Monthly Ridindex Update (November 2025)

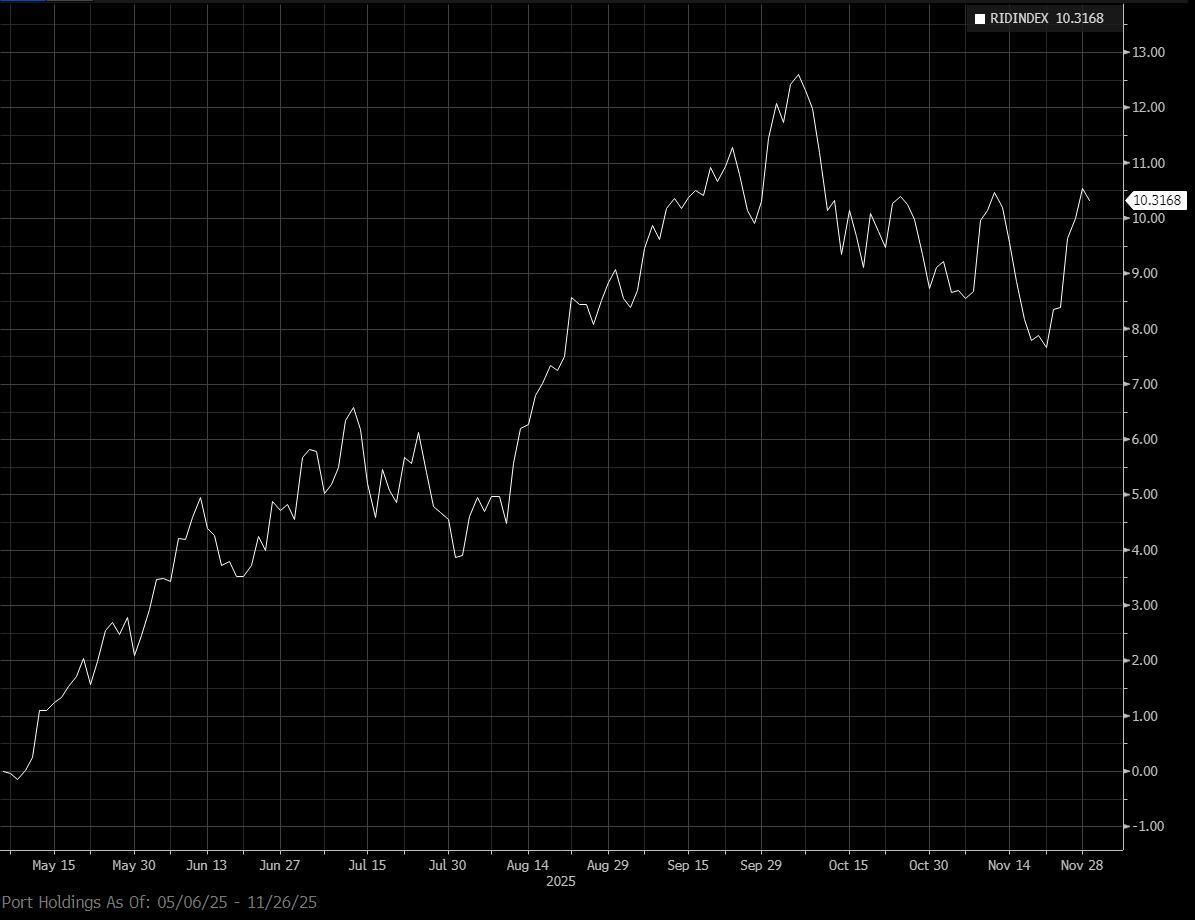

Since Inception (05/06/2025) Performance: +10.3%

Ridindex Since Inception Chart:

Link to Current Positions → HERE

🏆 Top 5 Contributors This Month

EXE (Long) +0.35%: The stock rallied sharply, and our overweight position helped. The company continues to execute well, and investors are starting to reward its improving financial profile and potential as an AI beneficiary. (Reference article)

ZS (Short) +0.26%: Zscaler sold off during the month, benefiting our short. High-growth software names faced pressure as investors rotated away from premium valuations. (Reference article)

JAZZ (Long) +0.25%: Jazz delivered a strong month on the back of solid results and better clarity around its pipeline. Even a modest long position produced meaningful contribution. (Note this is part of a pair trade, the other side is short WST)

NET (Short) +0.23%: Cloudflare declined as expectations reset for high-multiple software. The move lower supported our short, which continues to hedge factor risk in the portfolio. (Reference article)

PD (Short) +0.22%: PagerDuty weakened throughout the month as growth slowed and spending remained cautious across IT budgets. The short position added steady attribution.

💣 Largest Detractors This Month

NICE (Long) (–0.27%): The shares pulled back sharply as investors reassessed growth expectations in enterprise software. Our small long position detracted modestly. (Reference article)

AIRS (Long) (–0.36%): AirSculpt continued to sell off on weak procedure volumes and soft guidance. Even at a small weight, the magnitude of the decline drove a meaningful loss.

4180 JP (Long) (–0.38%): Appier traded lower as digital-ad spending stayed uneven and margin improvement remained slower than hoped. The long position was a steady drag through the month. (Reference article)

XBI (Short) (–0.41%): Biotech outperformed as risk appetite improved, which worked against our short. The rebound across smaller clinical-stage names added consistent pressure. (Reference articles: one and two)

IBIT (Long) (–0.73%): Bitcoin weakened throughout the month, and our long exposure weighed the most among detractors. The move was mostly macro-driven, tied to broader risk sentiment. (Reference article)

🔍 Watchlist & Tactical Pipeline

We’re actively monitoring the following themes for potential entry or re-engagement:

Critical Minerals & Domestic Sourcing

The overlooked spine of decarbonization: antimony, rare alloys, and strategic metals tied to national-security sourcing mandates. A slow-moving but durable theme as Western and Asian governments onshore material sovereignty.

Power Infrastructure & Energy Repricing

The industrial expression of policy stimulus, solar, nuclear, and grid equipment capacity expanding in parallel. Beneficiaries span generation to transmission, with multi-year tailwinds from both transition incentives and grid reliability imperatives.

Applied Intelligence & Digital Adjacencies

Selective engagement in next-gen software, infrastructure, and consumer-tech ecosystems where AI utility (not hype) is being monetized. Focused on the layer between compute and interface, the bottleneck where data becomes product.

Structural Shorts

We remain positioned against narrative-driven SaaS and speculative consumer platforms where valuation elasticity has far outpaced operating leverage.

Final Notes

If anything is unclear or you’d like added context, raise it in the chat or comments. I’ve been collecting your questions over the past few weeks and will release a consolidated FAQ later this month. In addition, I’m considering introducing a small set of dashboards to support idea generation, likely something I’ll poll readers on before launching.

In closing, the Ridindex reflects the current set of published ideas as they are expressed within a model portfolio. Allocations are updated and tracked promptly so readers can monitor how the positioning evolves as new information comes in. The aim is simply to provide structure, clarity, and accountability around the idea flow.

The next review will be published after the December close. Until then, stay sharp.

Disclaimer:

This publication is for educational purposes only and reflects a hypothetical model portfolio. Nothing herein is investment advice or a solicitation. By reading, you agree to the full disclosures → Ridire Research Substack Disclaimer