The Radioactive Renaissance

Therapies, isotopes, and the infrastructure

Disclaimer:

This publication is for educational and informational purposes only. Any performance referenced is illustrative and tracked on a per-article basis, not as part of a model portfolio or investment program. Nothing herein constitutes investment advice, a recommendation, or a solicitation. → Ridire Research Substack Disclaimer

Table of Contents

Executive Summary

Key Thesis Points

Theme Basket Overview & Expression

Nuclear Medicine Overview

Casual Mechanism & Tipping Point

Competitive Advantages & Structural Edges

Ecosystem Landscape

Valuation & Implied Expectations

Capital Cycle, Policy & Capital Allocation

Key Risks

Executive Summary

Nuclear medicine, the use of radioactive isotopes for imaging and treating disease, is emerging from niche status to become a frontline modality in cancer care. Our thesis is that recent breakthroughs in radiopharmaceutical therapies and supply-chain infrastructure have brought this field to a tipping point. We identify a long basket of select radiopharmaceutical developers and “picks-and-shovels” suppliers to capture this theme’s multi-faceted upside while mitigating single-name risk.

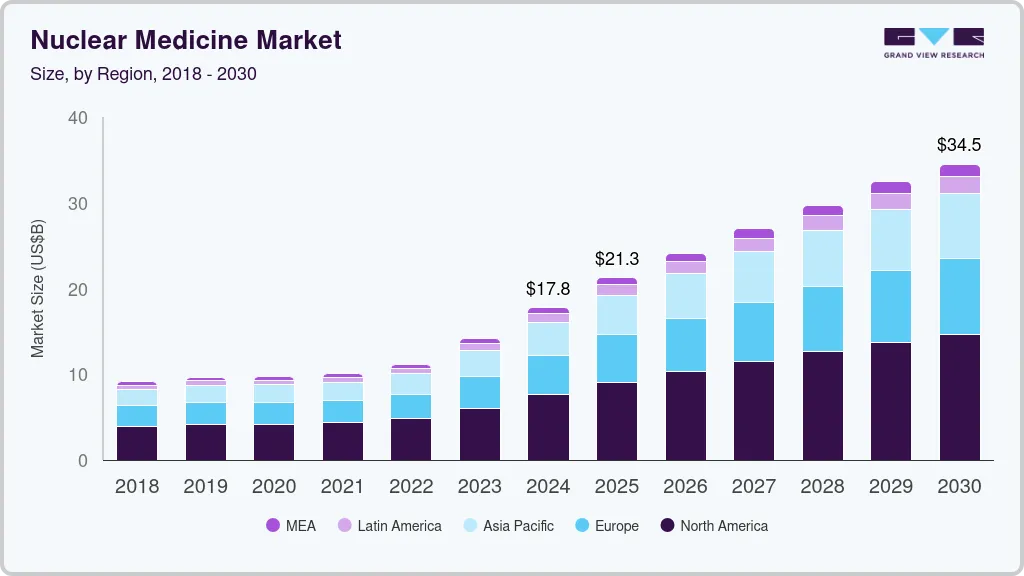

Figure 1: The global nuclear medicine market is projected to grow significantly, supporting the investment thesis that the field is at a tipping point. This growth is driven by the introduction of new therapies and expanding applications.

Key Thesis Points:

Demonstrated Efficacy: Targeted radiotherapies have shown compelling clinical results in hard-to-treat cancers (Novartis’s radioligand drugs prolong survival in neuroendocrine tumors and prostate cancer). This validates nuclear medicine as a powerful therapeutic approach.

Technology & Infrastructure Advances: Improvements in isotope production, targeting molecules, and safety protocols have lowered historical barriers. Modern “theranostic” platforms pair imaging and therapy, ensuring patients get the right isotopic treatment at the right time. Meanwhile, specialized suppliers are scaling up isotope manufacturing and distribution networks.

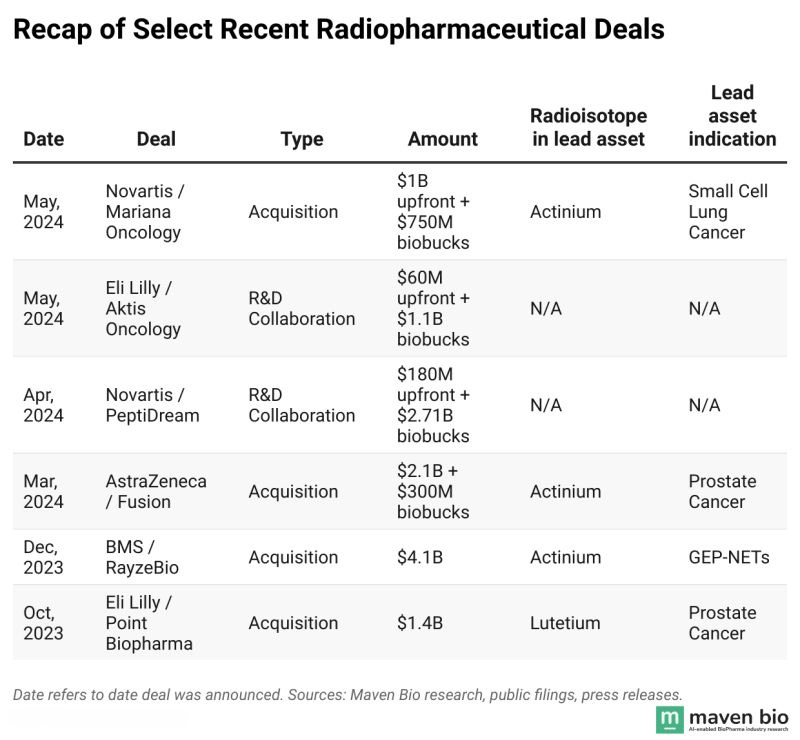

Big Pharma Endorsement: Large pharmaceutical companies are making major investments in radiopharma. Recent acquisitions (Bristol Myers buying RayzeBio, AstraZeneca acquiring Fusion Pharma, Lilly acquiring POINT Biopharma) signal a long-term commitment to build radiotherapeutics franchises, bringing deep capital and expertise into the field.

Figure 2: A wave of multi-billion dollar acquisitions by major pharmaceutical companies helps validate the long-term potential of the radiopharmaceutical sector.

Broad Optionality: Radiopharmaceuticals represent a platform, not a single drug. The same core technologies (radioisotopes + targeting ligands) can be applied across multiple cancer types and even other diseases. This gives the sector numerous “shots on goal”, success in one indication can open the door to many others, delivering outsized growth for the leaders.

Structural Tailwinds: We see a favorable capital cycle: years of underinvestment in nuclear med are reversing as demand rises. Regulatory agencies and governments are supporting domestic isotope supply and fast-tracking novel radiopharmas. This backdrop creates a supportive environment for the theme to play out over the next 3–5+ years.

Theme Basket Overview:

We express this theme with a basket of equities spanning the value chain – from drug development to isotope supply. This includes established leaders with commercial products (to provide stability and cash flow), late-stage innovators nearing the market, emerging platform players (for high-upside optionality), and infrastructure providers that profit from broader industry growth.

The basket balances current revenue generators (Novartis, Telix) with pipeline-dependent biotechs (Actinium, Clarity, Alpha Tau). It also adds lower-volatility “picks and shovels” names (BWX Technologies, Eckert & Ziegler) that benefit from rising isotope demand regardless of which drug wins. This mix is designed to capture the theme’s upside while reducing single-name binary risk.

By including both growth-oriented biotech and cash-flowing industrials, the basket is positioned to weather different market conditions. In a bull case where multiple radiotherapies succeed, the pure-play biotechs could soar. In a scenario where progress is slower, the infrastructure names and diversified pharma exposure help preserve value.

Thematic Basket Expression

We express the nuclear medicine theme through a diversified long-only basket spanning Revenue Anchors, Infrastructure (Picks & Shovels), and Pipeline Optionality. The construction is designed to capture upside across the full value chain while reducing single-asset binary risk.

Revenue Anchors — 40%

Novartis (NVS) and Telix (TLX AU / TLPPF) anchor the basket with commercial scale, proven execution, and near-term revenue visibility. These positions provide durability and ensure exposure to radiopharma adoption even if pipeline outcomes vary.

NVS — 20%

TLX AU / TLPPF — 20%

Infrastructure (Picks & Shovels) — 30%

BWX Technologies (BWXT) and Eckert & Ziegler (EUZ GY) represent the isotope supply and manufacturing backbone of nuclear medicine. These positions benefit from rising sector activity regardless of which specific therapies ultimately dominate.

BWXT — 15%

EUZ GY — 15%

Pipeline Optionality — 30%

Actinium (ATNM), Clarity (CLRPF), Perspective (CATX), and Alpha Tau (DRTS) provide asymmetric upside through differentiated radiotherapy approaches. These are intentionally sized smaller to reflect clinical and regulatory risk, with the expectation that only one or two successes are required to materially lift basket returns.

ATNM — 10%

CLRPF — 8%

CATX — 6%

DRTS — 6%

Nuclear Medicine Overview

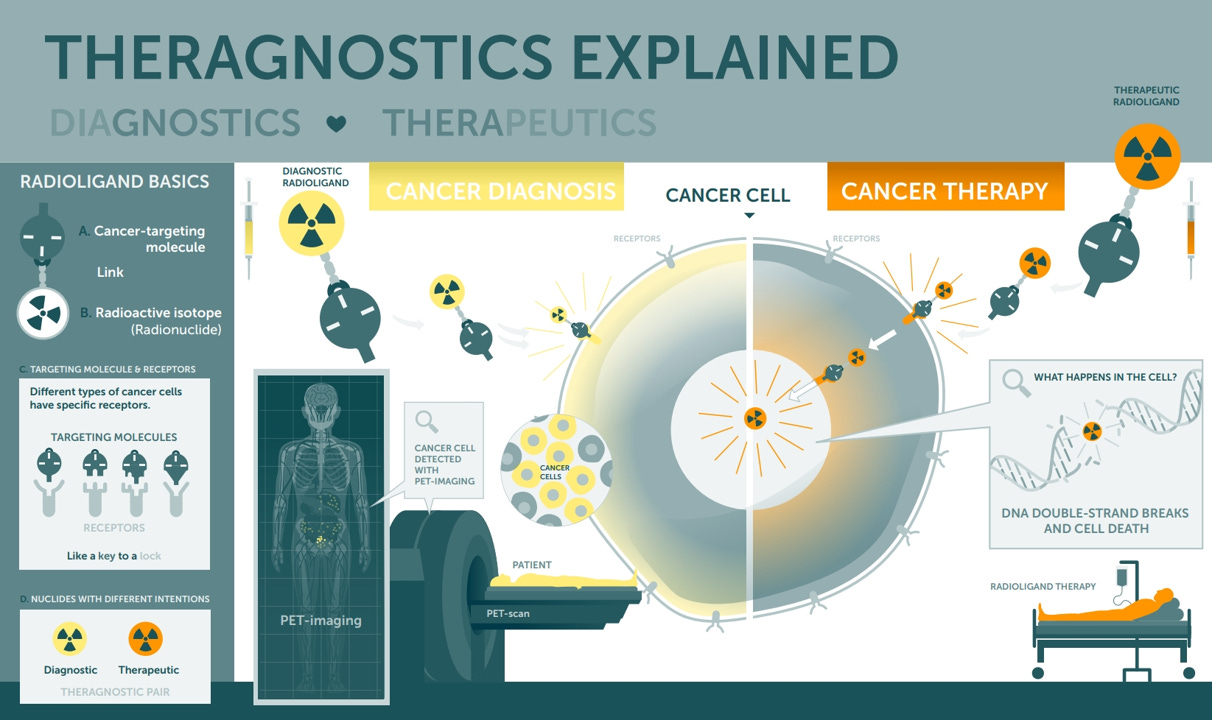

Nuclear Medicine is an interdisciplinary field at the intersection of nuclear physics and medicine, encompassing the use of radioactive isotopes for diagnosis and therapy. In practice, this ranges from imaging procedures, for example, PET and SPECT scans where radioactive tracers illuminate biological processes, to radiopharmaceutical therapies that deliver lethal radiation doses directly to disease sites. For decades, nuclear medicine was largely confined to diagnostics (think of cardiac stress tests or FDG PET scans in oncology) and a few niche treatments (like radioactive iodine for thyroid disease). Today, however, a new generation of radiopharmaceutical “theranostics”, pairings of diagnostic scans and targeted radioisotope treatments, is poised to move the field from the fringes of oncology into the mainstream.

Nuclear medicine occupies a unique niche in healthcare, sitting between traditional pharmaceuticals and the world of nuclear technology. It requires a tight integration of science and infrastructure: advanced chemistry to link radioactive atoms with targeting molecules (like antibodies or peptides), as well as specialized facilities to produce, transport, and safely administer these compounds. Historically, this complexity kept radiopharmaceuticals as a backwater in pharma – a bit too “nuclear” for biotech investors, and a bit too biotech for the nuclear industry. That is now changing. The convergence of better molecular targeting (from biotech) and improved isotope production techniques (from nuclear engineering) has created the conditions for a renaissance in nuclear medicine.

Figure 4: Theranostics allows clinicians to "see what they treat" by pairing a diagnostic agent with a therapeutic agent.

Two landmark therapies illustrate this turning point:

Lutathera (Lutetium-177 dotatate) was approved in 2018 for certain neuroendocrine tumors, becoming one of the first modern radioligand therapies to show a survival benefit in solid tumors.

Figure 5: The mechanism of PRRT, the technology behind Lutathera, which targets neuroendocrine tumors.

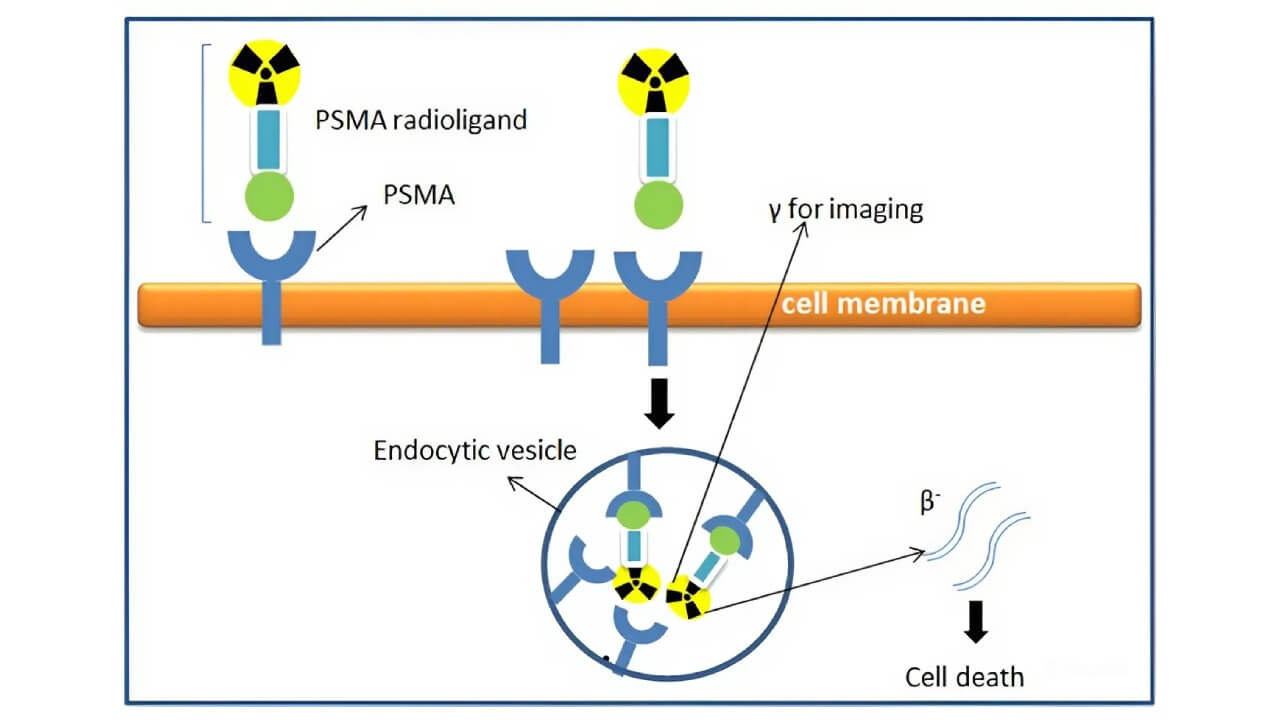

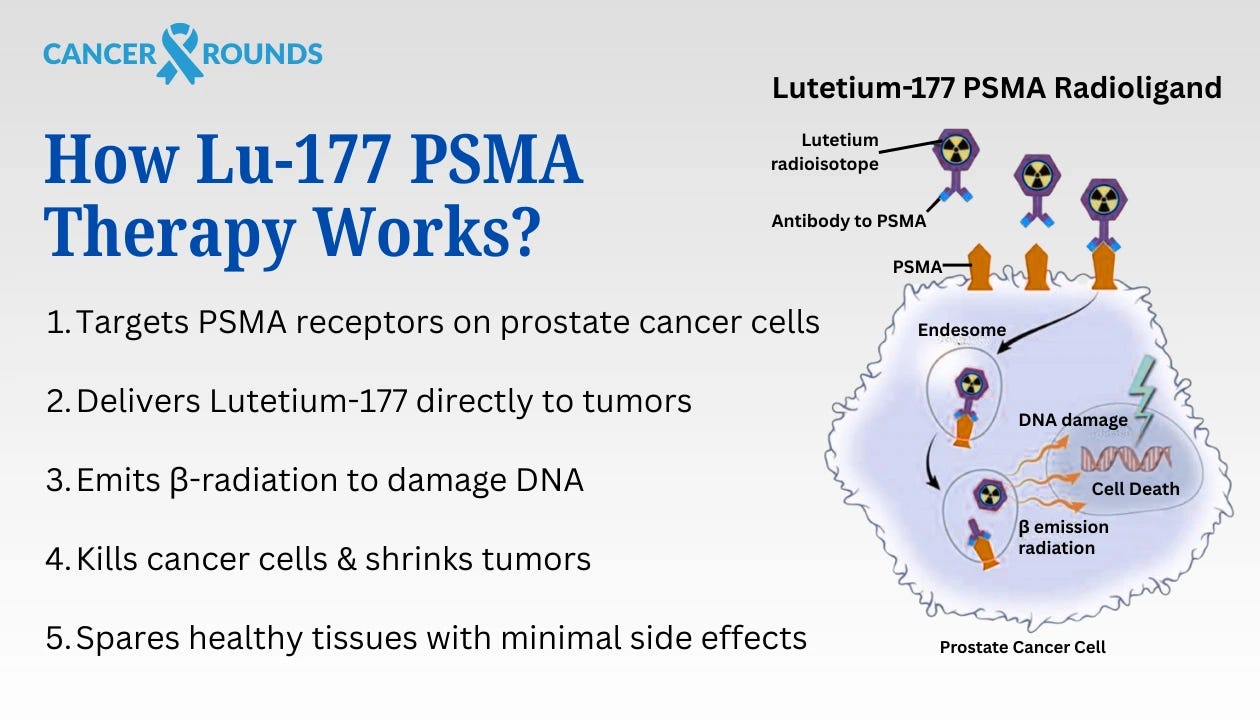

Then in 2022, Pluvicto (Lutetium-177 PSMA-617) was approved for advanced prostate cancer, after dramatically reducing tumor progression in trials.

Figure 6: The mechanism of action for PSMA-targeted radioligand therapy, where the drug binds to and is internalized by prostate cancer cells, delivering a lethal dose of radiation.

These drugs proved that by combining a radioactive payload with a targeting vehicle (such as a peptide that seeks tumor cells), one can attack cancers that are otherwise incurable, with manageable safety profiles. The success of Lutathera and Pluvicto provided a clinic-ready template for others to follow, sparking intense R&D activity and investment across the sector.

Causal Mechanism & Tipping Point

Why Now? The core mechanism driving this theme is straightforward: targeted radiotherapy works. By delivering ionizing radiation from within the body, right at the cancer cell, radiopharmaceuticals can destroy tumors that evade surgery, external radiation, or conventional drugs. The concept isn’t new, earlier attempts date back to radio-immunotherapy drugs in the early 2000s, but the tipping point came from improvements in precision and proof. Unlike older agents, today’s radiopharmas use more selective targeting ligands (for example, PSMA in prostate cancer is a highly specific marker) and often pair therapy with diagnostic scans to confirm that the drug will hone in on a patient’s tumors. This greatly increases the chances of success and builds physician confidence.

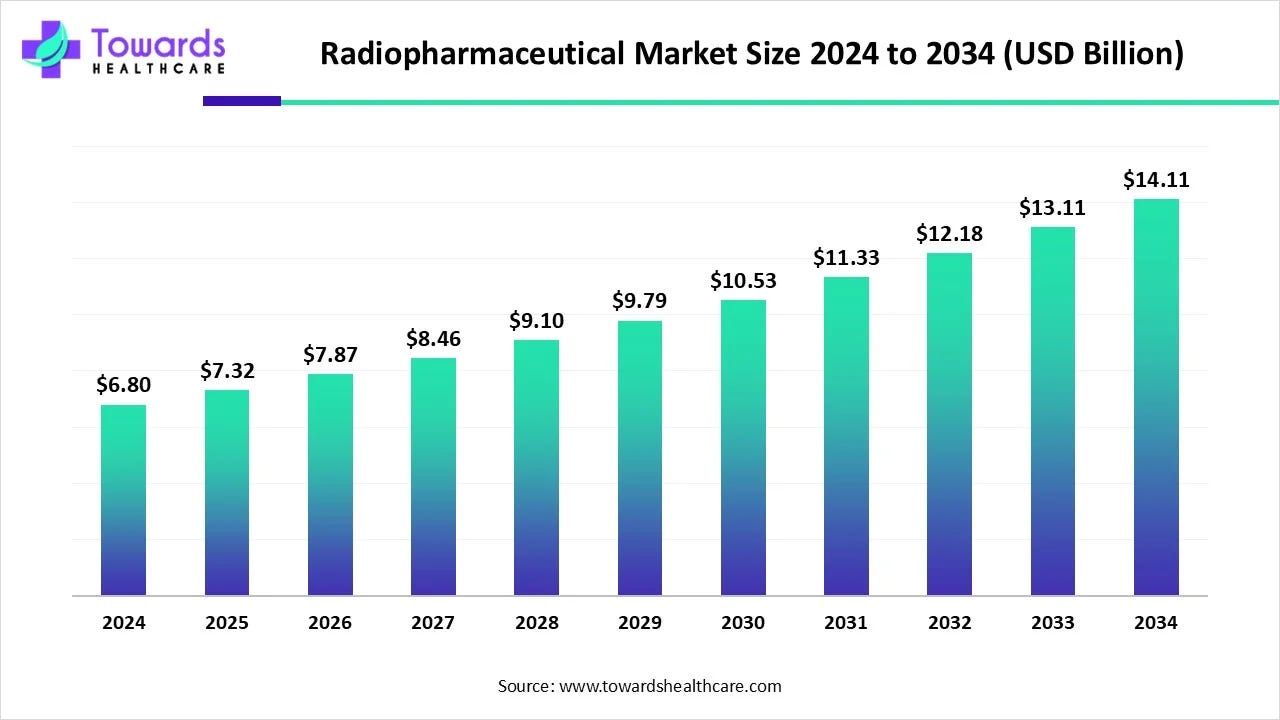

Figure 7: The radiopharmaceuticals market is forecasted to experience steady growth, driven by the clinical success of new therapies.

Several converging factors created the tipping point we’re now witnessing:

Clinical validation: The strong trial results and real-world outcomes from Lutathera and Pluvicto in the late 2010s and early 2020s gave physicians and investors tangible proof that radiopharmaceuticals can extend and improve lives. After decades of being viewed as experimental, nuclear medicine suddenly had credible champions and published data in top journals showing meaningful survival benefits. This changed the narrative from skepticism (“too toxic, too complicated”) to optimism (“a new pillar of cancer therapy”).

Supply chain maturation: A therapy is only as good as its ability to reach patients. Historically, one of nuclear medicine’s Achilles’ heels was the fragile supply chain for isotopes. Many medical isotopes are produced in only a handful of aging nuclear reactors worldwide, leading to chronic shortages (for instance, the well-known molybdenum-99 supply crises affecting diagnostic scans). However, the past few years have seen major initiatives to modernize and expand isotope production: new reactor projects and particle accelerators dedicated to medical isotopes, government funding (in the US, EU, and others) to localize supply, and companies like BWXT and Eckert & Ziegler ramping up commercial production lines. These efforts mean the infrastructure is finally catching up to the science, reducing the risk that a breakthrough drug languishes due to lack of material.

Better targeting & safety: Early radio-drugs sometimes faltered because they either hit unwanted tissues or caused collateral damage. Advances in biochemistry (e.g. more stable chelators that securely hold radioactive metals, and more specific targeting agents) have improved the therapeutic index of radiopharmas. For example, modern radioligands can target antigens almost exclusive to tumors (like PSMA or SSTR2) and clear quickly from the bloodstream, limiting radiation to just the cancer. Moreover, supportive care protocols (such as amino acid infusions to protect kidneys during Lutetium treatments) have evolved to mitigate side effects. The result is a tipping point where the benefits now clearly outweigh the risks in many indications, which was not the case 20 years ago.

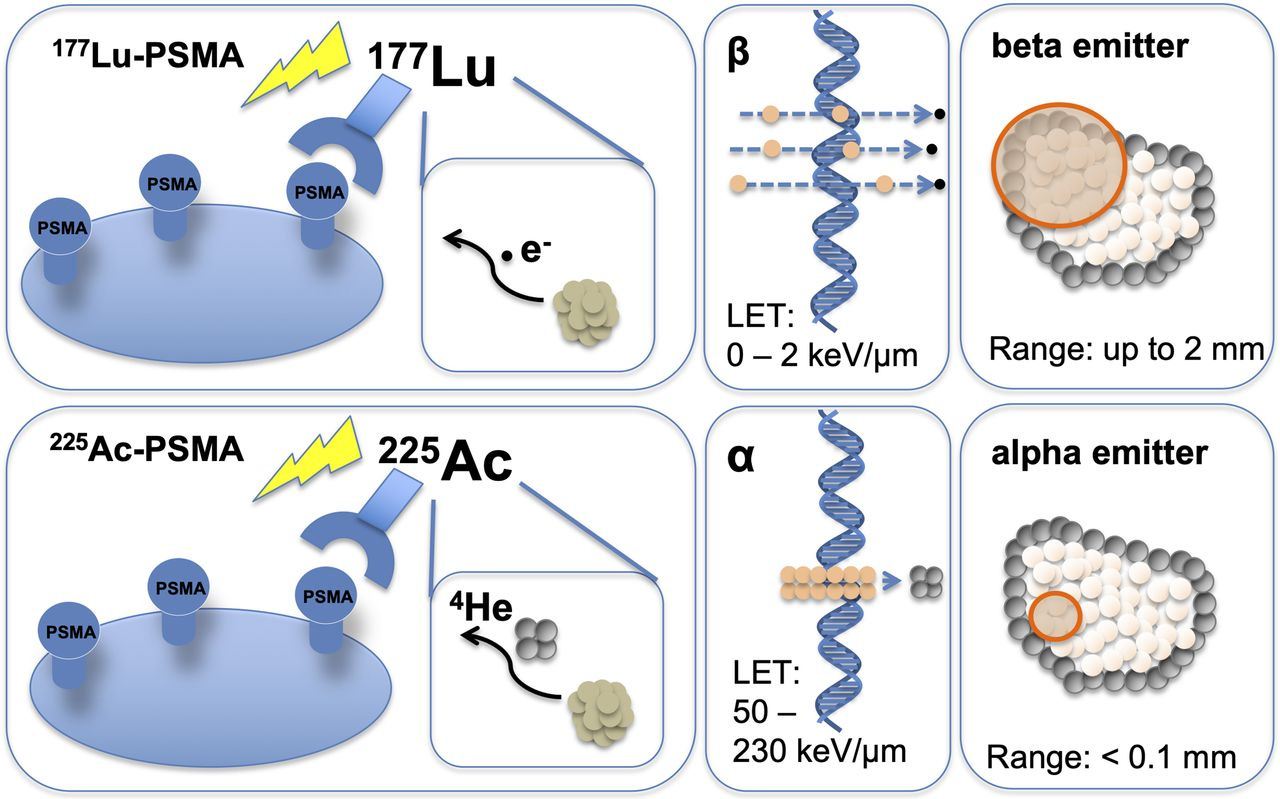

Figure 10: The development of different types of radioisotopes, such as alpha and beta emitters, provides a range of therapeutic options with distinct properties for targeting various cancers.

External pressures in oncology: It’s worth noting the broader context that oncology is hungry for new modalities. Many cancers (prostate, lung, brain metastases, etc.) still have poor outcomes in advanced stages. As immunotherapies and targeted pills plateau in some settings, doctors are looking for the next leap. Radiopharmaceuticals offer a fundamentally different mode of attack, physical cell destruction, that can complement or overcome resistance to other treatments. This has created an openness among oncologists and regulators to try novel approaches, paving the way for radiotherapeutics to get a fair shot where previously they might have been dismissed as too unorthodox.

Chain Reaction of Adoption: Success breeds success. As initial patients responded well and word spread, more clinical trials launched, drawing in more investment. We’re now seeing a classic feedback loop: positive data → more funding and partnerships → more trials → broader proof-of-concept → increased big pharma interest → even more funding.

Competitive Advantages / Structural Edges

Nuclear medicine exhibits unusually strong structural moats driven by technical complexity, regulatory friction, and supply-chain constraints. The same factors that historically limited adoption now favor incumbents that have already built the required capabilities.

High barriers to entry: Radiopharma is capital-intensive and operationally complex. Production requires radiation-safe facilities, licensed handling of isotopes, and regulatory approvals that are slow to replicate. On the supply side, companies like BWXT and Eckert & Ziegler have spent decades building nuclear and isotope expertise that newcomers cannot quickly duplicate. On the therapy side, platforms such as Telix and Actinium have accumulated proprietary know-how, chelators, targeting ligands, and manufacturing processes, that compound over time.

A hot cell facility at the Saskatchewan Centre for Cyclotron Sciences, showing the specialized radiation-safe infrastructure required for radiopharmaceutical production.

Integrated infrastructure and first-mover advantage: Early leaders were forced to integrate vertically to succeed, and that integration is now a competitive edge. Scaled manufacturing, logistics, and hospital relationships allow faster and more reliable delivery than new entrants starting from zero. First-mover adoption also creates operational stickiness: once hospitals integrate a radiopharma workflow, they are more likely to expand usage with the same suppliers.

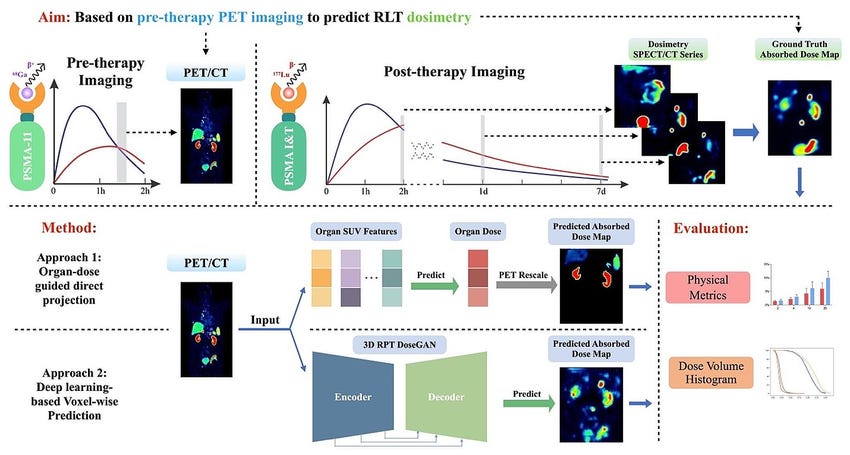

Theranostic Model – Patient Selection and Loyalty: Radiopharma companies benefit from a theranostic approach: they often develop a diagnostic scan alongside the therapeutic. This is a competitive advantage because it creates a built-in funnel for their therapy. For example, if a Telix or Clarity Pharmaceuticals provides an imaging agent that identifies patients with a certain tumor target, those patients (and their doctors) are naturally led to consider the corresponding therapy from the same company. It’s a seamless pipeline from diagnosis to treatment that competitors without a paired diagnostic can’t easily replicate. This model also potentially speeds adoption – by demonstrating with a scan that a patient’s cancer is lighting up (i.e. has the target), you give physicians confidence that treating with the radiopharmaceutical will be worthwhile. As a result, companies following this theranostic playbook can gain physician mindshare and patient loyalty that others might struggle to chip away.

A detailed workflow diagram showing the theranostic approach from pre-therapy imaging through post-therapy imaging and treatment.

Concentrated supply and sticky relationships: Key isotopes are produced by a small number of qualified facilities, creating de-facto oligopolies. Switching suppliers is non-trivial due to quality control, regulatory re-validation, and logistics. Once long-term supply contracts are in place, they tend to be durable, supporting pricing power and stable demand for infrastructure providers.

Convexity through M&A interest: One could argue another “advantage” for investors in this space is the heightened probability of takeover at premium valuations. Big Pharma’s growing interest means each successful smaller player has multiple suitors. This isn’t a traditional competitive advantage in product terms, but it is a structural feature of the industry now: if a small cap radiopharma shows positive phase 2 data, the odds are higher than in many biotech sub-fields that it gets snapped up (given the current arms race for radiotherapy pipelines). For our theme, this dynamic provides upside optionality, even if a company might not succeed as a standalone long-term, investors could benefit from a buyout at a rewarding price.

In summary, nuclear medicine rewards companies that solve the hard problems: isotope access, manufacturing, logistics, and workflow integration. These structural edges favor entrenched platforms and infrastructure providers, aligning with a basket approach that owns both the therapies and the system that makes them scalable.

Ecosystem Landscape

The nuclear medicine ecosystem has matured into a vertically interdependent value chain, spanning large pharmaceutical platforms, specialist radiopharma developers, and a constrained isotope supply base. Our basket is constructed to capture value at each layer.

Large Pharma Anchor

Novartis (NVS). Novartis remains the category leader and reference point for radioligand therapy. It was the first large pharmaceutical company to build an integrated radiopharma franchise, combining drug assets with global manufacturing and distribution. Its continued investment and commercialization establish radiopharma as a durable therapeutic category rather than an experimental niche. Novartis serves as both a stabilizing anchor and a benchmark for what scaled success looks like in the sector.

Specialist Radiopharma Biotechs:

Telix Pharmaceuticals (TLX.AX) – A global leader among pure-plays, Telix already commercialized an imaging agent (Illuccix for prostate cancer PET scans) and is advancing a broad pipeline of therapeutic candidates (targeting renal cancer, brain cancer, etc.). Telix’s success with Illuccix (achieved significant sales within its first year of launch) underscores its strong execution ability. It’s carving out a role as a full-spectrum radiopharma company (diagnostics + therapeutics), somewhat akin to a mini-AAA/Novartis but independent. We consider Telix a bellwether for investor sentiment in this sector – and a potential mid-term acquisition target for a larger pharma given its head start.

Actinium Pharmaceuticals (ATNM) – A US-based biotech focusing on alpha and beta emitting therapies for hematologic cancers. Its lead program, Iomab-B (using radioiodine to condition bone marrow prior to transplant in leukemia patients), has completed Phase 3 with positive results. Actinium also has collaborations to use Actinium-225 labeled antibodies in combination with other drugs for leukemia. If approved, Iomab-B would open a new niche (radiation conditioning for bone marrow transplant) with little competition, effectively creating a new market category. Actinium’s expertise in antibody radioconjugates gives it a platform it can potentially extend to other blood cancers or even solid tumors. We include it for its late-stage status and unique focus – though we acknowledge regulatory uncertainty around the approval path is a current overhang.

Clarity Pharmaceuticals (CLRPF) – An emerging platform out of Australia, Clarity is championing copper-based radiopharmaceuticals (Copper-64 for imaging, Copper-67 for therapy). The idea is that copper isotopes have ideal properties for theranostics (Cu-64’s half-life allows centralized manufacture and distribution to imaging sites, and Cu-67 can be produced without a reactor, theoretically easing supply issues). Clarity has multiple drugs in early clinical development, including targets in prostate cancer and neuroblastoma. We include Clarity as a representative of the “next wave” of platform biotechs, it offers exposure to potentially more scalable technology (if copper can be produced via cyclotrons, that’s a game-changer for supply) and has attracted partnerships and government support. It’s still in trials, so it’s a higher-risk, higher-reward piece of the basket.

Perspective Therapeutics (CATX) – Formed via the merger of Isoray and Viewpoint Molecular Targeting, Perspective combines a legacy brachytherapy business (Cesium-131 implants for treating prostate cancer, which Isoray had sold for years) with new targeted alpha therapies from Viewpoint. Their pipeline includes lead-212 conjugated molecules (Lead-212 is an alpha emitter) for cancers such as melanoma and neuroendocrine tumors. Perspective brings an interesting angle: they have experience in localized radiation (brachytherapy) and are now translating that into systemic targeted therapy. With isotopes like lead-212, they can create tumor-seeking radiopharmaceuticals. This company is early-stage, but it’s a play on alpha-particle therapy, an area that could leapfrog beta emitters in potency if challenges are solved. We include CATX for diversification into alpha therapeutics and to capture upside from any progress in their novel pipeline.

Alpha Tau Medical (DRTS) – A bit different from others, Alpha Tau’s approach (Alpha DaRT) straddles the line between device and drug. They insert tiny seeds imbued with Radium-224 directly into tumors, which then emit alpha particles that kill the tumor from within over a few weeks. It’s a localized therapy (unlike the systemic injections of other radiopharmas) and is being tested in indications like skin cancers, breast tumors, and glioblastoma. Alpha Tau’s technology showed promising early results in a pilot skin cancer study. If it proves out in larger trials, it could become a new modality for solid tumors that can be accessed by a needle or minor surgery. We added Alpha Tau to the basket to reflect the diversity of approaches in nuclear medicine – it’s a more targeted “procedure-based” therapy that could complement systemic radioligands. It also exemplifies how the nuclear medicine toolbox is expanding (not just injections, but implants too). The company has risk (still in mid-stage trials, and adoption would require training surgeons/radiation oncologists on a new technique), but its upside is high as a potential disrupter of certain surgical or external radiation procedures.

There are other specialist radiopharma companies outside our basket for various reasons, for instance, Lantheus (LNTH) which is a commercial leader in diagnostics (they market Pylarify, an F-18 PET agent for prostate cancer). We chose not to include Lantheus mainly because its radiotherapeutic exposure is indirect (though it has licensed rights to some of POINT’s therapeutic candidates, Lantheus is still primarily an imaging and contrast agent company, and its valuation already reflects the huge success of Pylarify). Similarly, smaller biotechs exist but are either not easily investable for generalists or too early-stage to fit this memo. Our basket focuses on a representative set that covers both the current leaders and the promising newcomers in a balanced way.

Infrastructure & Isotope Supply

BWX Technologies (BWXT) – A U.S. company with a long history in nuclear reactors (for submarines, power, etc.), BWXT has a growing medical segment. They are working on producing Molybdenum-99 (the source of Technetium-99m, used in millions of scans annually) using innovative reactor technology that doesn’t rely on weapons-grade uranium, a significant advancement in securing domestic supply. They also have initiatives for manufacturing Actinium-225 at scale in partnership with national labs, and are involved in producing other isotopes like Yttrium-90 and Strontium-89. BWXT’s advantage is it has the engineering muscle and capital to build complex facilities, something few pure biotechs can do. It also generates steady revenue from its core defense contracts, giving it financial stability. In our theme, BWXT represents the “macro” infrastructure bet, if nuclear medicine demand skyrockets, BWXT will likely see large, long-term contracts and government support to produce isotopes, boosting its medical segment earnings.

BWXT Medical's Tc-99m generator facility.

Eckert & Ziegler (EZJ.DE) – A German company that has quietly become a global leader in radioisotope products and services. E&Z provides everything from radioactive source materials (Germanium-68 generators for Gallium-68 production, Cobalt sources for industrial and medical use, etc.) to contract development and manufacturing (CDMO) services specifically for radiopharmaceuticals. For example, if a biotech needs to build a production line for a Lu-177 drug, they might partner with E&Z to design and supply the hot cells and handling systems, or even have E&Z produce it for them. E&Z also produces small quantities of high-purity isotopes for trials. Essentially, it’s the one-stop shop for any company entering nuclear medicine that doesn’t have in-house manufacturing – a picks-and-shovels pure-play. We include E&Z in the basket because its profits rise with the entire sector: as more radiopharma trials commence and products commercialize, E&Z sees increased orders, service contracts, and sales of generators and equipment. It’s more Europe-focused (which is where a lot of isotope R&D happens), nicely complementing BWXT’s North American emphasis.

Eckert & Ziegler's radionuclide production equipment.

Healthcare Providers and Distributors: Another part of the ecosystem (not in our basket, but worth noting) are the nuclear pharmacies and hospital networks. In the US, companies like Cardinal Health and GE HealthCare’s pharmacy network are crucial for last-mile delivery – they take isotopes from producers and compound patient-ready doses daily. While we haven’t included these as positions (Cardinal is a broad healthcare company, GEHC is large imaging modality player), their role indicates that distribution channels are in place. It means scaling a new drug might be easier now because these networks can be tapped rather than built from scratch. Additionally, large hospital systems are investing in theranostic centers (for instance, some academic centers have opened dedicated radioligand therapy clinics). This increasing provider-side investment is a positive sign for the ecosystem’s maturity.

Competition and Landscape Summary:

Novartis competes mainly with itself (it set the bar).

Telix competes with Lantheus in imaging and will compete with big pharma radioligand programs in therapy (Novartis, Lilly’s POINT programs) but has a broad pipeline to differentiate.

Actinium is fairly unique in bone marrow conditioning; its other programs (like CD33 targeting in leukemia) compete conceptually with CAR-T or antibody therapies for leukemia, not with another radiopharma per se.

Clarity will inevitably compete with whoever is in the same indication (if their copper prostate therapy advances, it would compete vs Novartis’s Pluvicto and Lilly/POINT’s candidate). But Clarity’s bet is that a different isotope and improved targeting can carve a niche or even surpass incumbents.

Perspective and Alpha Tau are in early stages where the “competition” is more status quo treatments (standard brachytherapy or surgery) rather than another similar company.

BWXT’s competition is limited (mostly government-run reactors or a couple of smaller firms like Nordion in Canada or NorthStar in the US).

Eckert & Ziegler similarly is one of few in its space; other players include ITM (a private German company focusing on Lutetium supply and therapies) and maybe Cardinal’s radiopharmacy division in the US. But E&Z has international reach and deep expertise that give it a solid position.

One can see that collaboration is as prevalent as competition, many of these companies will likely partner (a biotech partnering with BWXT for supply, or a big pharma licensing a smaller company’s compound). Our basket essentially picks those we think have strong individual prospects and also strategic value to others in the ecosystem.

Valuation & Implied Expectations

Traditional valuation frameworks are poorly suited to nuclear medicine. Instead of focusing on multiples, the relevant question is whether market expectations for the modality and its infrastructure are too low relative to the likely scale of adoption.

Large Pharma (NVS): Radioligand therapy is still treated as a non-core option within a diversified pharma model. Expectations appear conservative, shaped more by manufacturing constraints than demand. Upside comes from indication expansion and scale, which would reframe radiopharma as a durable growth engine rather than a niche line item.

Pure-Play Leaders (TLX): The market prices in at least one successful therapeutic transition beyond diagnostics, but does not fully price the platform nature of theranostics. Success in a single additional program could materially re-rate expectations; success across multiple programs would reframe the company entirely.

Late-Stage / Platform Biotech (ATNM): Market expectations are low, reflecting regulatory uncertainty and narrow initial indications. This creates asymmetry: approval or partnership would force a rapid re-underwriting, while failure is partially mitigated by diversified basket exposure.

Early Platforms (CATX, DRTS): Valuations imply a low probability of success. The market assumes most early programs fail. The basket thesis does not require broad success, one meaningful clinical win is sufficient to justify inclusion.

Infrastructure (BWXT, EUZ GY): These names are valued as steady industrial or nuclear businesses, with medical isotopes treated as incremental. If radiopharma activity accelerates, medical exposure could drive earnings surprises and multiple expansion not currently reflected.

Capital Cycle, Policy & Capital Allocation

Early speculative funding enabled proof-of-concept and late-stage trials. The current phase is dominated by strategic capital (large pharma M&A, partnerships, and long-term manufacturing investment), which is stickier and less cyclical.

Capital is being allocated toward manufacturing capacity, isotope access, and platform build-out, not just clinical experimentation. This signals confidence in durability rather than short-term option value.

Governments view medical isotopes as strategic infrastructure. Funding, regulatory alignment, and reimbursement frameworks have reduced non-scientific friction to adoption. This lowers the risk that effective therapies fail due to logistics or payment issues.

Overfunding and thematic crowding remain possible, but leaders with scale, differentiated technology, or infrastructure positioning are more likely to consolidate rather than be displaced.

Key Risks

Isotope Supply Crunch: If the ramp-up in isotope production does not keep pace with demand, the growth of radiotherapies will hit a hard ceiling. Many radiopharmaceuticals use exotic isotopes that are currently produced in gram or millicurie quantities worldwide. For example, Actinium-225 (an alpha emitter powering several next-gen therapies) is in extremely short supply, global production can meet only a fraction of potential patient demand. Efforts are underway to scale production (new reactors, particle accelerators, even projects to extract Actinium from Thorium stockpiles), but success is not guaranteed. Any setback, a reactor project running years late, technical difficulties in isotope extraction, or geopolitical issues (some isotopes come from reactors in Russia or Europe that could face disruptions), could leave eager patients and drug developers empty-handed. This would significantly slow adoption and could cause investors to lose faith if revenue ramps are bottlenecked by supply constraints rather than science.

Logistical and Clinical Adoption Barriers: Even with supply in hand, operational logistics pose a risk. Radiopharmaceuticals have very short half-lives (hours to days), meaning the whole chain from production to patient is time-sensitive. Hospitals need special facilities (hot labs, radiation shielding, trained nuclear medicine physicians) to receive and administer these drugs. In areas without established nuclear medicine departments, adoption might lag simply due to infrastructure. Training and staffing are another issue, nuclear medicine specialists are not as common as, say, medical oncologists or surgeons. If healthcare systems are slow to invest in the necessary facilities or if there is resistance among physicians (some oncologists might be unfamiliar or uncomfortable with radiopharma initially), the rollout of new therapies could be slower than forecast. Essentially, the risk is delivery: many patients might benefit, but getting the product to them reliably is non-trivial. This could translate into lower sales than expected for novel drugs in their first few years, disappointing the market.

Emerging Competing Therapies: The oncology landscape is highly competitive and dynamic. A risk to radiopharma is that some of the same targets being pursued (PSMA for prostate, somatostatin receptors for neuroendocrine tumors, etc.) are also being targeted by other therapeutic modalities. For instance, there are antibody-drug conjugates (ADCs) and bispecific antibodies in development for prostate cancer that target PSMA as well, these deliver a toxin or engage the immune system to kill tumor cells, rather than radiation. It’s possible that one of these approaches yields similar efficacy without the complexity of handling radioactivity. If an easier-to-administer, equally effective therapy emerges for the same patient population, it could cap the market for the radiopharmaceutical alternative. Additionally, conventional external beam radiation technology isn’t standing still, new techniques like proton therapy or targeted intraoperative radiation could address some tumors that radiopharmaceuticals target. While we believe radiopharma will often combine well with other treatments (not just compete), it’s a risk that, in some cases, it may lose out to a more convenient competitor.

Figure 12: While radiopharmaceuticals show great promise, they must compete with existing treatment modalities on both efficacy and safety.

Regulatory and Perception Risks: Using radioactive materials in medicine naturally attracts regulatory scrutiny. Radiopharma trials have to navigate not just the FDA’s usual hurdles for drugs, but also radiation safety regulations from nuclear agencies. A risk factor is that regulatory requirements could become onerous, for example, requiring additional long-term safety monitoring or complex handling protocols that slow down trials and approvals. Furthermore, any safety scare could taint public and physician perception. If, hypothetically, a late-stage trial of a radiotherapy revealed an unexpected side effect (say, higher rates of secondary cancers years later, or severe organ toxicity in some patients), it could cast a pall over the whole field. Because radiation fears have a visceral element (the word “nuclear” can alarm people), a single high-profile incident might have outsized impact on sentiment. It’s worth noting that one of the companies in our basket, Actinium Pharmaceuticals, encountered an FDA request for more evidence of survival benefit despite meeting its trial endpoints – highlighting that regulators are cautious and want clear proof that benefits outweigh risks. Such hurdles could delay approvals or require costly additional studies.

Financing & Execution Challenges for Smaller Players: The innovative biotechs driving this theme (aside from the big pharmaceutical anchors) are mostly pre-profit companies that rely on investor funding or partnerships. If the biotech funding environment deteriorates (for instance, due to rising interest rates or a broad risk-off sentiment), these companies might struggle to raise the capital needed for Phase 3 trials, manufacturing build-out, or commercialization. A prolonged capital winter could force dilutive financings or even shelve certain programs, stunting the theme’s progress. Additionally, executing in this field is harder than in traditional biotech – it’s a marriage of pharma and nuclear engineering. There could be unexpected setbacks in scaling production or in quality control (e.g., a manufacturing batch failing to meet purity standards could halt a trial). Companies might find it challenging to recruit enough specialized talent (radiochemists, medical physicists) to support their programs as they grow. In short, the road from promising Phase 1 data to a marketed product is long and fraught with operational hurdles; not all current players will make it to the finish line. For our basket, that’s why diversification is key – but it’s a risk that a couple of the smaller names could falter or even fail along the way, which would hurt the basket’s overall performance if not offset by others succeeding.

Macro and Geopolitical Risks: Given the global nature of the supply chain (isotopes, equipment, and even patients for trials often cross borders), broader macro risks apply. Trade restrictions or geopolitical tensions could impact isotope supply (for example, some isotopes come from Russia or require Russian enrichment services; sanctions or conflict could cut that off). Currency fluctuations and inflation can affect the cost of building new production facilities or running trials across multiple countries. While these are not core to the thesis, they could create headwinds or volatility in timelines and costs.