The Stock the AI Tourists Won’t Find

AI investors are chasing chips. Healthcare investors are chasing drugs. This company sells the overlooked materials and tools underneath both.

Affiliation Disclosure & Disclaimer:

The managing principal of Ridire Research is affiliated with a private investment fund that holds long positions in the securities discussed herein (Daicel Corporation, 4202 JP), which could influence the views expressed. This publication is for educational and informational purposes only. Any performance referenced is illustrative and tracked on a per-article basis, not as part of a model portfolio or investment program. Nothing herein constitutes investment advice, a recommendation, or a solicitation. → Ridire Research Substack Disclaimer

Table of Contents

Executive Summary

Company Overview

The Setup

Causal Mechanism

Timeline

Key Risks

Conclusion

Executive Summary

Daicel (4202 JP) is a cheap Japanese chemicals platform where the market is fixated on cyclical earnings, while the product portfolio quietly carries real exposure to two structurally well-funded demand pools: health-science tooling and AI-linked semiconductor / server content.

Daicel is interesting precisely because it does not look like an AI or healthcare stock on first pass. It screens as a mature chemicals name: low multiple, respectable dividend yield, low price-to-book, and earnings pressure concentrated in legacy segments. That surface-level read is directionally correct, but incomplete.

The portfolio underneath includes chiral columns and separation services used by pharmaceutical customers; health ingredients and a needle-free delivery device on the medical side; and photoresist polymers, electronic solvents, cycloaliphatic epoxies, and LCP content tied to semiconductor manufacturing and AI server hardware on the technology side.

The important nuance is that this is not a “pure-play theme stock” hiding in Japan rather it is a misclassified platform. Engineering Plastics, Materials, and Safety still anchor the P&L; which is why the market continues to underwrite the company on cyclical chemicals logic. Yet that same legacy base funds the optionality. If investors begin to value Daicel as a portfolio with a higher-quality mix, rather than as a homogenous commodity-chemical exposure, a re-rating becomes possible without requiring heroic group-level growth.

What makes the timing workable is that the supporting evidence is no longer entirely conceptual:

In 9M FY2026, Medical / Healthcare sales rose 10.7% and operating profit rose ~75%.

Smart segment swung from a loss to a profit.

Company disclosures have become more explicit about AI-linked semiconductor demand and LCP use in GPU sockets and cooling fans for AI servers.

The market is still paying for a tired cyclical but the product map suggests something more interesting.

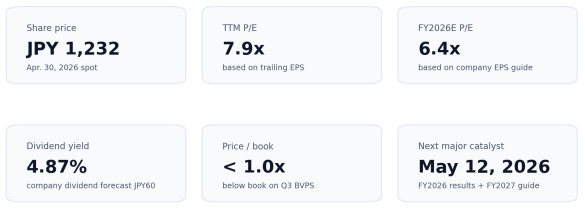

Figure 1 — Selected Valuation Metrics: Daicel still trades like a cyclical chemicals stock, not like a strategically relevant supplier to health and AI infrastructure.

Company Overview

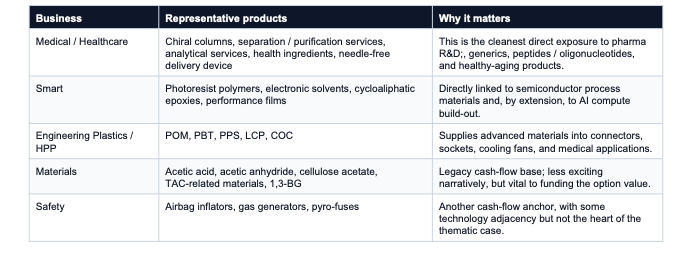

Daicel Corporation is a diversified Japanese chemicals company with five reported businesses: Medical/Healthcare, Smart, Safety, Materials, and Engineering Plastics. The company traces its roots to cellulose chemistry and celluloid, but the portfolio now spans acetyl chain products, airbag inflators, electronic materials, functional films, engineering plastics, chiral columns, functional foods, and medical devices.

Engineering Plastics is the largest segment by revenue and the core of the AI-infrastructure angle. Daicel fully owns Polyplastics and is integrating its engineering plastics business into Daicel effective April 2026. Polyplastics brings POM, PBT, PPS, LCP, and COC products plus global technical solution centers. The company disclosed that LCP capacity started operation in Taiwan in February 2025, and that Engineering Plastics demand includes PPS/PBT for AI servers and LCP demand in AI-server and electronic-device applications.

The Smart segment is the semiconductor-materials vector. Daicel discloses advanced-technology products including polymers for photoresists, solvents for electronic materials and high-performance films. The company identifies increased demand in AI semiconductors and cutting-edge logic/memory as relevant to these products, while also discussing front-end and back-end semiconductor process opportunities.

Medical/Healthcare is smaller in reported revenue, but strategically useful. It includes chiral columns/stationary phases, separation and purification services, novel drug delivery devices, cosmetic ingredients, and functional food ingredients including Equol, Urolithin, Lactobionic acid and Astrohop. The segment is not large enough today to drive the whole equity story, but it gives Daicel a credible healthcare picks-and-axes lane.

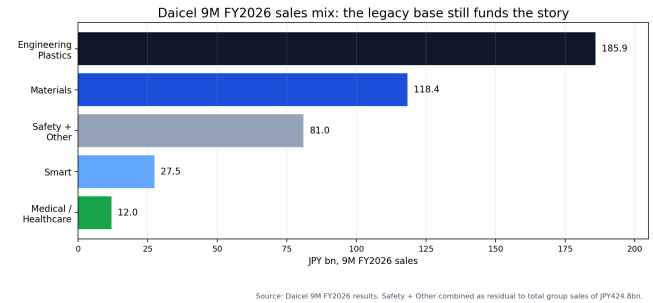

Figure 2 — Sales Mix, simplified. The legacy base is still large which is why the market continues to classify Daicel as a cyclical chemicals company.

The Setup

The setup is a classification error:

The market sees deteriorating cyclical earnings, China exposure, capex intensity, and raw-material volatility.

The product map shows a company with genuine exposure to the tools and materials that sit underneath two of the more durable end-markets in global industry.

Those two views are not mutually exclusive. The stock is interesting because both are true at once.

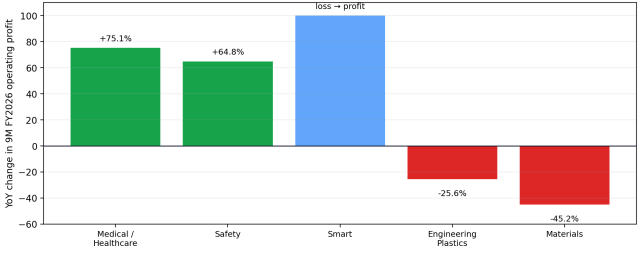

The bad news is easy to see: In 9M FY2026, group sales declined 1.8% year over year and operating profit fell 25.0%. Materials operating profit fell 45.2%, and Engineering Plastics fell 25.6%. When the profit pools that dominate the group are moving in that direction, it is unsurprising that investors refuse to award a premium multiple.

The more interesting news is hiding one layer below that. Medical / Healthcare posted 10.7% sales growth and 75.1% operating-profit growth. Safety also improved sharply. Smart swung from an operating loss to a profit. In other words, the parts of the portfolio most relevant to the “health and AI picks-and-shovels” framing are not merely conceptually attractive; they are beginning to improve in the financials as well.

Figure 3 — Operating profit trend, simplified.

The base case is not that Daicel becomes an AI pure-play. The base case is that the market stops penalizing the whole company as a structurally ex-growth chemicals collection once the quality mix becomes more visible.

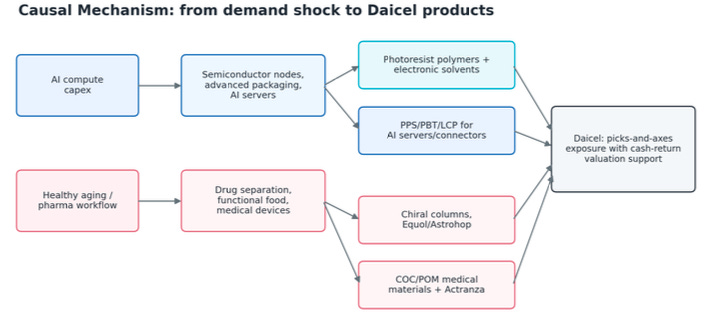

Casual Mechanism

The causal mechanism is a materials-stack story. AI demand creates incremental capex in data centers, accelerators, memory, advanced packaging and high-speed electronics. That demand does not only accrue to GPU designers; it creates a pull-through for high-purity chemicals, photoresist polymers, precision connectors and heat-resistant engineering plastics. Daicel sits lower in the stack, where the unit economics are less glamorous but often more durable because qualification cycles, purity requirements and customer-specific formulations create switching frictions.

Figure 5 — Mechanism map linking AI and health demand to Daicel categories.

The health case rests first on chiral separation. Daicel describes its optical-isomer separation business as having a world-leading position, with operations across Japan, the U.S., France, China, and India. This is better than typical healthcare equity, it is a tool-maker business. Demand is tied to pharmaceutical analysis, separation, purification, and synthesis, and management is explicitly broadening target applications from small molecules toward peptides and oligonucleotides. That is exactly the kind of exposure one wants in a picks-and-shovels framing: less dependent on a single drug outcome, more tied to the activity layer.

The second part of the health case is smaller today, but strategically useful. Daicel has launched ASTROHOP, a health-food ingredient aimed at aging-related muscle concerns, and is also pursuing a needle-free subcutaneous drug-delivery device. Neither line needs to become a huge standalone business for the equity to work.

The AI case is more credible than a quick screen would suggest. Through the Smart business, Daicel sells high-performance polymers for photoresists and electronic solvents used in semiconductor manufacturing. The company also highlights strong positioning in high-boiling-point solvents used as resist solvents and thinners, and explicitly references sales growth opportunities tied to AI demand. In a market where “AI exposure” is often stretched beyond recognition, this is relatively clean: these are enabling materials.

The second layer of the AI case runs through engineering plastics. Polyplastics LCP has a leading position globally, and company materials specifically reference rising use in GPU sockets and cooling fans for AI servers. This matters because it turns the AI thesis from a pure semiconductor-fabrication story into a broader content-per-box story.

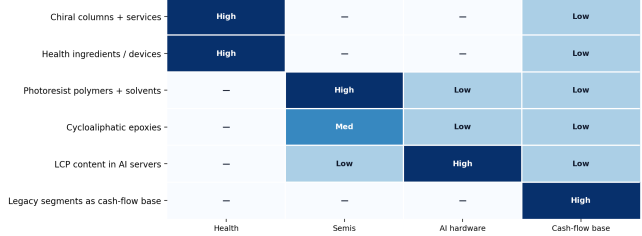

Figure 6 — Theme Exposure Matrix

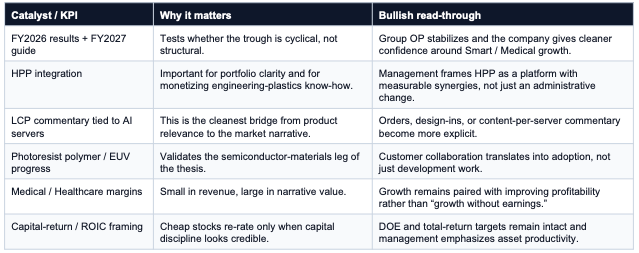

Timeline

The next year is about proof. Investors simply need evidence that the financially relevant pieces of the portfolio are becoming less small, less volatile, and more legible. The May 12, 2026 result is therefore the first real forcing function. After that, the quality of management commentary around HPP integration, Smart growth, LCP demand, and medical / healthcare margins will matter more than broad thematic language.

Figure 7 — Catalyst Path

Key Risks

The right risk lens is straightforward: the thematic product lines may be real, but they may remain too small to matter at the pace the market wants. That is the main risk. The other risks are mostly variants of that same issue.

Scale risk: Smart and Medical / Healthcare remain small relative to Engineering Plastics and Materials. Product relevance alone does not guarantee group-level rerating.

Cyclical-earnings risk: Materials and Engineering Plastics still dominate the P&L. If those pools remain weak, investors may continue to anchor on trough optics.

Execution risk: EUV polymers, AI-server LCP content, and medical-device programs require customer qualification and commercialization discipline. Delays would push out the thesis timeline.

China / macro risk: Daicel itself flags uncertainty around China, raw-material costs, and competitive pricing pressure. Those factors can overwhelm segment-level progress for long stretches.

Capex and asset-productivity risk: This is not a pristine capital-light story. The market will need evidence that rising asset intensity is being converted into better returns.

Value-trap risk: A low P/E and P/B are only useful if the market begins to believe the quality of the portfolio is improving. Otherwise the stock can stay statistically cheap for years.

Conclusion

Daicel is a credible picks-and-axes supplier to AI and health, but the cleanest version of the thesis is not that it is a pure AI or healthcare stock. The clean version is that the market is pricing a cyclical Japanese chemical company while the product mix increasingly includes higher-value, qualification-heavy materials for AI semiconductors, AI servers, pharmaceutical workflow, functional foods and medical materials.

The stock offers a value-backed way to own that transition: low trailing multiples, a meaningful dividend yield, buyback/capital-return support, and a May 2026 guidance catalyst. The near-term hurdle is credibility. Daicel needs to show that the March 2026 COC impairment is a reset, that Materials can stabilize, and that Engineering Plastics/Smart can convert AI and semiconductor demand into margin rather than merely revenue.

The bottom line is Daicel looks like a low-expectation cyclical chemicals name. The better interpretation is a misclassified picks-and-shovels supplier to health and AI, funded by legacy cash flow and priced as if none of the optionality matters.

Very well written. This seems like a really diversified company, and they have the upside of AI while keeping options for a stable downside through Engineering, Medical, etc.