traditional value exposures are similarly sensitive to inflation persistence and higher discount rates.

However, these could all still work for reasons not mentioned in the scope of this article.

Our framework is designed to benefit from uncertainty repricing rather than inflation acceleration.